Home>Finance>What Are Credit Default Swaps? What Role Did They Play In The Meltdown

Finance

What Are Credit Default Swaps? What Role Did They Play In The Meltdown

Published: March 4, 2024

Learn about credit default swaps and their impact on the financial meltdown. Understand the role of credit default swaps in finance and the consequences of their use.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding Credit Default Swaps

In the complex world of finance, certain instruments wield remarkable influence, often without the general public fully comprehending their intricacies. One such instrument that gained notoriety during the global financial crisis of 2008 is the Credit Default Swap (CDS). Understanding the nature and function of CDS is vital to grasp the events that precipitated the economic meltdown.

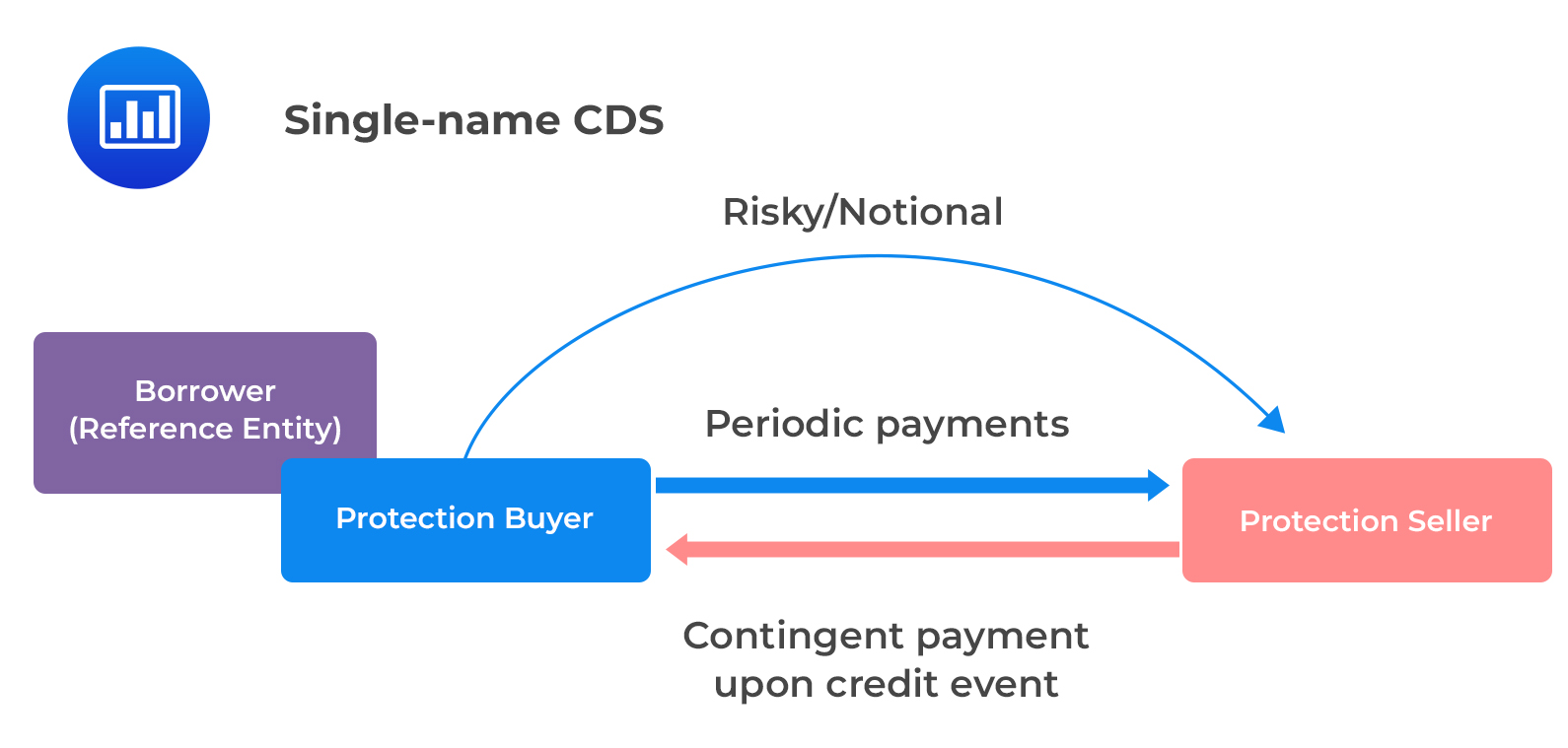

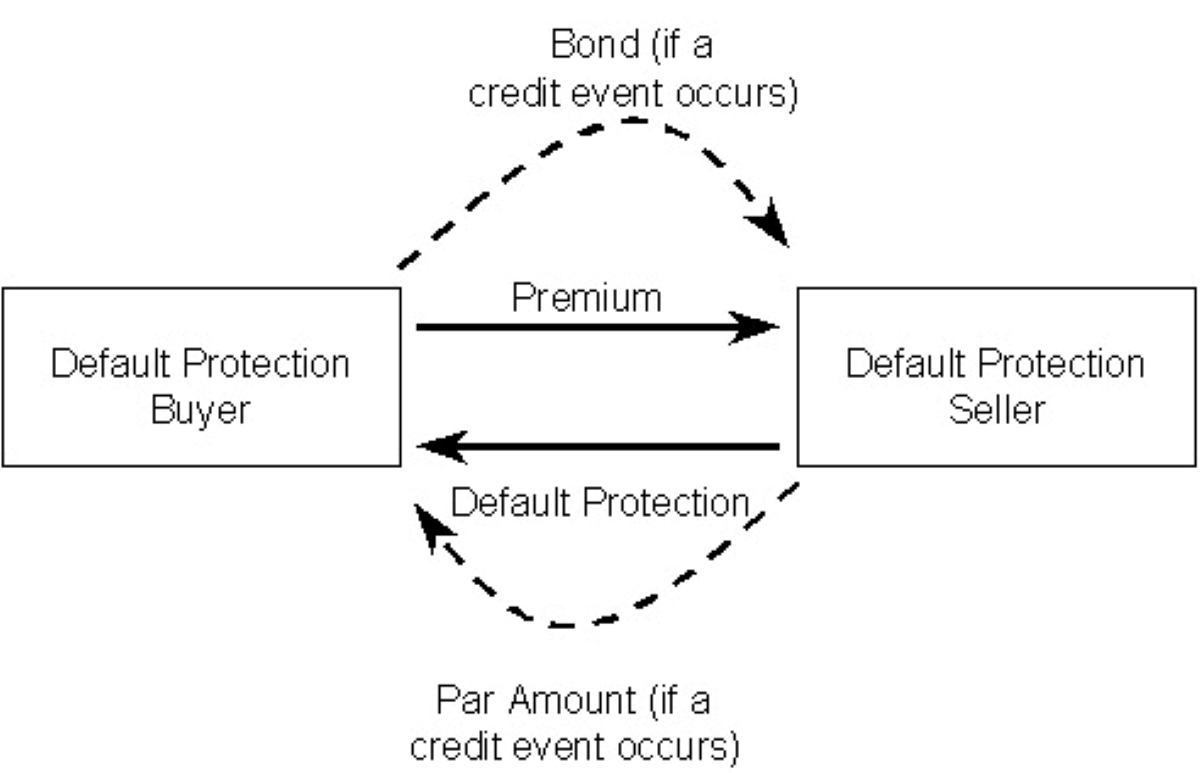

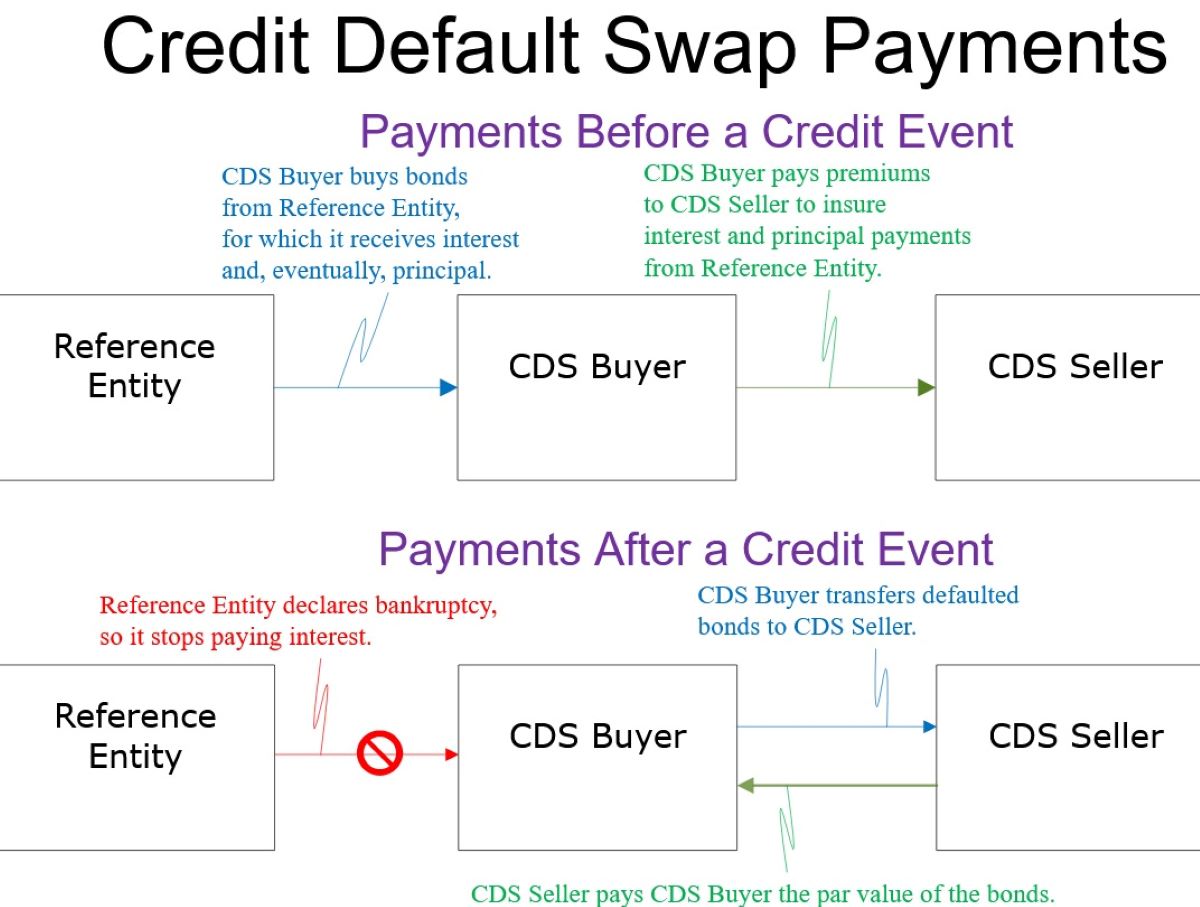

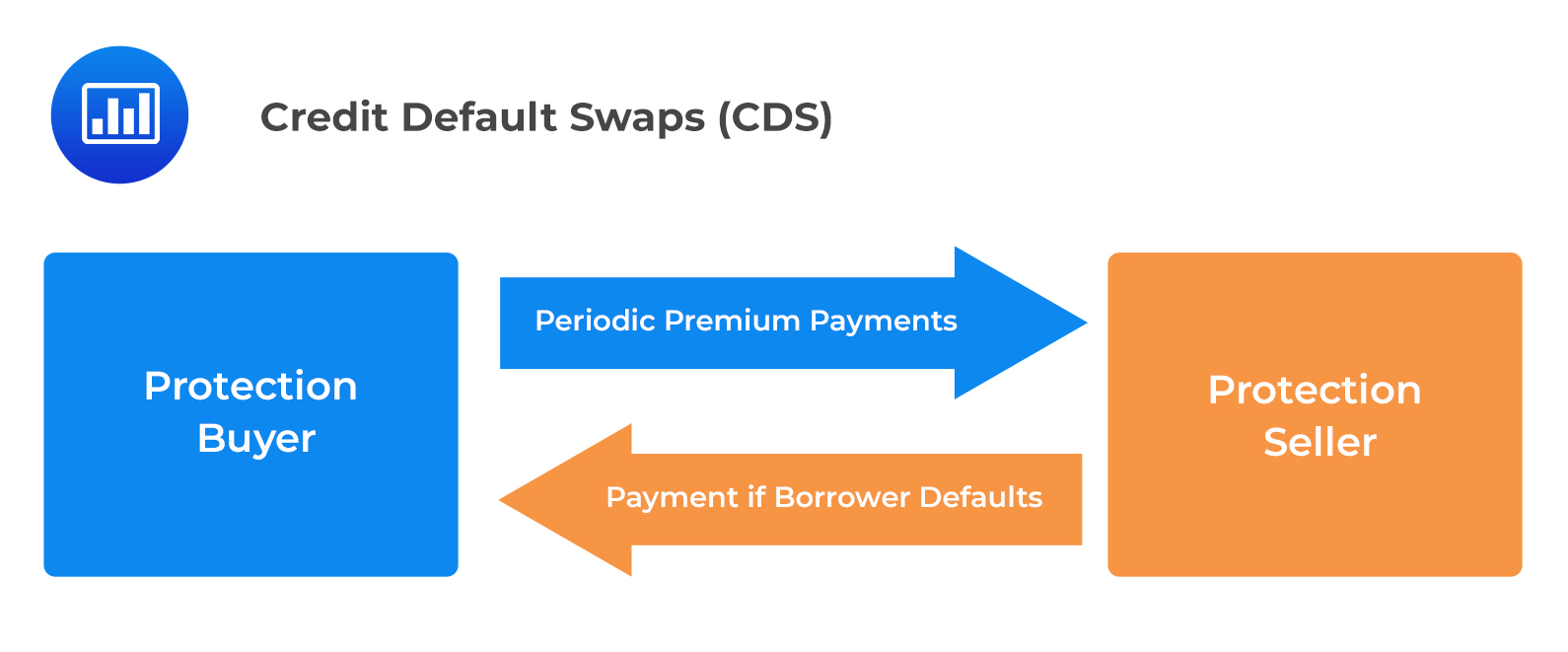

Credit Default Swaps, often referred to as CDS, are financial derivatives that enable investors to protect themselves against the risk of a borrower defaulting on their debt. They essentially operate as insurance policies against non-payment. The buyer of a CDS pays a premium to the seller in exchange for protection in the event that the underlying asset, typically a bond or loan, defaults. If the borrower does default, the seller of the CDS compensates the buyer for the losses incurred.

CDS can be likened to a form of hedging, allowing investors to mitigate their exposure to credit risk. They are also used for speculative purposes, enabling investors to bet on the creditworthiness of a particular entity without owning the underlying debt. This speculative aspect of CDS trading has been a subject of controversy, as it introduced a layer of complexity and opacity to the financial markets.

The widespread use and intricate interconnections of Credit Default Swaps played a pivotal role in the events leading up to the financial crisis. Understanding the mechanics and implications of CDS is crucial in comprehending the broader impact of the crisis and the subsequent regulatory reforms that aimed to address the vulnerabilities exposed by these financial instruments.

Understanding Credit Default Swaps

To truly comprehend the significance of Credit Default Swaps (CDS), it’s essential to delve into their mechanics. At its core, a CDS is a bilateral contract between two parties, the buyer and the seller. The buyer, seeking protection against the risk of a default on a particular debt instrument, pays a periodic fee, known as the premium, to the seller. In return, the seller agrees to compensate the buyer in the event of a default.

Credit Default Swaps are not limited to traditional bonds; they can be based on a variety of underlying assets, including corporate bonds, mortgage-backed securities, and sovereign debt. This versatility contributed to the widespread use of CDS across different sectors of the financial markets.

One of the defining features of CDS is their potential for leverage. Unlike traditional insurance, where the buyer must possess an insurable interest in the underlying asset, CDS can be bought without any direct connection to the referenced debt. This characteristic opened the door for speculative trading, as investors could purchase CDS contracts on assets in which they had no vested interest, essentially creating a form of side bet on the likelihood of default.

The proliferation of CDS contracts also introduced the concept of “naked” credit default swaps, where the buyer does not hold the underlying asset being insured. This speculative practice drew criticism for its potential to artificially inflate the perceived risk of a particular entity’s debt, leading to increased market volatility and systemic risk.

Furthermore, the lack of transparency in the CDS market posed challenges for regulators and market participants. Unlike exchange-traded instruments, CDS transactions were predominantly conducted over-the-counter (OTC), making it difficult to assess the overall exposure and interconnectedness of market participants. This opacity amplified the challenges in gauging the systemic implications of a widespread default event.

As the financial crisis unfolded, the intricate web of Credit Default Swaps became a focal point of scrutiny, shedding light on the complexities and vulnerabilities embedded in these financial instruments. The role of CDS in amplifying the impact of the crisis underscored the need for greater transparency, oversight, and risk management in the realm of derivatives trading.

The Role of Credit Default Swaps in the Meltdown

The financial meltdown of 2008 sent shockwaves through global markets, and the role of Credit Default Swaps (CDS) in exacerbating the crisis cannot be overstated. As the housing market bubble burst and mortgage-backed securities faced mounting defaults, the interconnected web of CDS contracts magnified the impact of these events, contributing to the severity of the meltdown.

One of the critical aspects of CDS that amplified the crisis was the widespread use of these instruments to hedge exposure to mortgage-backed securities. Financial institutions, including banks and insurance companies, had accumulated significant holdings of mortgage-related assets, seeking to profit from the housing boom. To mitigate the associated risks, they turned to CDS as a means of insuring against potential defaults on these assets.

However, the sheer volume of CDS contracts tied to mortgage-backed securities created a precarious situation. When the underlying mortgages began to default at an alarming rate, the sellers of these CDS found themselves facing substantial liabilities. This triggered a chain reaction, as the sellers struggled to fulfill their obligations, leading to concerns about their solvency and further exacerbating market uncertainty.

Furthermore, the opaque nature of the CDS market added a layer of complexity to the crisis. With many CDS contracts traded over-the-counter, the true extent of exposure and interconnectedness among financial institutions remained obscured. This lack of transparency heightened concerns about counterparty risk and the potential domino effect of defaults, amplifying the sense of systemic instability.

The interconnectedness of financial institutions through CDS contracts also contributed to contagion, as the distress in one sector spilled over into others. As the crisis unfolded, the interconnected web of CDS amplified the transmission of risk throughout the financial system, leading to widespread panic and a loss of confidence in the stability of major institutions.

The role of Credit Default Swaps in the meltdown underscored the need for enhanced regulation and oversight of derivative markets. The subsequent regulatory reforms aimed to address the systemic vulnerabilities exposed by CDS and other complex financial instruments, emphasizing the importance of transparency, risk management, and accountability in the realm of derivatives trading.

Conclusion

The intricate and often contentious role of Credit Default Swaps (CDS) in the financial meltdown of 2008 serves as a stark reminder of the complexities and vulnerabilities inherent in the world of derivatives trading. These financial instruments, initially designed to hedge against credit risk, evolved into powerful and interconnected tools that amplified the impact of the crisis, contributing to widespread market turmoil and systemic instability.

Understanding the mechanics of CDS is crucial in comprehending the events that unfolded during the crisis. The speculative nature of these instruments, coupled with their potential for leverage and lack of transparency, created a volatile environment that exacerbated the fallout from the housing market collapse. The interconnected web of CDS contracts tied to mortgage-backed securities magnified the risks, leading to a cascading effect that reverberated throughout the global financial system.

The aftermath of the crisis prompted a reevaluation of the regulatory framework governing derivatives markets. The need for greater transparency, oversight, and risk management became apparent, leading to regulatory reforms aimed at addressing the systemic vulnerabilities exposed by CDS and other complex financial instruments. Enhanced regulatory scrutiny and efforts to promote central clearing and reporting of derivative transactions sought to mitigate the risks associated with these instruments and bolster market resilience.

While the role of Credit Default Swaps in the meltdown exemplified the potential for financial innovation to outpace regulatory safeguards, it also underscored the imperative of adapting regulatory frameworks to evolving market dynamics. The lessons learned from the crisis have prompted a renewed focus on risk management, transparency, and accountability, shaping a more robust and resilient financial landscape.

In essence, the story of Credit Default Swaps and their impact on the financial meltdown serves as a cautionary tale, highlighting the delicate balance between financial innovation and risk management. By understanding the complexities and implications of these instruments, market participants and regulators can strive to foster a more stable and transparent financial ecosystem, better equipped to navigate the challenges of an ever-evolving global economy.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance