Finance

What Is A 740 Credit Score

Published: October 21, 2023

Discover what a 740 credit score means and how it can impact your finances. Explore the benefits and opportunities this credit score can bring.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the world of personal finance, credit scores play a crucial role. Your credit score is a numerical representation of your creditworthiness, and it impacts your ability to secure loans, obtain favorable interest rates, and even rent an apartment or get a job. Understanding credit scores and how they work is essential for financial success.

One credit score that holds significant importance is the 740 credit score. This score is considered very good and puts you in a favorable position with lenders. It signifies responsible credit management and makes you an attractive candidate for loans and other financial opportunities.

In this article, we will delve into the details of a 740 credit score, exploring what it means, the factors that influence it, and the advantages that come with having such a score. We will also provide practical tips for achieving and maintaining a 740 credit score, as well as debunk common misconceptions surrounding this credit score range.

Whether you are aiming to improve your current score or simply want to understand the significance of a 740 credit score, this guide will equip you with the knowledge you need to navigate the world of credit and achieve your financial goals.

Understanding Credit Scores

Before we dive into the specifics of a 740 credit score, let’s first understand the concept of credit scores in general. A credit score is a three-digit number that reflects your creditworthiness and is typically generated by credit bureaus based on your credit history.

The most widely used credit scoring models are the FICO® Score and VantageScore. These scores range from 300 to 850, with higher scores indicating better creditworthiness. Lenders use credit scores to assess the risk of lending to a borrower and to determine the interest rates and terms of credit.

Credit scores are calculated using various factors, including:

- Payment History: This is the most influential factor, accounting for approximately 35% of your credit score. It reflects whether you have made payments on time, missed any payments, or have any delinquencies or bankruptcies.

- Credit Utilization: This factor examines how much of your available credit you are using. Ideally, you should keep your credit utilization below 30%.

- Length of Credit History: This takes into account how long you have been using credit and the average age of your credit accounts. A longer credit history generally helps boost your score.

- Credit Mix: Lenders like to see a diverse mix of credit, such as credit cards, loans, and mortgages. This shows your ability to manage different types of credit responsibly.

- New Credit Inquiries: Applying for multiple new lines of credit within a short period of time can negatively impact your credit score.

Understanding these factors is crucial for improving and maintaining a good credit score. Now, let’s focus specifically on what a 740 credit score entails.

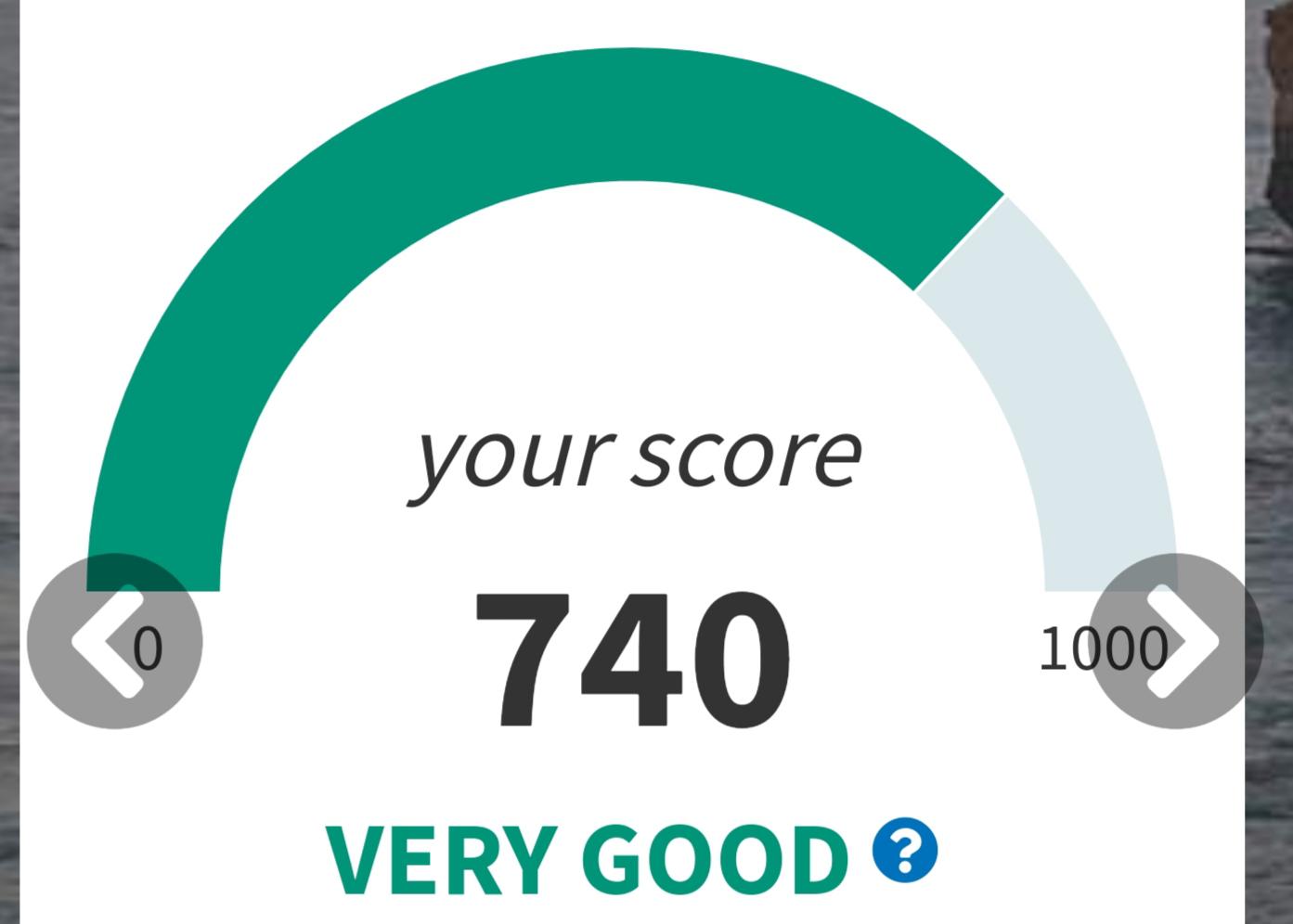

What Is a 740 Credit Score?

A 740 credit score is considered very good and puts you in a favorable position when it comes to creditworthiness. Credit scores range from 300 to 850, with higher scores indicating better creditworthiness. A score of 740 is well above the national average and demonstrates responsible credit management.

With a 740 credit score, you can expect to have access to a wide range of financial opportunities. Lenders view borrowers with a score of 740 as low-risk individuals who are likely to repay their debts on time. This means you may qualify for attractive interest rates on loans, credit cards, and mortgages.

In addition to the benefits of lower interest rates, a 740 credit score can also provide you with more negotiating power when it comes to securing loans. Lenders tend to view borrowers with higher credit scores as trustworthy and financially responsible, making them more likely to offer favorable terms and conditions.

Having a 740 credit score can also be advantageous when it comes to renting an apartment or obtaining insurance. Landlords and insurance companies often check credit scores to assess an individual’s reliability and potential risk. With a 740 credit score, you are more likely to be approved for rental applications and may even get lower insurance premiums.

It’s important to note that credit scores fluctuate over time based on factors such as payment history, credit utilization, and new credit inquiries. Therefore, it’s crucial to regularly monitor and maintain your credit score to ensure it stays in the 740 range or even improves.

Next, let’s explore the various factors that can affect a 740 credit score and how to take advantage of its benefits.

Factors That Affect a 740 Credit Score

While a 740 credit score is considered very good, it’s important to understand the factors that contribute to achieving and maintaining this level of creditworthiness. Several key factors influence your credit score and can have an impact on whether it stays at 740 or fluctuates.

1. Payment History: Your payment history has the most significant impact on your credit score. Making consistent, on-time payments is crucial for maintaining a 740 credit score. Late payments, delinquencies, and defaults can lower your score significantly.

2. Credit Utilization: Credit utilization refers to the percentage of available credit that you are currently using. Keeping your credit utilization below 30% is ideal for maintaining a good credit score. This means using no more than 30% of your available credit limit on credit cards and other lines of credit.

3. Length of Credit History: The length of your credit history plays a role in determining your credit score. A longer credit history gives lenders more information about your credit management habits and increases your creditworthiness. If you have a shorter credit history, it can be beneficial to maintain good credit practices over time to improve your score.

4. Credit Mix: Lenders like to see a diverse mix of credit types on your credit report, including credit cards, loans, and mortgages. By responsibly managing different types of credit, you can demonstrate your ability to handle financial obligations and improve your credit score.

5. New Credit Inquiries: Applying for new credit can temporarily lower your credit score. Each time you apply for credit, it triggers a hard inquiry on your credit report. Too many inquiries within a short period can be seen as a sign of financial instability. It’s important to apply for new credit only when necessary and space out your applications.

By understanding and managing these factors, you can take control of your credit score and work towards maintaining or improving a 740 credit score. In the next section, we will explore the advantages of having a 740 credit score and how it can benefit you financially.

Advantages of Having a 740 Credit Score

Holding a 740 credit score comes with a range of advantages that can positively impact your financial well-being. Lenders and financial institutions view individuals with a 740 credit score as low-risk borrowers, making you an attractive candidate for various financial opportunities.

1. Favorable Interest Rates: One of the significant advantages of a 740 credit score is the ability to secure loans and credit cards at favorable interest rates. Lenders are more likely to offer lower interest rates to borrowers with higher credit scores, potentially saving you thousands of dollars in interest over the life of a loan.

2. Access to a Wide Range of Loans: With a 740 credit score, you can qualify for a variety of loans, including mortgage loans, auto loans, and personal loans. This opens up opportunities for homeownership, purchasing a car, or financing other significant expenses.

3. Improved Chance of Approval: Having a 740 credit score increases your chances of loan and credit card approval. Lenders have confidence in your ability to manage debt responsibly, making them more willing to extend credit to you.

4. Negotiating Power: When you have a 740 credit score, you have more bargaining power when it comes to negotiating terms and conditions for loans or credit cards. Lenders are more likely to offer flexible terms, such as higher credit limits or waived fees, to individuals with strong credit profiles.

5. Easier Rental Process: A 740 credit score can make renting an apartment or house much easier. Landlords often check credit scores to assess a potential tenant’s reliability. With a 740 credit score, you are seen as financially responsible and trustworthy, increasing your chances of being approved for rental applications.

6. Lower Insurance Premiums: Insurance companies also consider credit scores when determining premiums. With a 740 credit score, you may qualify for lower insurance rates on auto, home, or other insurance policies.

Having a 740 credit score provides numerous financial advantages that can save you money and offer greater flexibility when it comes to borrowing and financial decisions. However, it’s essential to understand how to achieve and maintain this credit score, which we will explore in the following sections.

How to Achieve and Maintain a 740 Credit Score

While a 740 credit score is considered very good, it takes time and effort to achieve and maintain this level of creditworthiness. Here are some steps you can take to work towards a 740 credit score:

- Pay Your Bills on Time: Consistently make your payments by the due dates to establish a positive payment history. Late payments can have a significant impact on your credit score.

- Manage Your Credit Utilization: Aim to keep your credit utilization ratio below 30%. This means using no more than 30% of your available credit. Paying off balances in full or making more frequent payments can help keep your utilization in check.

- Maintain a Diverse Credit Portfolio: Having a mix of different types of credit accounts, such as credit cards, installment loans, and mortgages, can positively impact your credit score. However, avoid opening new accounts just for the sake of diversification.

- Keep Old Credit Accounts Open: Closing old credit accounts can shorten your credit history and lower your credit score. Even if you no longer use certain accounts, keeping them open can help maintain a longer average age of credit.

- Monitor Your Credit Report: Regularly check your credit report for any errors or discrepancies that could negatively impact your score. Report any inaccuracies to the credit bureaus to have them corrected.

- Avoid Applying for Too Much Credit: While it’s important to have a mix of credit accounts, be mindful of applying for too much credit within a short period. Each application triggers a hard inquiry, which can temporarily lower your credit score.

Consistency and responsible financial habits are key to achieving and maintaining a 740 credit score. By following these steps and practicing good credit management, you can increase your chances of reaching and surpassing the 740 credit score range.

Next, we will provide some actionable tips for improving a 740 credit score if you find yourself below this range or want to aim for an even higher score.

Tips for Improving a 740 Credit Score

If you aspire to improve your credit score from its current level or aim for an even higher score, here are some actionable tips to help you on your journey:

- Pay your bills on time: Consistently making on-time payments is crucial for improving your credit score. Set up payment reminders or automatic payments to ensure you never miss a due date.

- Reduce your credit utilization: Lowering your credit utilization ratio can have a positive impact on your credit score. Paying down outstanding balances and keeping your credit card utilization below 30% can help improve your score.

- Dispute inaccuracies: Regularly review your credit report for any errors or inaccuracies that may be affecting your score. If you find any discrepancies, file a dispute with the credit bureaus to have them corrected.

- Limit new credit applications: Each time you apply for new credit, it triggers a hard inquiry on your credit report, which can temporarily lower your score. Be selective and mindful of the number of credit applications you make within a short period.

- Build a positive credit history: If you have limited credit history, consider opening a secured credit card or becoming an authorized user on someone else’s credit card. Making responsible, on-time payments will help establish and build your credit history.

- Manage existing credit responsibly: Practice responsible credit management by avoiding maxing out credit cards and paying more than the minimum payment. Demonstrating responsible credit behavior over time can boost your credit score.

- Be patient and consistent: Remember that improving your credit score takes time and requires consistent effort. Focus on building positive credit habits, and your score will gradually improve over time.

By implementing these strategies, you can work towards improving your credit score and moving closer to the coveted 740 credit score range. Remember that every positive financial decision and responsible credit management can contribute to a better credit score.

Now that we have explored how to improve a credit score, let’s address some common misconceptions surrounding 740 credit scores in the next section.

Common Misconceptions About 740 Credit Scores

While a 740 credit score is considered very good, there are several misconceptions surrounding this credit score range that are important to address. Understanding these misconceptions can help you make better financial decisions and avoid unnecessary confusion. Let’s debunk some common misconceptions:

- A 740 credit score is perfect: While a 740 credit score is excellent, it does not mean your credit is flawless or without room for improvement. There is always room for growth and further enhancing your credit profile.

- A 740 credit score guarantees loan approval: While a 740 credit score increases your chances of approval, lending decisions also consider other factors such as income, employment history, and debt-to-income ratio. A credit score is just one piece of the overall assessment lenders make.

- A 740 credit score will never change: Credit scores are not static and can fluctuate based on various factors such as payment history, credit utilization, and new credit inquiries. It’s important to consistently practice good credit habits to maintain a 740 credit score or improve it even further.

- Closing credit accounts improves a 740 credit score: Closing old credit accounts can actually hurt your credit score. It shortens your credit history and reduces the overall amount of credit available to you, which can increase your credit utilization ratio.

- Having a 740 credit score means you’ve reached the highest level: While a 740 credit score is excellent, there are higher credit score ranges. Strive to continue practicing responsible credit management and aim for an even higher score to unlock further financial opportunities.

Understanding these misconceptions allows you to have a more realistic view of a 740 credit score and how it fits into the larger picture of your overall financial health. It’s important to stay informed and continue working towards financial goals regardless of your current credit score range.

As we conclude, let’s summarize the key points and reflect on the significance of a 740 credit score.

Conclusion

A 740 credit score is considered very good and opens up a range of financial opportunities. It signifies responsible credit management and makes you an attractive candidate for loans, credit cards, and other financial products. By understanding the factors that affect your credit score, such as payment history, credit utilization, and credit mix, you can work towards achieving and maintaining a 740 credit score.

Having a 740 credit score comes with significant advantages, including access to lower interest rates, a wider range of loan options, and improved negotiating power. It can also make the rental process easier and potentially lead to lower insurance premiums. However, it’s important to debunk common misconceptions, such as a 740 credit score being perfect or guaranteeing loan approval. Credit scores can fluctuate, and there is always room for improvement.

To achieve and maintain a 740 credit score, it’s important to pay your bills on time, manage your credit utilization, maintain a diverse credit mix, and monitor your credit report for errors. By practicing responsible credit habits and being patient and consistent, you can work towards improving your credit score over time.

Remember, a 740 credit score is just one aspect of your overall financial health. It’s essential to also focus on other aspects such as saving, budgeting, and investing to build a strong financial foundation. By adopting a holistic approach to personal finance, you can set yourself up for long-term success and achieve your financial goals.

Continue to educate yourself on credit scores, financial management, and the factors that impact your creditworthiness. With the right knowledge and habits, you can use your credit score as a tool to unlock financial opportunities and improve your overall financial well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance