Home>Finance>What Are Some Key Components Of Successful Budgeting

Finance

What Are Some Key Components Of Successful Budgeting

Published: October 11, 2023

Discover the essential components of successful budgeting, including finance strategies and tips for effective financial planning.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Clear Financial Goals

- Detailed Expense Tracking

- Accurate Income Projection

- Assessing and Prioritizing Expenses

- Creating Realistic Budgetary Categories

- Regular Monitoring and Adjustments

- Emergency Fund Allocation

- Debt Management

- Savings and Investment Strategies

- Involving and Communicating with all Stakeholders

- Conclusion

Introduction

Budgeting is a crucial aspect of personal and financial management. Whether you are an individual, a family, or a business, having a well-thought-out budget is essential for achieving financial success. A budget helps you track your income and expenses, make informed financial decisions, and ensure that you are living within your means.

While budgeting may seem daunting at first, it is a skill that can be learned and mastered. By implementing key components of successful budgeting, you can take control of your finances and work towards your financial goals.

In this article, we will explore some of the essential components of successful budgeting and how they can contribute to your financial well-being. From setting clear financial goals to effectively managing debt, these components will guide you towards making informed financial decisions and achieving financial stability.

Before we delve into the details, it’s important to note that budgeting is not about restricting yourself or depriving yourself of the things you enjoy. Instead, it is about prioritizing your financial goals and aligning your spending with those goals. It’s about being intentional with your money and making choices that support your long-term financial health.

So, without further ado, let’s explore the key components of successful budgeting that can help you take control of your financial future.

Clear Financial Goals

Setting clear financial goals is the foundation of successful budgeting. Without clear goals, it becomes challenging to prioritize your expenses and make informed financial decisions. When setting your financial goals, it’s important to be specific, measurable, achievable, relevant, and time-bound (SMART).

Start by identifying what you want to achieve financially. Do you want to save for a down payment on a house, pay off your student loans, or build a retirement nest egg? Once you have a clear understanding of your goals, break them down into smaller milestones. For example, if your goal is to save for a down payment on a house, break it down into how much you need to save each month or year to reach that goal within a specific timeframe.

Having clear financial goals helps you prioritize your spending and make intentional choices. It becomes easier to differentiate between needs and wants, as you align your expenses with your goals. For example, if your goal is to pay off your student loans, you might choose to cut down on discretionary expenses like eating out or entertainment and allocate those funds towards your debt repayment.

Regularly review and revise your financial goals as your circumstances change. As you make progress towards your goals, celebrate your achievements and set new goals to continue your financial journey.

By having clear financial goals, you have a roadmap for your budgeting efforts. It provides you with motivation and direction, making it easier to stay focused and committed to your financial plan.

Detailed Expense Tracking

One of the key components of successful budgeting is keeping a detailed track of your expenses. This involves diligently recording and categorizing every expenditure you make, no matter how small.

Expense tracking allows you to gain a deeper understanding of where your money is going and helps you identify areas where you can potentially cut back or make adjustments. It also helps you identify any spending patterns or habits that may be hindering your financial progress.

There are various methods you can use to track your expenses, depending on your preference and convenience. You can use a budgeting app or software, create a spreadsheet, or simply use a pen and paper. The key is to track your expenses consistently and accurately.

When tracking your expenses, be sure to include all categories, such as housing, transportation, groceries, utilities, entertainment, and miscellaneous expenses. It’s important to allocate a specific category for each expense to get a comprehensive overview of your spending habits.

Reviewing your expenses regularly can help you identify areas where you may be overspending or areas where you can potentially save. For example, if you notice that you are spending a significant amount on dining out, you can make a conscious effort to cook more meals at home and reduce your restaurant expenses.

Remember, the goal of tracking your expenses is not to restrict yourself unnecessarily, but rather to gain awareness and make informed decisions about your spending. It will enable you to prioritize your expenses based on your financial goals and make adjustments where needed.

By diligently tracking your expenses, you will have a clearer picture of your financial situation and be better equipped to create a realistic and effective budget.

Accurate Income Projection

When it comes to budgeting, accurately projecting your income is crucial. Your income serves as the foundation for your budget and determines how much you can allocate towards your various expenses and financial goals.

To create an accurate income projection, start by analyzing your sources of income. This can include your salary, freelance work, rental income, dividends, or any other income streams you may have. If you have irregular or variable income, it’s essential to consider an average or conservative estimate to account for any fluctuations.

Additionally, it’s important to consider any upcoming changes or fluctuations in your income. For example, if you anticipate a salary increase, bonus, or commission, factor that into your projection. On the other hand, if you expect a reduction in income due to job loss, career change, or transition, account for those changes as well.

Once you have a clear understanding of your income sources and potential changes, create a monthly or annual income projection. This projection will help you determine your available funds for budgeting purposes.

It’s important to be realistic when projecting your income. Overestimating your income can lead to financial strain and potentially derail your budget. On the other hand, underestimating your income may prevent you from maximizing your financial potential and achieving your goals.

Regularly review and update your income projection as needed. If your income changes or if there are unexpected fluctuations, adjust your budget accordingly to ensure that it remains aligned with your financial goals.

Remember, accurate income projection is essential for effective budgeting. It provides you with a clear understanding of your financial resources and allows you to allocate your money wisely and strategically.

Assessing and Prioritizing Expenses

Assessing and prioritizing expenses is a crucial component of successful budgeting. It involves evaluating your expenses, categorizing them based on importance and necessity, and making informed decisions about how to allocate your funds.

Start by categorizing your expenses into essential and non-essential categories. Essential expenses are those that are necessary for your basic needs and financial obligations, such as housing, utilities, food, transportation, and debt payments. Non-essential expenses, on the other hand, are discretionary expenses that are not crucial for your survival or financial well-being, such as entertainment, dining out, or luxury purchases.

Once you have categorized your expenses, it’s time to prioritize them. Prioritization is about identifying the expenses that are most important and aligning them with your financial goals. Consider your financial objectives, such as saving for a down payment, paying off debt, or building an emergency fund, and allocate your resources accordingly.

When assessing your expenses, also look for areas where you can potentially reduce or eliminate costs. For example, review your utility bills and explore energy-saving measures, such as using LED lights or adjusting your thermostat. Look for ways to cut back on discretionary expenses, such as reducing your entertainment budget or finding more affordable alternatives.

However, it’s important to strike a balance between cutting expenses and maintaining a reasonable quality of life. Budgeting is not about depriving yourself excessively, but rather about making choices that align with your financial goals and values.

Regularly review and reassess your expenses to ensure that they continue to align with your financial priorities. Adjust your budget as needed to accommodate any changes in income, expenses, or financial goals.

By assessing and prioritizing your expenses, you can make intentional decisions about how to allocate your resources. This ensures that your spending aligns with your financial goals and helps you move closer towards achieving financial stability and success.

Creating Realistic Budgetary Categories

Creating realistic budgetary categories is an important step in effective budgeting. It involves breaking down your expenses into specific categories to provide structure and organization to your budget.

When creating budgetary categories, it’s important to be comprehensive and specific. Start by listing all your regular expenses, such as housing, transportation, groceries, utilities, and insurance. Then, consider other expenses that may occur less frequently but still need to be accounted for, such as car maintenance, medical bills, or holiday expenses.

It’s also important to anticipate and allocate funds for irregular expenses. These are expenses that do not occur monthly but are still significant, such as annual car insurance premiums or property taxes. By including these irregular expenses in your budget and setting aside money each month, you can avoid financial surprises and plan for them in advance.

Consider organizing your budgetary categories in a way that makes sense for you. You can group similar expenses together, such as all housing-related expenses or all transportation expenses. This will make it easier to track and manage your spending in each category.

While creating your budgetary categories, it’s essential to be realistic about your expenses. Avoid overestimating or underestimating your spending. If you are unsure about certain expenses, it’s better to err on the side of caution and allocate a realistic amount.

Regularly review and adjust your budgetary categories as needed. As your financial situation changes or new expenses arise, update your budget to reflect those changes. Flexibility is key in ensuring that your budget remains accurate and effective.

Remember, creating realistic budgetary categories helps you gain a clear understanding of your expenses and allows you to allocate your funds in a purposeful manner. It provides a framework for your budget and helps you make more informed financial decisions.

Regular Monitoring and Adjustments

Regular monitoring and adjustments are crucial components of successful budgeting. It’s not enough to create a budget and then forget about it. To ensure its effectiveness, you need to actively monitor and make necessary adjustments along the way.

Schedule regular check-ins with your budget to review your income, expenses, and progress towards your financial goals. This can be done weekly, bi-weekly, or monthly, depending on your preference and the level of detail you want to track. During these check-ins, compare your actual spending with your budgeted amounts and identify any discrepancies or areas where you may have overspent.

If you find that you are consistently overspending in certain categories, it may be necessary to make adjustments. Look for areas where you can cut back or find more cost-effective alternatives. For example, if you are consistently exceeding your food budget, consider meal planning, cooking at home, or buying in bulk to reduce costs.

Similarly, if you find yourself consistently underspending in certain categories, you may be able to re-allocate those funds towards other financial goals or expenses that may need additional funding.

Regular monitoring also helps you stay accountable and make course corrections, if necessary. It allows you to spot any deviations from your financial plan and take proactive steps to get back on track.

As you progress on your financial journey, your circumstances, goals, and income may change. Be prepared to adjust your budget accordingly. Whether it’s a job change, a pay raise, or a change in your financial goals, your budget should adapt to accommodate these changes.

Remember, your budget is not set in stone. It should be a dynamic tool that evolves with your life and financial situation.

By regularly monitoring your budget and making necessary adjustments, you can stay on top of your finances and ensure that your budget remains an effective tool for managing your money and achieving your financial goals.

Emergency Fund Allocation

An emergency fund is a crucial component of financial stability and should be included in any comprehensive budget. It serves as a safety net during unexpected events or financial emergencies, providing you with peace of mind and protecting you from accumulating debt.

When it comes to allocating funds for your emergency fund, the general recommendation is to aim for three to six months’ worth of living expenses. This amount will vary depending on your personal circumstances, such as your monthly expenses, income stability, and the level of risk in your profession.

Start by calculating your monthly expenses, including fixed costs like rent or mortgage, utilities, insurance, and groceries, as well as variable expenses such as entertainment or dining out. Multiply this monthly expense amount by the number of months you want to save for in your emergency fund.

As you allocate funds for your emergency fund, prioritize it above other non-essential expenses. Consider automating your savings by setting up automatic transfers from your income to your emergency fund, making it easier to consistently contribute towards this important goal.

It’s crucial to keep your emergency fund separate from your day-to-day spending account. Consider opening a high-yield savings account or a designated emergency fund account to ensure that the funds are easily accessible when needed, but not tempting to spend on non-emergency items.

Keep in mind that the purpose of the emergency fund is to provide financial security in times of unexpected events, such as medical emergencies, job loss, or major car repairs. It’s important to replenish the funds if you ever need to dip into it.

Once you have successfully built your emergency fund, regularly review and reassess the amount. Life circumstances change, and what may have been sufficient in the past may no longer be adequate. Take into account any changes in income, expenses, or family situations, and adjust the size of your emergency fund as necessary.

Remember, having a well-funded emergency fund is essential for long-term financial stability. It provides a cushion during unexpected events and allows you to navigate challenging times without relying on credit cards or loans.

Debt Management

Debt can be a significant obstacle to achieving financial stability and reaching your goals. That’s why effective debt management is a crucial component of successful budgeting. It involves strategies to pay off existing debt, avoid accumulating new debt, and improve your overall financial health.

Start by taking an inventory of your debts. Make a list of all your outstanding loans, credit card balances, and any other form of debt you may have. Include details such as interest rates, minimum monthly payments, and repayment terms.

Once you have a clear picture of your debts, prioritize them based on factors such as interest rates, outstanding balances, and repayment terms. Consider focusing on high-interest debts first, as they tend to have a bigger impact on your overall financial situation.

Develop a debt repayment plan that aligns with your budget and financial goals. This may involve making larger payments towards your highest interest debts while paying the minimums on others, or employing a debt snowball or debt avalanche method.

Set realistic and achievable goals for paying off your debt. Break down your debt repayment plan into smaller milestones, and celebrate each achievement along the way. This will help keep you motivated and on track.

As you work towards paying off your debt, it’s important to avoid accumulating new debt. Review your spending habits and identify any patterns or triggers that lead to excessive borrowing. Adopt strategies to curb impulse spending and prioritize needs over wants.

Consider seeking professional help if you find yourself overwhelmed by debt. A credit counselor or financial advisor can provide guidance and advice tailored to your specific situation.

In addition to debt repayment, consider exploring opportunities to refinance or consolidate your debt to potentially save on interest payments. However, carefully evaluate the terms and fees associated with these options to ensure they are beneficial in the long run.

Lastly, as you manage your debt, be patient with yourself. It may take time to become debt-free, but with consistent effort and discipline, you can achieve your goal.

Remember, effective debt management is essential for long-term financial stability. By prioritizing debt repayment and being proactive in managing your finances, you can regain control over your financial future and pave the way towards a debt-free life.

Savings and Investment Strategies

Building savings and implementing investment strategies are vital components of successful budgeting. They help you grow your wealth, achieve long-term financial goals, and secure your future. Here are some key considerations for effective savings and investment strategies.

1. Establish an Emergency Fund: As mentioned earlier, having an emergency fund is crucial. Set aside a portion of your income each month into a separate account to cover unexpected expenses or financial setbacks.

2. Prioritize Retirement Savings: Start saving for retirement early and consistently. Take advantage of employer-sponsored retirement plans, such as 401(k)s or pension schemes. If available, maximize contributions to benefit from employer matching programs.

3. Determine Risk Tolerance: Assess your risk tolerance based on your financial goals, time horizon, and comfort level. Determine the right balance between low-risk and high-risk investments to achieve your desired returns while managing potential volatility.

4. Diversify Your Investments: Spread your investments across different asset classes such as stocks, bonds, mutual funds, or real estate. Diversification helps mitigate risk by avoiding overexposure to any single investment.

5. Set Clear Saving Goals: Define short-term and long-term saving goals. Whether it’s saving for a vacation, a down payment, or a child’s education, set specific goals and allocate funds accordingly in your budget.

6. Automate Savings: Establish automatic transfers to a separate savings account. This ensures consistent savings by consistently setting aside a predetermined amount of money each month.

7. Monitor and Adjust Investments: Regularly review and reassess your investment portfolio. As your financial goals or market conditions change, make appropriate adjustments to ensure your investments remain aligned with your objectives.

8. Seek Professional Advice: Consider consulting a financial advisor who can provide personalized guidance based on your financial situation, goals, and risk tolerance. They can help you develop an investment strategy that best suits your needs.

9. Educate Yourself: Take the time to educate yourself about different investment options, strategies, and potential risks. This knowledge empowers you to make informed decisions and take control of your financial future.

10. Stay Committed: Building wealth takes time and consistency. Stay committed to your savings and investment goals, even during periods of market volatility. Stick to your plan and avoid making emotional decisions based on short-term market fluctuations.

Remember, savings and investment strategies are essential for long-term financial success. By diligently saving, diversifying your investments, and staying committed to your financial goals, you can grow your wealth and secure a brighter financial future.

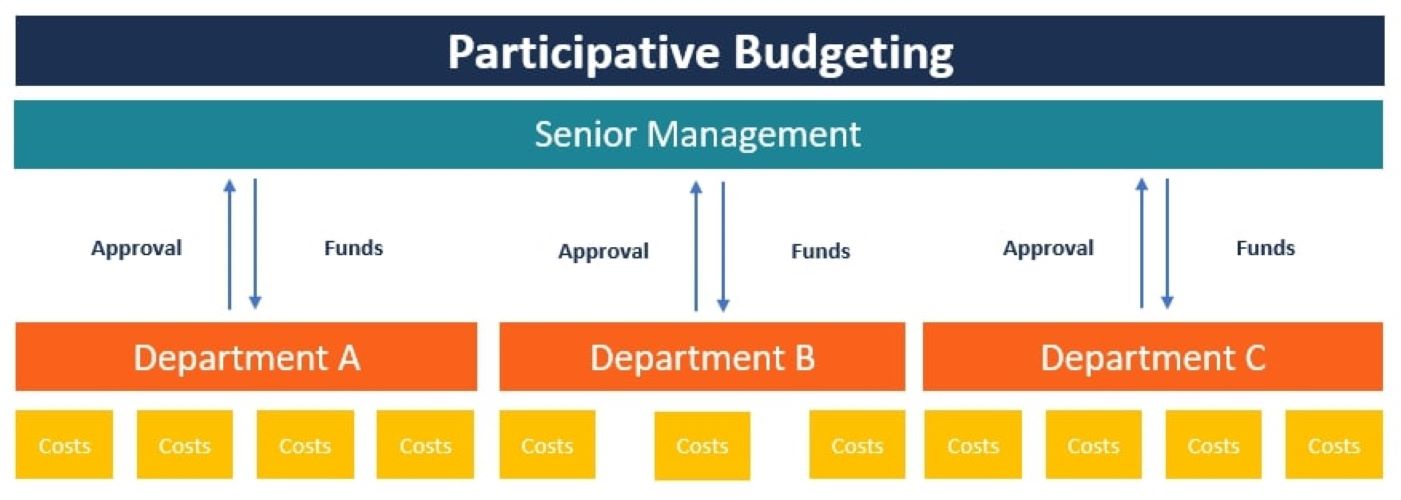

Involving and Communicating with all Stakeholders

Effective budgeting extends beyond your individual efforts. It involves involving and communicating with all relevant stakeholders who may be impacted by your financial decisions. This includes family members, partners, or business associates. Here’s why involving and communicating with stakeholders is important for successful budgeting.

1. Shared Accountability: By involving others in your budgeting process, you create a sense of shared responsibility and accountability. This can be particularly important in a family setting, where everyone’s financial well-being is interconnected.

2. Open and Transparent Communication: Regular, open, and transparent communication is key to ensuring that everyone is on the same page regarding financial goals, priorities, and constraints. It allows for better decision-making, avoids misunderstandings, and promotes unity.

3. Collaborative Decision-Making: Involving stakeholders in the budgeting process allows for collaborative decision-making. It provides an opportunity for everyone to have a voice, share their perspectives, and contribute their ideas. This fosters a sense of ownership and increases the likelihood of successful implementation.

4. Clarification of Financial Expectations: Different stakeholders may have varying financial expectations or priorities. By involving and communicating with all parties, you can gain a better understanding of these expectations, bridge any gaps, and work towards common financial goals.

5. Identification of Shared Goals and Priorities: Through discussions and conversations, you can identify shared financial goals and priorities. This allows you to align your budgeting efforts and focus resources on what matters most to all the stakeholders involved.

6. Agreement on Financial Boundaries: Involving stakeholders in the budgeting process helps establish clear financial boundaries. It sets expectations for spending limits, savings goals, and investment decisions, ensuring that everyone is aware of the limitations and constraints in place.

7. Building Trust: Open and inclusive communication builds trust among stakeholders. It creates an environment where everyone feels heard, valued, and included. Trust is essential for effective collaboration and long-term financial success.

8. Flexibility and Adaptability: Involving stakeholders enables you to adapt your budget to evolving circumstances or changing needs. It allows for flexibility in adjusting financial plans, reallocating resources, or making necessary revisions as situations change.

9. Teaching Financial Responsibility: Involving children or younger family members in budgeting discussions helps teach them financial responsibility and money management skills. It builds their financial literacy and fosters a healthy relationship with money from an early age.

10. Celebrating Milestones Together: Involving stakeholders in the budgeting process allows for shared celebrations when financial milestones are achieved. It reinforces a sense of progress, accomplishment, and unity in working towards shared financial success.

Remember, involving and communicating with all stakeholders is a key component of successful budgeting. It promotes accountability, collaboration, and unity, and helps ensure that everyone is aligned towards common financial goals.

Conclusion

Effective budgeting is a foundational pillar of financial success. By incorporating key components into your budgeting process, you can take control of your finances, work towards your goals, and achieve long-term stability.

In this article, we explored several important elements of successful budgeting. We learned the significance of setting clear financial goals as a roadmap for your budget, tracking and categorizing expenses to gain insights into your spending habits, and accurately projecting your income to allocate funds wisely.

We also emphasized the importance of assessing and prioritizing expenses to align your spending with your goals, creating realistic budgetary categories to provide structure and organization, and regularly monitoring and adjusting your budget to stay on track.

Additionally, we explored the crucial components of allocating funds for emergency savings, managing debt effectively to improve your financial health, and implementing savings and investment strategies to build wealth for your future.

Lastly, we highlighted the significance of involving and communicating with all stakeholders, promoting shared responsibility, collaboration, and unity in pursuing financial goals together.

Remember, successful budgeting requires discipline, commitment, and adaptability. It’s an ongoing process that requires regular review, adjustments, and open communication with all those affected by your financial decisions.

By applying these key components of successful budgeting, you can take control of your finances, reduce financial stress, and make progress towards your financial goals. Whether it’s becoming debt-free, saving for a down payment, or securing a comfortable retirement, budgeting will be your ally in achieving financial success.

Start implementing these components today and watch as your financial well-being improves and your dreams become tangible realities.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance