Home>Finance>What Are The Stipulations For Joining A Credit Union

Finance

What Are The Stipulations For Joining A Credit Union

Published: January 5, 2024

Learn about the prerequisites for becoming a member of a credit union and get the financial benefits you need. Discover how joining a credit union can improve your finances.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When looking for financial solutions, many individuals turn to traditional banks. However, credit unions offer a viable alternative that often comes with unique advantages. Credit unions are not-for-profit financial institutions that are owned and operated by their members. This cooperative structure enables credit unions to provide a wide range of financial services to their members, including savings accounts, loans, and credit cards.

Joining a credit union requires meeting certain eligibility criteria and fulfilling specific membership requirements. While requirements may vary from one credit union to another, there are some common stipulations that prospective members need to be aware of.

In this article, we will explore the stipulations for joining a credit union and the steps involved in the application process. We will discuss criteria such as identification and documentation, financial standing, geographic location, and employment or affiliation. Additionally, we will highlight the benefits of joining a credit union and why it may be a preferable option for your financial needs.

It is important to note that credit unions prioritize serving their members and promoting financial well-being, rather than maximizing profits. This commitment to their members is what sets credit unions apart from traditional banks and why many individuals choose to become members of these unique financial institutions.

Eligibility Criteria

To become a member of a credit union, you must meet certain eligibility criteria. These criteria determine whether you qualify for membership based on specific factors such as location, occupation, or affiliation. While the eligibility requirements may differ between credit unions, here are some common criteria to consider:

- Geographic Location: Many credit unions serve a specific geographic area, such as a city, county, or state. To be eligible for membership, you typically need to live or work within the credit union’s defined geographic boundaries.

- Occupation or Affiliation: Some credit unions are formed to serve individuals who share a common occupation or affiliation, such as employees of a particular company, members of a certain organization, or residents of a specific community. You may need to provide proof of your employment or affiliation to meet the eligibility criteria.

- Familial Connections: Credit unions often extend membership to immediate family members (spouses, children, siblings, parents) of current members. If you have a family member who is already a member, you may be eligible to join as well.

- Membership in a Specific Group: Certain credit unions are associated with specific groups, such as military personnel, veterans, or educators. If you belong to one of these groups, you may be eligible to join a credit union that caters to your profession or affiliation.

It is important to research and identify credit unions that align with your eligibility criteria. This will increase your chances of finding a credit union that suits your financial needs and offers the services you require.

Furthermore, some credit unions have open membership policies that allow anyone to join even if they do not meet the traditional eligibility criteria. This can include credit unions that serve a specific community or have a social mission. Checking with local credit unions or credit union associations can help you discover if there are alternative membership options available.

Once you have determined that you meet the eligibility criteria for a credit union, you can move forward with the membership application process. Understanding the requirements and documentation needed for membership is crucial to ensuring a smooth and successful application process.

Membership Requirements

To become a member of a credit union, you need to fulfill certain membership requirements. These requirements are put in place to establish your eligibility and ensure that you meet the necessary qualifications. While the specific requirements may vary between credit unions, there are some common aspects to consider:

- Identification and Documentation: Like any financial institution, credit unions require proper identification and documentation to verify your identity and establish your eligibility. This typically includes a valid government-issued identification card (such as a driver’s license or passport) and proof of address (such as a utility bill or lease agreement).

- Financial Standing: Credit unions may also evaluate your financial standing to determine your eligibility for membership. They may request information such as income verification, employment history, or credit history. The purpose of this evaluation is to ensure that you are financially responsible and capable of utilizing the credit union’s services.

- Minimum Age Requirement: Some credit unions have a minimum age requirement for membership. This is often set at 18 years old or older. However, there may be special membership options available for minors, such as youth accounts or custodial accounts.

- Membership Fees: While credit unions are known for their competitive fees and low-cost services, some may require an initial membership fee or an annual membership fee. This fee is typically nominal and contributes to the credit union’s operational expenses.

It is important to understand the specific membership requirements of the credit union you wish to join, as this will enable you to gather the necessary documents and fulfill the necessary obligations. Many credit unions provide clear information about their membership requirements on their websites or by contacting their member services department.

Once you have gathered the required documentation and met the membership requirements, you are ready to proceed with the application process. The application process may vary between credit unions, but it generally involves completing an application form and submitting the required documents for review.

By fulfilling the membership requirements, you are taking the first step towards becoming a member of a credit union and gaining access to the many benefits they offer.

Identification and Documentation

When applying for membership with a credit union, you will be required to provide proper identification and documentation to verify your identity and establish your eligibility. This step is crucial in ensuring the security and integrity of the credit union’s membership base. Here are the common forms of identification and documentation that credit unions typically require:

- Government-Issued Identification: The most common form of identification required by credit unions is a government-issued identification card. This can be a driver’s license, passport, or any other identification document issued by a recognized government agency. The identification document should contain your photograph, full name, date of birth, and signature.

- Proof of Address: Credit unions may also request proof of your residential address to verify your eligibility. This can be a recent utility bill, lease agreement, or bank statement that clearly displays your name and residential address. The document should be dated within the past three months.

- Social Security Number: The credit union may require your social security number, which is used for identification and tax reporting purposes. You will need to provide your social security card or other official documents that contain your social security number.

- Employment or Income Verification: Some credit unions may require you to provide documentation to verify your employment or income. This can include recent pay stubs, tax returns, or employment verification letters. The purpose of this verification is to assess your financial stability and determine your creditworthiness.

- Additional Documentation: Depending on the specific requirements of the credit union, you may be asked to provide additional documentation. This can include proof of citizenship or legal residency, marriage certificates for spousal membership, or birth certificates for minor membership applications.

It is essential to ensure that all the documents provided are valid, current, and accurate. Any discrepancies or inaccuracies in the documentation can delay the membership application process. It is advisable to contact the credit union beforehand to obtain a clear understanding of their identification and documentation requirements.

Protecting the privacy and security of your personal information is a top priority for credit unions. They have stringent measures in place to safeguard your data and comply with applicable privacy laws and regulations.

By providing the required identification and documentation, you demonstrate your commitment to joining the credit union and gain access to the wide range of financial services and benefits they offer.

Financial Standing

When applying for membership at a credit union, your financial standing may be evaluated to determine your eligibility. Credit unions have a responsibility to ensure that their members are financially responsible and capable of utilizing the services they offer. While the specific criteria may vary between credit unions, here are some common aspects of financial standing that may be assessed:

- Income Verification: Credit unions may require you to provide documentation to verify your income. This can include recent pay stubs, tax returns, or bank statements. The purpose of income verification is to assess your ability to meet financial obligations and determine your creditworthiness.

- Debt-to-Income Ratio: Credit unions may evaluate your debt-to-income ratio, which compares your monthly debt obligations to your income. This information helps determine your ability to manage additional financial commitments and make loan payments on time.

- Credit History: Your credit history may be reviewed to assess your financial responsibility and lending risk. This can be done through a credit report obtained from a credit bureau. Credit unions typically consider factors such as your payment history, outstanding debts, and length of credit history.

- Savings and Assets: Some credit unions may consider your savings and assets when evaluating your financial standing. This can include your existing savings accounts, investments, real estate, or other valuable possessions. Having substantial savings or assets can demonstrate financial stability and contribute to a positive evaluation.

It is important to note that credit unions have a more personalized approach to assessing financial standing compared to traditional banks. They consider factors beyond credit scores and are often more willing to work with members who may not have a perfect credit history.

If you have had financial challenges in the past, such as bankruptcy or late payments, it is still worth exploring membership with a credit union. They may take into account factors such as the length of time since the financial difficulty and your current financial situation.

Having strong financial standing can enhance your chances of being accepted as a member, especially for certain types of loans or credit products. However, even if your financial standing is not considered strong, credit unions are more likely to provide guidance and support to help you improve your financial situation.

By assessing your financial standing, credit unions aim to ensure that their members can responsibly utilize the financial services they offer while promoting financial well-being and stability.

Geographic Location

The geographic location is an important consideration when it comes to joining a credit union. Many credit unions have specific membership criteria based on a defined geographic area. The purpose of such criteria is to serve a specific community or locality and promote local financial well-being. Here are some key points to understand about geographic location requirements:

Serving a Specific Area: Some credit unions serve a particular city, county, or state. To become a member, you generally need to live or work within the credit union’s defined service area. This ensures that the credit union can effectively serve and meet the needs of its community.

Community-Chartered Credit Unions: Community-chartered credit unions have expanded geographic boundaries and can serve a broader area. These credit unions may have eligibility requirements based on a specific community, such as a neighborhood, school district, or a common interest shared by the residents.

Shared Branching and ATM Networks: Even if the credit union’s physical branches are limited to a specific geographic area, many credit unions participate in shared branching and ATM networks. This allows you to access your account and conduct transactions at other credit union locations across the country, providing a wider range of banking services when you are outside your credit union’s service area.

Online Banking: In the digital era, many credit unions offer online banking services, allowing members to access their accounts and perform transactions remotely. This can be particularly useful if you are unable to visit a physical branch due to geographic constraints. Check if the credit union you are interested in offers robust online banking services to ensure convenient access to your accounts.

Researching Local Credit Unions: If you have specific geographic requirements or preferences, it is advisable to research credit unions in your area. This can be done by checking online directories, contacting local credit union associations, or simply searching for credit unions in your locality. Exploring local credit unions can help you find options that align with your geographic criteria.

Understanding the geographic location requirements of the credit union you are interested in is essential to determine your eligibility. It ensures that you can access the services and benefits offered by the credit union and establish a convenient banking relationship within your desired area.

Employment or Affiliation

One common requirement for joining a credit union is employment or affiliation with a specific organization or group. Credit unions often serve individuals who share a common occupation, industry, or affiliation, and require proof of this connection to qualify for membership. Here are some key points to understand about employment or affiliation requirements:

- Employee-Based Credit Unions: Some credit unions are established to cater to the employees of a particular company, organization, or industry. This means that membership is limited to individuals who work for the designated employer or within the specific field. Proof of employment, such as a pay stub or employment verification letter, may be required.

- Membership Organizations: Certain credit unions are affiliated with specific membership organizations, such as unions, professional associations, or clubs. To become a member of these credit unions, you may need to provide proof of your membership or association with the organization.

- Community-Based Credit Unions: Some credit unions serve a defined community or neighborhood. In such cases, membership may be open to individuals who reside or have a connection to the local area, even if they are not affiliated with a specific organization. Proof of residency, such as a utility bill or lease agreement, may be required.

- Family Membership: Credit unions often extend membership eligibility to immediate family members of current members. This means that if a family member is already a member of the credit union, you may qualify for membership as well. Proof of the family relationship, such as a birth certificate or marriage certificate, may be required.

It’s important to note that credit unions prioritize serving their specific employee groups or affinity organizations. This focus allows them to tailor their financial products and services to meet the unique needs and challenges faced by these communities.

If you are unsure whether your employment or affiliation can make you eligible for a specific credit union, it’s recommended to reach out to the credit union directly or check their website for information on membership requirements. They will be able to clarify any questions you may have and guide you through the application process.

By fulfilling the employment or affiliation requirements, you are gaining access to a credit union that understands your specific financial situation and can provide tailored services and support. This affiliation can contribute to a mutually beneficial relationship between you and the credit union.

Application Process

The application process for joining a credit union is typically straightforward and can be completed in a few simple steps. While the specific process may vary between credit unions, here is a general overview of what to expect:

- Research and Select: Begin by researching credit unions that align with your eligibility criteria, such as geographic location, employment or affiliation requirements, and any other specific considerations. Consider factors such as the range of services offered, fees, and member benefits.

- Contact the Credit Union: Once you have identified a credit union that you are interested in, reach out to them directly to inquire about membership. You can call their member services department, visit their website, or even stop by one of their branches if applicable.

- Obtain and Complete Application Form: The credit union will provide you with an application form, either in person, through mail, or as a downloadable form from their website. Complete the application form accurately and thoroughly, providing all requested information.

- Submit Required Documentation: Along with the application form, you will need to submit any required documentation to verify your eligibility. This can include identification, proof of address, employment verification documents, or any other relevant information.

- Application Review and Approval: The credit union will review your application and supporting documents to verify your eligibility and assess your financial standing. This process may take a few days to a couple of weeks, depending on the credit union’s processing time.

- Membership Acceptance and Account Setup: If your application is approved, you will be notified of your membership acceptance. At this stage, you can proceed to set up your account and start utilizing the services offered by the credit union. This may involve depositing funds, applying for loans or credit cards, and accessing online banking services.

It’s vital to carefully review the application form, ensuring that all information provided is accurate and up to date. Any errors or omissions can delay the application process. If you have any questions or need guidance during the application process, don’t hesitate to reach out to the credit union’s member services department for assistance.

While credit unions strive to make the application process simple and accessible, it’s important to remember that meeting their eligibility criteria and providing the requested documentation is essential for a successful application.

By following the application process steps and providing all the necessary information, you can enjoy the benefits and services offered by the credit union and become an active member of their financial community.

Application Forms and Fees

When applying to join a credit union, you will be required to fill out an application form and, in some cases, pay applicable fees. These forms and fees are necessary to initiate the membership process and ensure your eligibility. Here’s what you need to know about application forms and fees:

Application Forms: The credit union will provide you with an application form that needs to be completed accurately and thoroughly. The form will typically require personal information such as your full name, contact details, social security number, employment details, and other relevant information. Some credit unions offer online application forms, while others may require you to fill out a physical form at a branch or mail it in.

Membership Fees: While credit unions typically offer competitive fees, some may require an initial membership fee or an annual membership fee. These fees contribute to the credit union’s operational expenses and are usually nominal. The specific fees, if any, will vary from credit union to credit union. It’s essential to check with the credit union regarding any fees associated with membership.

Fee Waivers: Many credit unions offer fee waivers for certain categories of membership, such as students or senior citizens. Some credit unions may also waive fees based on maintaining a minimum account balance or meeting specific transaction requirements. If you believe you may qualify for a fee waiver, inquire about it during the application process.

Additional Fees: Aside from the membership fee, there may be other fees associated with certain services or products offered by the credit union. These can include fees for checks, wire transfers, overdrafts, or late payments. It’s important to review the credit union’s fee schedule and terms and conditions to understand any potential additional fees that may apply.

It’s crucial to carefully read and understand all the terms and conditions associated with the application form and any fees involved. If you have any questions or need clarification, don’t hesitate to contact the credit union’s member services department for assistance.

Remember, the fees associated with credit union membership are typically lower compared to those of traditional banks, making them an appealing option for individuals seeking affordable financial services.

By completing the application form accurately and paying any necessary fees, you are demonstrating your commitment to becoming a member of the credit union. This paves the way for accessing the wide range of services and benefits that credit unions offer to their members.

Waiting Period

After submitting your application to join a credit union, there may be a waiting period before your membership is approved and officially granted. This waiting period allows the credit union to review your application, verify your eligibility, and conduct any necessary evaluations. Here’s what you need to know about the waiting period:

Processing Time: The length of the waiting period can vary depending on the credit union and their internal processes. Some credit unions may be able to process applications quickly, while others may take several days or weeks to complete the review. It’s advisable to inquire about the estimated processing time when you submit your application.

Evaluation and Verification: During the waiting period, the credit union will review your application form and supporting documentation to ensure that you meet the membership requirements. They may also conduct evaluations of your financial standing, such as reviewing your credit history or verifying your income. This thorough evaluation is done to assess your eligibility and ensure the security and integrity of the credit union’s membership base.

Communication: Throughout the waiting period, the credit union will keep you informed of the progress of your application. They will notify you if any additional information or documentation is required. If there are any delays or complications, the credit union will communicate with you to provide updates on the status of your membership application.

Membership Acceptance: Once the waiting period is over and your application is approved, you will be officially accepted as a member of the credit union. The credit union will notify you of your membership acceptance, typically through a welcome letter or email. This communication will provide instructions on how to proceed with setting up your account and accessing the services offered by the credit union.

The waiting period can be an exciting time as you anticipate becoming a member of the credit union and gaining access to its benefits and services. If you have any questions or concerns during the waiting period, you can reach out to the credit union’s member services department for clarification or assistance.

It’s important to note that credit unions strive to process applications efficiently and promptly, but the waiting period may be influenced by factors such as the volume of applications or the complexity of the review process. Patience and understanding are key during this phase of the membership application process.

By waiting patiently, you are taking the necessary steps to become part of the credit union community and enjoy the advantages of being a member, such as better rates, personalized service, and a focus on member well-being.

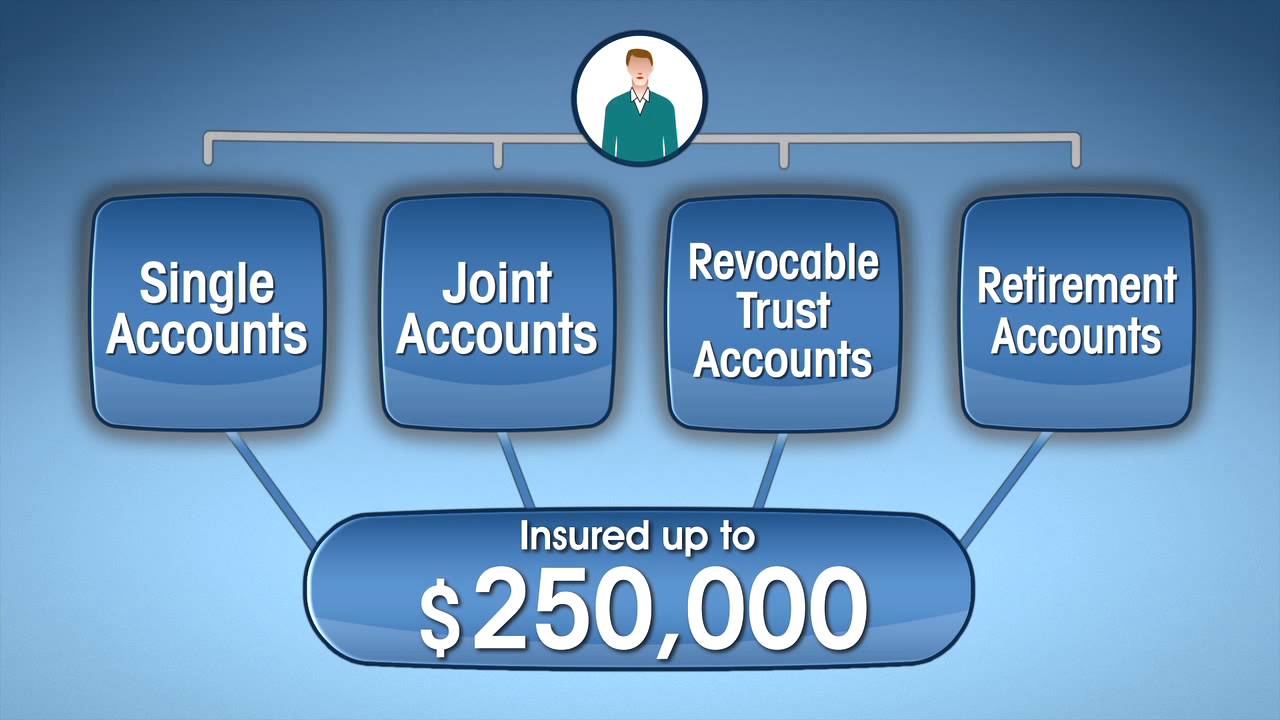

Account Ownership Options

When joining a credit union, you will have the opportunity to choose from various account ownership options. These options determine how your accounts are structured and who has access to them. Understanding the different ownership options available can help you make informed decisions on how to manage your finances within the credit union. Here are some common account ownership options:

- Individual Account: An individual account is solely owned by one person. This option is suitable if you want complete control and ownership of your account. You have the freedom to make transactions, access funds, and manage your finances independently.

- Joint Account: A joint account is shared by two or more individuals. It is a popular choice for couples, family members, or business partners who want equal access to the account and the ability to manage finances collectively. Each joint account holder has the same rights and responsibilities regarding the account.

- Trust Account: A trust account is designed for estate planning purposes. It allows you to designate beneficiaries who will receive the funds in the account upon your passing. Setting up a trust account can help protect and manage your assets for future generations.

- Custodial Account: A custodial account is established for a minor, typically managed by a parent or legal guardian. It allows the custodian to hold and manage funds on behalf of the minor until they reach a certain age. Custodial accounts aim to provide financial support and teach money management skills.

- Business Account: If you are a business owner, a credit union may offer business accounts tailored to meet your specific needs. Business accounts provide features such as checking, savings, and access to merchant services, allowing you to manage your business finances effectively.

Keep in mind that the availability of account ownership options may vary between credit unions. It’s important to discuss your specific needs with the credit union representative to ensure that they offer the appropriate account ownership options that suit your circumstances.

When deciding on account ownership, consider factors such as your financial goals, the level of control you desire, and the individuals or entities who require access to the account. It’s also essential to review the terms and conditions, fees, and any limitations associated with each ownership option.

By selecting the most suitable account ownership option, you can effectively manage your finances, accommodate shared financial responsibilities, and make informed decisions within the credit union.

Benefits of Joining a Credit Union

Joining a credit union offers numerous benefits that can enhance your financial well-being and provide a more personalized banking experience compared to traditional banks. Here are some compelling advantages of becoming a credit union member:

- Member-Owned and Non-Profit Structure: Unlike banks that prioritize shareholder profits, credit unions are member-owned and operated on a not-for-profit basis. This structure allows credit unions to prioritize their members’ financial well-being by offering competitive rates, low fees, and personalized services.

- Better Interest Rates and Lower Fees: Credit unions often offer more favorable interest rates on loans, credit cards, and savings accounts compared to traditional banks. Additionally, they tend to have lower fees and transaction costs, helping you save money in the long run.

- Personalized Service: Credit unions pride themselves on providing a higher level of personalized service to their members. You can expect a more personal touch, direct access to decision-makers, and financial guidance tailored to your specific needs and goals.

- Community Focus: Credit unions are deeply rooted in the communities they serve. They are committed to supporting local businesses, community projects, and charitable initiatives, fostering economic growth and social development within the community.

- Shared Branching and ATM Networks: Many credit unions participate in shared branching and ATM networks, allowing you to access your accounts and conduct transactions at other credit union locations across the country. This provides greater convenience and accessibility, especially when you are travelling or outside your credit union’s service area.

- Financial Education and Counseling: Credit unions often offer financial education programs and counseling services to help their members develop sound financial habits, improve credit scores, and make informed financial decisions. These resources can empower you to achieve your financial goals and improve your financial literacy.

- Member Voting Rights and Influence: As a credit union member, you have the right to vote in board elections and participate in the decision-making processes. This democratic structure allows you to have a voice in shaping the direction and policies of the credit union.

- Security and Privacy: Credit unions prioritize the security and privacy of their members’ information. They have stringent measures in place to safeguard your data, comply with privacy laws, and protect you from potential fraud or identity theft.

Joining a credit union not only provides financial benefits but also allows you to be part of a community-focused institution that operates in your best interest. The personalized service, lower fees, and commitment to member well-being make credit unions an appealing choice for individuals and families seeking a more rewarding and customer-centric banking experience.

By becoming a credit union member, you are joining a collective of individuals who are committed to helping each other thrive financially and making a positive impact in the community.

Conclusion

Joining a credit union offers a compelling alternative to traditional banking, providing a range of benefits that prioritize your financial well-being and foster a sense of community. Throughout this article, we have explored the stipulations for joining a credit union, including eligibility criteria, membership requirements, identification and documentation, financial standing, geographic location, and employment or affiliation.

By meeting the membership requirements and completing the application process, you can gain access to a wide range of financial services tailored to your needs. Credit unions offer competitive interest rates, lower fees, and personalized service, driven by their member-owned and non-profit structure.

Moreover, the community focus of credit unions sets them apart from traditional banks. Credit unions prioritize supporting local businesses, sponsoring community projects, and providing financial education resources. By joining one, you become part of a cooperative financial institution that aims to improve the well-being of its members and the local community.

While each credit union may have its specific stipulations and benefits, the core principles of member ownership, personalized service, and community focus remain consistent. Researching credit unions that align with your eligibility criteria and financial goals will help you find the right institution to meet your needs.

Ultimately, joining a credit union empowers you to have a voice in your financial future, benefit from competitive rates and fees, and receive personalized financial guidance. By supporting a credit union, you contribute to the strength and vibrancy of your community, fostering economic growth and social development.

So, whether you’re looking to open a savings account, obtain a loan, or utilize a credit card, consider joining a credit union. Experience the advantages it offers and become part of a financial institution that prioritizes its members’ interests and promotes financial well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance