Finance

How To Calculate Nominal Interest Rates

Modified: February 21, 2024

Learn how to calculate nominal interest rates in finance. Understand the formula and factors involved to make accurate interest rate calculations.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of finance, where numbers and calculations play a crucial role in determining the value of money. One key concept in the realm of finance is the nominal interest rate, which is integral to understanding the cost of borrowing and the return on investments. Whether you are a seasoned investor, a curious individual, or someone looking to make informed financial decisions, having a clear understanding of nominal interest rates is essential.

In this article, we will dive into the world of nominal interest rates, exploring their definition, components, and calculation methods. We will also provide you with practical examples to illustrate how nominal interest rates are determined and the impact they have on your financial decisions. Additionally, we will highlight the limitations of relying solely on nominal interest rates and discuss other factors that should be considered when evaluating financial opportunities.

So, strap in and get ready to embark on a journey to unravel the mysteries of nominal interest rates. By the end of this article, you will have a solid foundation to interpret and calculate nominal interest rates, empowering you to make informed financial decisions with confidence. Let’s dive in!

Understanding Nominal Interest Rates

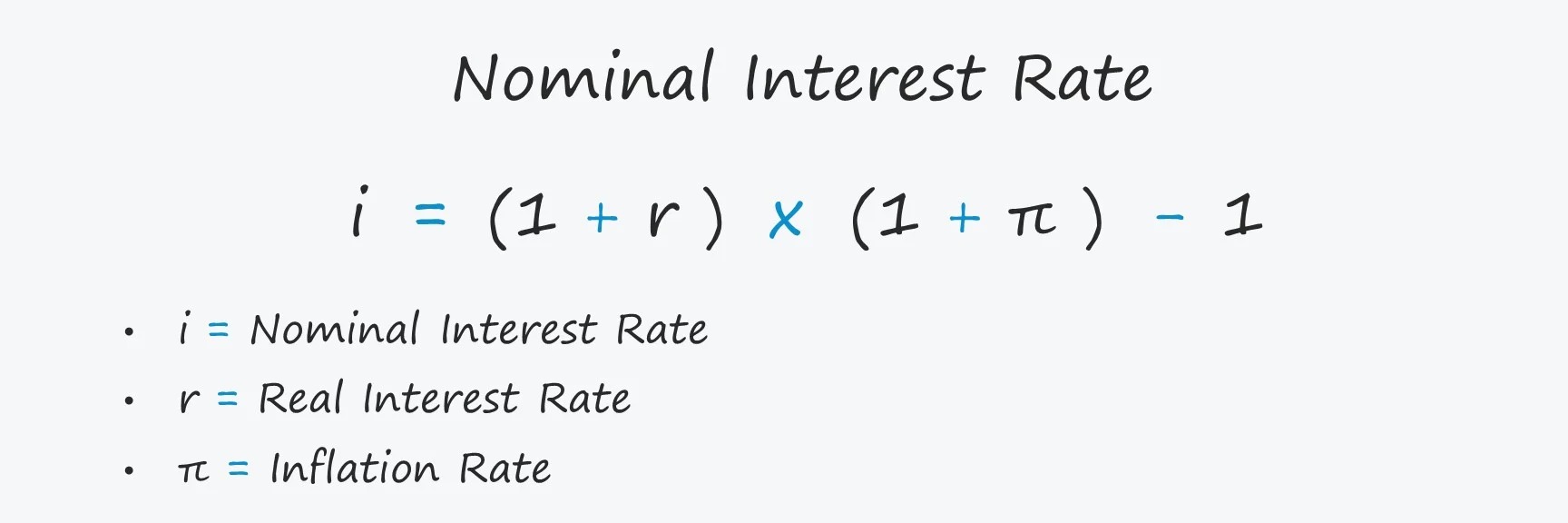

Before we delve into the calculation of nominal interest rates, it is important to have a clear understanding of what they represent. A nominal interest rate, also known as a stated or quoted interest rate, refers to the percentage of interest charged or earned on a loan or investment without considering the effect of inflation.

What sets nominal interest rates apart is that they do not take into account the impact of inflation on the purchasing power of money. In simple terms, nominal interest rates provide a baseline measure of the cost of borrowing or the return on investment, excluding the effects of price changes over time.

For example, let’s say you borrow $1,000 at a nominal interest rate of 5%. At face value, this means that you would owe $1,050 at the end of the loan term. However, if there is inflation of 3% during that period, the purchasing power of your money diminishes. Consequently, the real cost of borrowing is higher than the nominal interest rate suggests.

Understanding the distinction between nominal and real interest rates is crucial as it allows individuals and institutions to make more accurate financial projections and assessments. Real interest rates, which take inflation into account, provide a more realistic picture of the true cost or return on a loan or investment.

It’s important to note that nominal interest rates are typically expressed on an annual basis. For shorter-term loans or investments, the interest rate may be adjusted accordingly to reflect the time period involved.

Now that we have a solid understanding of what nominal interest rates entail, let’s take a closer look at the components that make up these rates.

Components of Nominal Interest Rates

When it comes to understanding nominal interest rates, it is essential to be familiar with the key components that contribute to their calculation. These components help determine the final rate that borrowers or investors encounter in various financial transactions.

1. Base Interest Rate: The base interest rate forms the foundation of the nominal interest rate. It represents the compensation lenders or investors expect for lending their money. Base interest rates are influenced by various factors, including economic conditions, central bank policies, and market forces.

2. Inflation Expectations: Inflation expectations refer to the anticipated rate of inflation over the loan or investment period. Lenders and investors consider inflation expectations when setting nominal interest rates. Higher inflation expectations result in higher nominal interest rates to account for the erosion of purchasing power over time.

3. Risk Premium: The risk premium is an additional component included in nominal interest rates to compensate lenders or investors for the level of risk associated with a particular loan or investment. Different borrowers or investments carry varying levels of risk, and lenders require a higher return as compensation for taking on higher risk. Factors such as creditworthiness, collateral, and market conditions impact the risk premium.

4. Lender’s Costs: Lenders incur costs in providing loans or making investments, such as administrative expenses, the cost of capital, and overhead costs. These costs are factored into the nominal interest rate to ensure that lenders can cover their expenses and earn a reasonable profit.

By considering these components, lenders and investors calculate the nominal interest rate that appropriately reflects the risk, inflation expectations, and costs associated with a particular transaction.

It is worth noting that the weightage given to each component may vary depending on factors such as the borrower’s creditworthiness, prevailing market conditions, and the term of the loan or investment. Therefore, understanding these components helps borrowers and investors assess the fairness and competitiveness of the nominal interest rates offered to them.

Now that we have explored the components comprising nominal interest rates, let’s move on to the next section that focuses on calculating these rates.

Calculating Nominal Interest Rates

The calculation of nominal interest rates involves combining the various components we discussed earlier. By understanding how these components interact, you can determine the nominal interest rate associated with a loan or investment.

To calculate the nominal interest rate, you need to follow these steps:

- Determine the base interest rate: Start by identifying the prevailing base interest rate in the market. This rate serves as a benchmark for lenders and investors.

- Consider inflation expectations: Evaluate the expected rate of inflation over the loan or investment period. This estimation allows you to assess the impact of inflation on the final nominal interest rate.

- Include the risk premium: Assess the level of risk associated with the specific loan or investment. Higher-risk transactions typically warrant a higher risk premium, contributing to an elevated nominal interest rate.

- Account for lender’s costs: Consider the costs incurred by lenders in providing the loan or making the investment. These costs, such as administrative fees, capital costs, and overhead expenses, are factored into the nominal interest rate calculation.

- Combine the components: Once you have determined the values for each component, add them together to calculate the nominal interest rate. The formula may vary depending on the complexity of the transaction and the specific circumstances involved.

It is important to note that the above steps provide a general framework for calculating nominal interest rates. The specific formula and methodology may vary depending on the type of loan or investment and the prevailing market conditions.

Furthermore, keep in mind that nominal interest rates are typically expressed on an annual basis. If you are dealing with a loan or investment with a different time period, you may need to adjust the interest rate accordingly.

Now that you have a clearer understanding of how to calculate nominal interest rates, let’s move on to the next section where we will explore practical examples to further illustrate the concept.

Example Calculations

To help solidify your understanding of nominal interest rate calculations, let’s take a look at a few practical examples:

Example 1: Personal Loan

Suppose you are considering taking out a personal loan for $10,000 with a term of 3 years. The bank offers a base interest rate of 6%, inflation is expected to be 2% per year, and they determine that your risk profile warrants a risk premium of 2%. Additionally, the lender’s costs amount to 1% of the loan amount.

Using these values, we can calculate the nominal interest rate as follows:

- Base Interest Rate: 6%

- Inflation Expectations: 2% per year

- Risk Premium: 2%

- Lender’s Costs: 1% of the loan amount

Nominal Interest Rate = Base Interest Rate + Inflation Expectations + Risk Premium + Lender’s Costs

Nominal Interest Rate = 6% + 2% + 2% + 1% = 11%

Therefore, the nominal interest rate for this personal loan would be 11%.

Example 2: Investment Opportunity

Imagine you are considering investing in a bond that offers a base interest rate of 4%. Inflation is projected to be 3% per year, the risk premium for this bond is 1%, and the lender’s costs amount to 0.5% of the investment amount.

Using these values, we can calculate the nominal interest rate as follows:

- Base Interest Rate: 4%

- Inflation Expectations: 3% per year

- Risk Premium: 1%

- Lender’s Costs: 0.5% of the investment amount

Nominal Interest Rate = Base Interest Rate + Inflation Expectations + Risk Premium + Lender’s Costs

Nominal Interest Rate = 4% + 3% + 1% + 0.5% = 8.5%

Therefore, the nominal interest rate for this investment opportunity would be 8.5%.

These examples showcase how the combination of base interest rates, inflation expectations, risk premiums, and lender’s costs contribute to the determination of nominal interest rates. Calculating nominal interest rates allows individuals and institutions to assess the true cost or return of financial transactions.

While nominal interest rates provide valuable insights, it is crucial to be aware of their limitations, which we will explore in the next section.

Limitations of Nominal Interest Rates

While nominal interest rates are a valuable metric for assessing the cost of borrowing or the return on investment, it is important to be aware of their limitations. Understanding these limitations can help you make more informed financial decisions and avoid potential pitfalls.

1. Does Not Account for Inflation: One of the primary limitations of nominal interest rates is that they do not account for the impact of inflation. Inflation erodes the purchasing power of money over time, reducing the real value of loans and investments. To get a more accurate picture, it is essential to consider real interest rates, which adjust for inflation.

2. Varies With Time and Term: Nominal interest rates can fluctuate with changes in economic conditions, market factors, and central bank policies. Additionally, the term of a loan or investment can affect the nominal interest rate. Shorter-term loans may have higher nominal interest rates compared to longer-term loans.

3. Does Not Capture Risk Factors: Nominal interest rates do not fully incorporate risk factors associated with a loan or investment. While a risk premium is included, it may not accurately reflect the actual level of risk involved. It is essential to consider other risk assessment tools, such as credit ratings and market conditions, when evaluating financial opportunities.

4. Does Not Consider External Factors: Nominal interest rates focus solely on the cost of borrowing or the return on investment without considering external factors that may affect the overall value. Factors such as taxes, fees, and unforeseen events can impact the actual cost or return of a financial transaction.

5. Dependent on Assumptions: Nominal interest rates are based on assumptions regarding inflation rates, risk assessments, and lender’s costs. These assumptions may not always align with the actual conditions and can lead to discrepancies between projected and realized costs or returns.

Despite these limitations, nominal interest rates serve as a foundational measure of the cost of borrowing or the return on investment. They provide a starting point for evaluating financial opportunities and understanding the baseline expectation. However, it is important to consider these limitations and complement your analysis with other factors to make well-informed decisions.

Now that we have explored the limitations of nominal interest rates, let’s conclude our journey into the world of finance.

Conclusion

Congratulations! You have successfully navigated the intricacies of nominal interest rates and gained a deeper understanding of their significance in the world of finance. We explored the definition of nominal interest rates and learned that they represent the cost of borrowing or the return on investment without factoring in inflation.

We also examined the components that contribute to the calculation of nominal interest rates, including the base interest rate, inflation expectations, risk premium, and lender’s costs. By understanding these components, you can assess the fairness and competitiveness of the rates offered to you.

Furthermore, we dived into the process of calculating nominal interest rates by combining these components. We explored practical examples to illustrate how the values are determined and how they impact the final nominal interest rate.

It is important to keep in mind the limitations of nominal interest rates. While they provide a useful baseline for evaluating financial transactions, they do not account for inflation, can vary with time and term, and may not fully capture all risk factors and external influences.

As you continue on your financial journey, remember to consider other factors, such as real interest rates, credit ratings, fees, and unforeseen events, to make well-informed decisions.

Armed with this knowledge, you are now equipped to navigate the financial landscape with confidence. Whether you are considering a loan, evaluating an investment opportunity, or simply seeking to expand your financial literacy, understanding nominal interest rates is a valuable tool.

Stay curious, continue learning, and make informed financial decisions that align with your goals and aspirations. The world of finance is ever-evolving, and by staying informed, you can make sound financial choices that lead to a secure and prosperous future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance