Home>Finance>When A Person Declares Bankruptcy That Fact Will Appear On The Persons Credit Report

Finance

When A Person Declares Bankruptcy That Fact Will Appear On The Persons Credit Report

Published: October 21, 2023

Learn how declaring bankruptcy affects your credit report and financial situation. Get insights and advice on managing your finances after bankruptcy.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In today’s fast-paced and consumer-driven society, financial struggles are not uncommon. At some point in their lives, many individuals may face overwhelming debt and financial difficulties. When these challenges become too burdensome to handle, the option of declaring bankruptcy may arise. However, it is important to understand that declaring bankruptcy can have significant consequences, especially when it comes to a person’s credit report.

A credit report is a comprehensive record of an individual’s borrowing and repayment history. It plays a crucial role in determining one’s creditworthiness and affects their ability to secure loans, credit cards, and other financial opportunities. Any negative remarks on a credit report can have lasting implications, and bankruptcy is no exception.

In this article, we will explore the relationship between bankruptcy and credit reports, shedding light on how bankruptcy impacts a person’s creditworthiness. Additionally, we will discuss the duration of time that bankruptcy stays on a credit report and offer some insights into rebuilding credit after bankruptcy.

It is important to remember that this article is for informational purposes only and should not be considered legal advice. If you are considering bankruptcy or have questions about your specific financial situation, it is always best to consult with a qualified bankruptcy attorney who can provide guidance tailored to your unique circumstances.

What is bankruptcy?

Bankruptcy is a legal process that provides individuals or businesses with financial relief when they are unable to repay their debts. It is a way for debtors to obtain a fresh financial start by either restructuring their debts or having them discharged altogether.

There are different types of bankruptcy, but the most common ones for individuals are Chapter 7 and Chapter 13 bankruptcy. Chapter 7 bankruptcy, also known as liquidation bankruptcy, involves the sale of a debtor’s non-exempt assets to repay creditors. In this type of bankruptcy, most unsecured debts, such as credit card debt and medical bills, can be discharged. On the other hand, Chapter 13 bankruptcy is a reorganization bankruptcy that allows individuals to create a repayment plan to pay off their debts over a specific period of time.

Bankruptcy should not be seen as an easy way out of financial obligations, as it has long-term implications. It is a serious decision that should be carefully considered after exploring other alternatives, such as debt consolidation or negotiating with creditors. Declaring bankruptcy can have a significant impact on an individual’s financial future, especially when it comes to their credit report.

It is important to consult with a qualified bankruptcy attorney to understand the specific bankruptcy laws in your jurisdiction and the potential consequences before making any decisions. They can help you evaluate your financial situation, assess the feasibility of bankruptcy, and guide you through the process.

Understanding credit reports

A credit report is a detailed document that provides a snapshot of an individual’s credit history. It contains information about their borrowing and payment activities, as well as details about their current and past debts.

Typically, credit reports are compiled by credit reporting agencies, also known as credit bureaus. The three major credit bureaus in the United States are Equifax, Experian, and TransUnion. These agencies gather information from various sources, including lenders, credit card issuers, and public records, to create comprehensive credit reports.

Some key elements found in a credit report include:

- Personal information: This includes your name, address, social security number, and date of birth. It is important to review this section for accuracy and report any discrepancies.

- Credit accounts: This section lists all the credit lines and loans you have, including credit cards, mortgages, auto loans, and student loans. It provides details about the account balance, payment history, and current status.

- Public records: This includes information about any bankruptcies, tax liens, or judgments filed against you. Public records can have a significant impact on your creditworthiness and may remain on your credit report for several years.

- Inquiries: Whenever you apply for credit, the lender conducts a credit inquiry. These inquiries are documented in your credit report and can be either hard inquiries or soft inquiries. Hard inquiries, such as those made when applying for a loan, can temporarily lower your credit score, while soft inquiries, like those made by potential employers or lenders for promotional purposes, do not affect your credit score.

It’s important to review your credit report regularly to ensure its accuracy and identify any potential errors or fraudulent activity. By law, you are entitled to a free copy of your credit report from each of the major credit bureaus every year. You can request your report through the official website AnnualCreditReport.com.

Understanding the information contained in your credit report is essential for managing your finances effectively and making informed decisions. Now, let’s explore how bankruptcy impacts your credit report and creditworthiness.

How does bankruptcy impact a credit report?

Declaring bankruptcy can have a significant impact on your credit report and creditworthiness. When you file for bankruptcy, it is reflected on your credit report as a negative remark and can stay there for a considerable period of time.

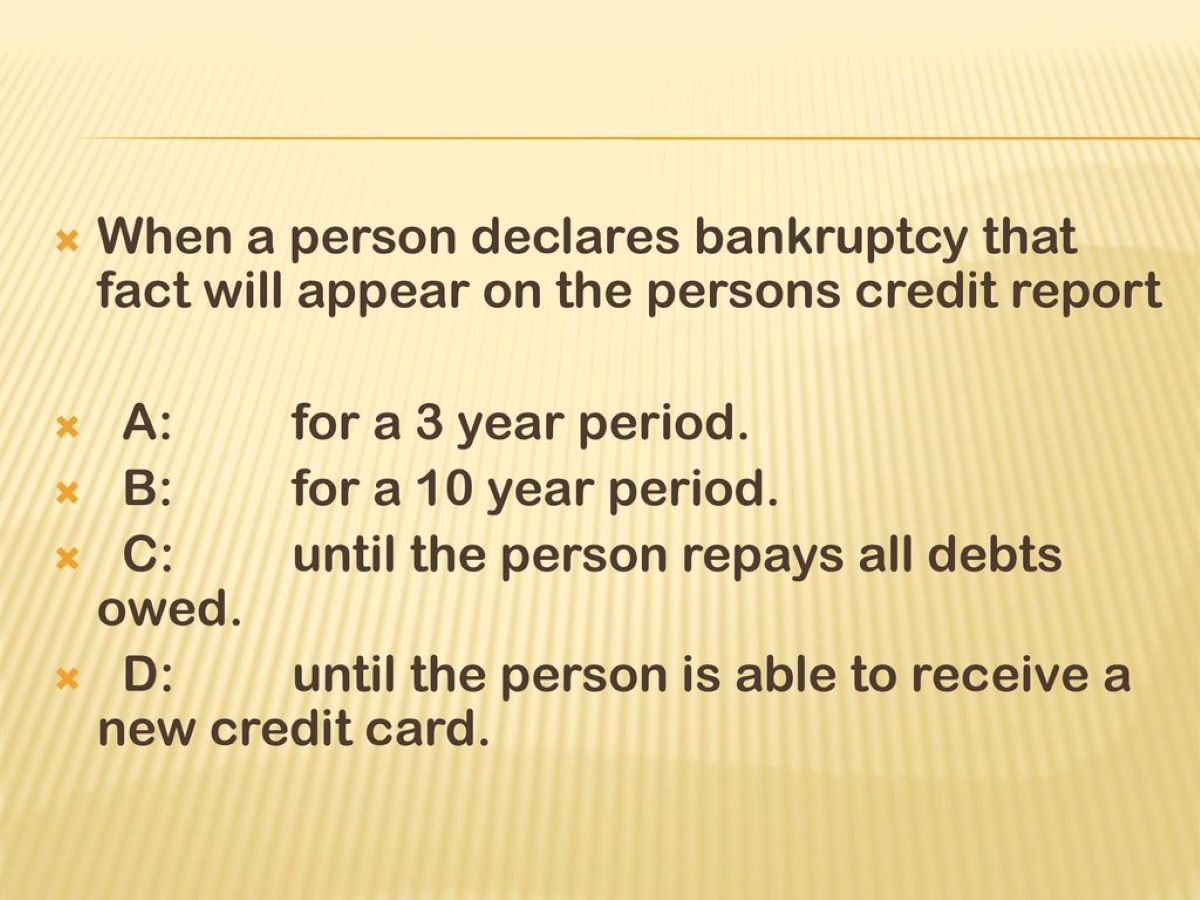

The specific impact of bankruptcy on your credit report depends on the type of bankruptcy you file. In the case of Chapter 7 bankruptcy, it will typically remain on your credit report for up to ten years. For Chapter 13 bankruptcy, which involves a repayment plan, it may stay on your credit report for up to seven years.

Bankruptcy affects various aspects of your credit report:

- Account status: When you file for bankruptcy, the accounts included in the bankruptcy will be updated on your credit report to reflect their new status. They may be listed as “included in bankruptcy,” “discharged through bankruptcy,” or a similar notation.

- Impact on credit score: Bankruptcy significantly impacts your credit score, resulting in a substantial decrease. The exact decrease in your score will depend on factors such as your previous credit history and the specific details of your bankruptcy.

- Difficulty obtaining new credit: After bankruptcy, it may become challenging to obtain new lines of credit or loans. Lenders may view you as a higher risk and may be hesitant to extend credit to you. If you are approved for credit, you may face higher interest rates and more stringent terms.

It’s important to note that bankruptcy doesn’t erase your credit history. While bankruptcy remains on your credit report for a significant period, as time passes, its impact will gradually decrease. Lenders and creditors may also consider other factors, such as your current financial situation and recent credit behavior, when evaluating your creditworthiness.

Keep in mind that each credit bureau may update your credit report at different times, so it’s essential to review all three reports regularly to ensure the accuracy of the information. If you spot any errors or inaccuracies in relation to your bankruptcy, you have the right to dispute them with the credit bureau to have them resolved.

Next, let’s explore the impact of bankruptcy on credit scores and how long bankruptcy remains on your credit report.

Bankruptcy and credit scores

One of the most significant impacts of bankruptcy is its effect on your credit score. A credit score is a numerical representation of your creditworthiness and plays a crucial role in determining your ability to obtain credit. Bankruptcy can cause a significant drop in your credit score, but the exact decrease will depend on various factors, such as your previous credit history and the specifics of your bankruptcy.

Before filing for bankruptcy, it is essential to understand that your credit score will likely be negatively affected. However, if you are already struggling with overwhelming debt and missed payments, your credit score may already be low. In such cases, bankruptcy can provide an opportunity to rebuild your financial life and ultimately improve your credit score over time.

It is crucial to note that the impact of bankruptcy on your credit score can vary. For individuals with higher credit scores at the time of filing, the drop may be more significant due to the larger distance to fall. Conversely, those with lower credit scores may experience a relatively smaller impact.

While it may take time, it is possible to rebuild your credit score after bankruptcy. Here are some steps you can take to begin the process of rebuilding your credit:

- Create a budget and stick to it: Establishing a solid budget will help you manage your finances and ensure you can make timely payments on any new credit you obtain.

- Apply for a secured credit card: A secured credit card requires a cash deposit as collateral, making it easier to obtain. Using a secured credit card responsibly and making timely payments can help rebuild your credit.

- Make all payments on time: Timely payments on any new credit or loans you obtain will help demonstrate your improved financial discipline and reliability.

- Monitor your credit report: Regularly reviewing your credit report will allow you to track your progress and identify any errors or inaccuracies that need to be addressed.

Rebuilding your credit score after bankruptcy will require time, patience, and responsible financial habits. While the impact of bankruptcy on your credit report and credit score may feel daunting, it is important to remember that it is not permanent. By taking proactive steps and demonstrating improved financial behavior, you can gradually rebuild your creditworthiness.

Now, let’s explore how long bankruptcy stays on your credit report and the steps you can take to rebuild your credit after bankruptcy.

How long does bankruptcy stay on a credit report?

Bankruptcy will remain on your credit report for a specific period, depending on the type of bankruptcy you filed. The two most common types of bankruptcy for individuals, Chapter 7 and Chapter 13, have different durations of appearance on your credit report.

For Chapter 7 bankruptcy, which involves the liquidation of assets, it typically stays on your credit report for up to ten years from the date of filing. During this time, lenders and creditors will be able to see the bankruptcy notation on your credit report. It is important to note that the impact of bankruptcy on your credit score will lessen over time, especially as you establish a positive credit history moving forward.

In the case of Chapter 13 bankruptcy, which involves a repayment plan, the duration is generally shorter. Chapter 13 bankruptcy remains on your credit report for up to seven years from the date of filing. As with Chapter 7 bankruptcy, although the notation will still appear on your report, its impact on your credit score will gradually diminish over time.

While bankruptcy has a significant impact on your credit report and creditworthiness, it is important to remember that it is not the end of the road. As time passes and you take steps to rebuild your credit, the impact of bankruptcy will lessen. It is essential to maintain responsible financial habits, such as making timely payments on any new credit you obtain and managing your finances wisely.

It is important to note that although bankruptcy remains on your credit report for a specific period, you are not permanently labeled as someone who filed for bankruptcy. Lenders and creditors consider other factors, such as your current financial situation, income stability, and credit behavior since the bankruptcy, when evaluating your creditworthiness.

It’s crucial to review your credit report regularly to ensure the accuracy of the information and to address any errors or discrepancies. By responsibly managing your credit and practicing good financial habits, you can gradually rebuild your credit history and improve your creditworthiness beyond the impact of bankruptcy.

Now, let’s explore some steps you can take to rebuild your credit after bankruptcy.

Rebuilding credit after bankruptcy

Rebuilding your credit after bankruptcy requires time, patience, and careful financial management. While bankruptcy can have a significant impact on your creditworthiness, it is not a permanent hindrance. Here are some steps you can take to start rebuilding your credit:

- Create a budget: Establishing a budget is essential for managing your finances effectively. Track your income and expenses, prioritize your payments, and ensure that you have enough funds to meet your financial obligations.

- Make timely payments: Paying your bills and any new credit you obtain on time is crucial for rebuilding your credit. Timely payments demonstrate financial responsibility and improve your creditworthiness.

- Obtain a secured credit card: A secured credit card requires a cash deposit as collateral. Using a secured credit card responsibly and making timely payments can help rebuild your credit history. Over time, you may qualify for an unsecured credit card.

- Apply for a small loan: If you’re ready to take on additional credit, consider applying for a small loan from a reputable lender. Use the proceeds responsibly and make all payments on time to demonstrate your new financial discipline.

- Monitor your credit report: Regularly review your credit report to track your progress and ensure the accuracy of the information. Report any errors or discrepancies to the credit bureau to have them corrected.

- Establish a mix of credit: Having a diverse credit mix, such as a combination of credit cards, loans, and a mortgage, can demonstrate your ability to manage different types of credit responsibly.

- Practice patience: Rebuilding your credit after bankruptcy takes time. It won’t happen overnight, but with consistent effort and responsible financial behavior, you can gradually improve your creditworthiness.

Remember to explore and understand your options before applying for new credit. Some lenders specialize in providing credit to individuals who have gone through bankruptcy. However, be cautious of predatory lenders who may charge excessively high interest rates or apply hidden fees. Research different options, compare terms, and choose reputable lenders to ensure you get the best possible terms for your situation.

Additionally, take advantage of financial education resources and seek guidance from reputable credit counseling agencies. They can provide valuable insights and personalized advice to help you improve your financial situation and rebuild your credit after bankruptcy.

Rebuilding credit after bankruptcy is a gradual process, but it is within your control. By practicing responsible financial habits, making timely payments, and demonstrating improved money management, you can rebuild your creditworthiness and regain your financial footing.

Now, let’s conclude our discussion on the impact of bankruptcy on credit reports and creditworthiness.

Conclusion

Declaring bankruptcy is a significant decision that can have lasting impacts on your credit report and creditworthiness. It is important to have a thorough understanding of the implications before proceeding with bankruptcy. Although bankruptcy can have a negative impact on your credit report, it is not a permanent obstacle. By taking proactive steps and practicing responsible financial habits, you can rebuild your credit over time.

Remember to review your credit report regularly for accuracy and address any errors or discrepancies promptly. Timely payments, budgeting, and obtaining new credit responsibly are key factors in rebuilding your credit after bankruptcy. It may take time and patience, but with dedication and perseverance, you can improve your credit score and regain your financial stability.

However, it’s also essential to be cautious of opportunistic lenders who may take advantage of individuals who have gone through bankruptcy. Research and select reputable lenders who offer fair terms and rates.

Lastly, it is advisable to seek guidance from qualified professionals, such as bankruptcy attorneys or credit counseling agencies, to navigate through the process effectively and make informed decisions regarding your financial future.

Remember that everyone’s situation is unique, and there is no one-size-fits-all approach to rebuilding credit after bankruptcy. Tailor your strategy to your specific circumstances and remain focused on long-term financial stability. With resilience and determination, you can overcome the challenges of bankruptcy and embark on a path towards a stronger financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance