Finance

What Is Collateral Protection Insurance?

Modified: February 21, 2024

Learn about collateral protection insurance, a crucial aspect of finance. Understand how it safeguards lenders against borrower defaults while securing loans.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- What is Collateral Protection Insurance?

- How Does Collateral Protection Insurance Work?

- Benefits of Collateral Protection Insurance

- Drawbacks of Collateral Protection Insurance

- Types of Collateral Covered by Collateral Protection Insurance

- How to Obtain Collateral Protection Insurance

- Factors to Consider When Choosing Collateral Protection Insurance

- Alternatives to Collateral Protection Insurance

- Conclusion

Introduction

When it comes to financing, lenders often require some form of security to protect themselves in case of borrower default. This security is known as collateral. Collateral can come in various forms, such as real estate, vehicles, or other valuable assets. However, lenders understand that accidents and unexpected events can happen, potentially causing the loss of the collateral.

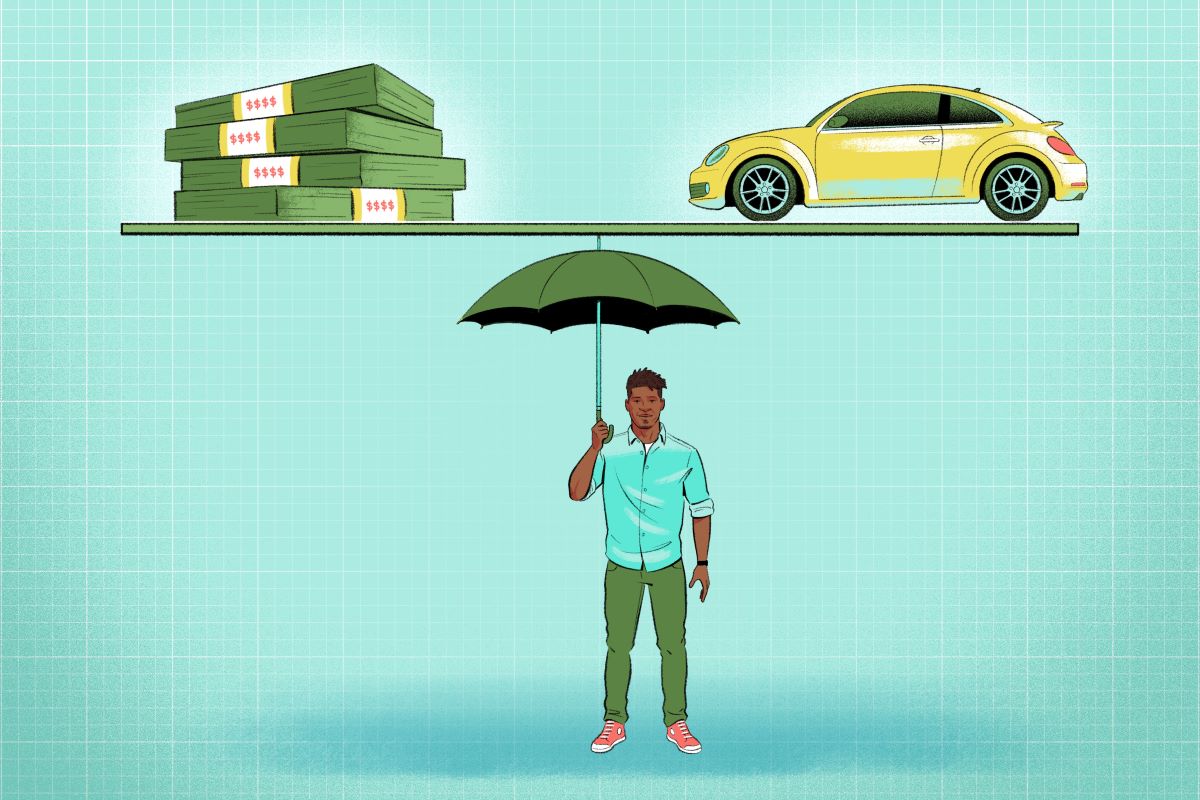

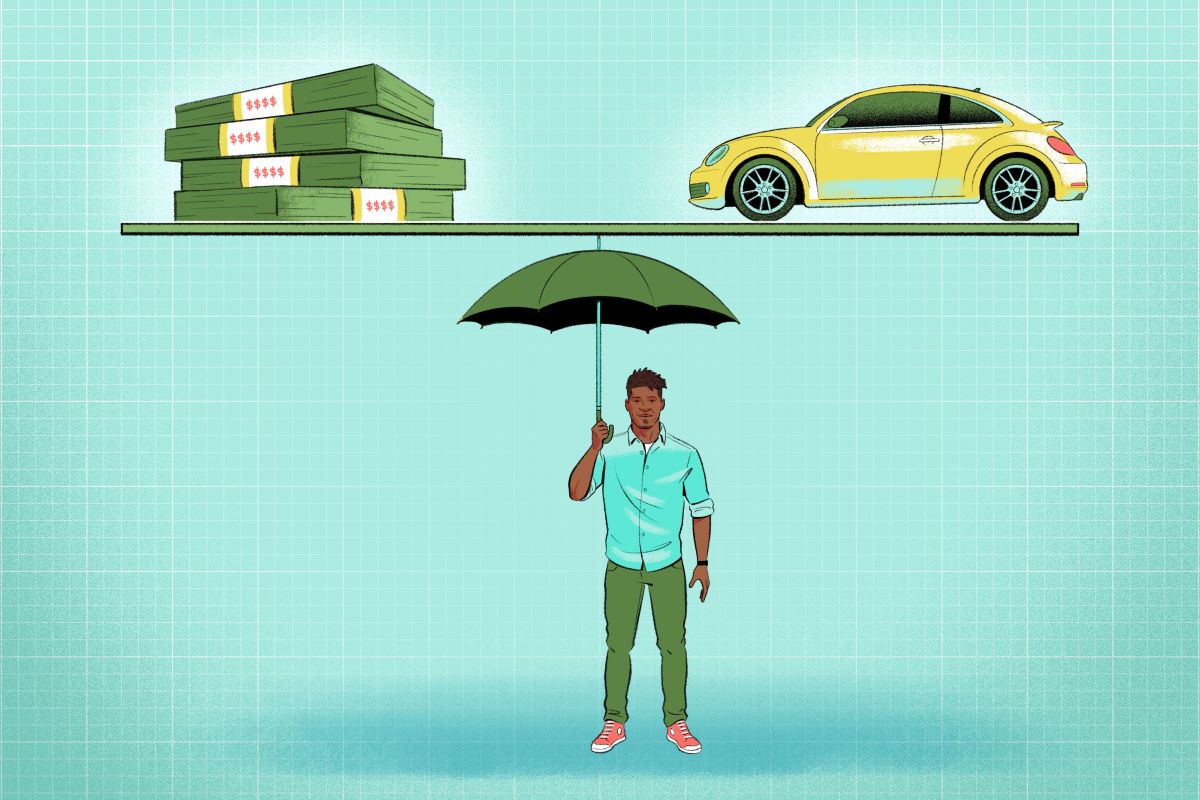

That’s where collateral protection insurance (CPI) comes into play. Collateral protection insurance is a type of insurance policy that protects lenders against the risk of losing their collateral due to a borrower’s failure to maintain adequate insurance coverage. In the event of a covered loss, the insurance policy pays the lender the value of the collateral, helping to mitigate the financial impact of the loss.

Collateral protection insurance is commonly used in lending arrangements where the borrower is required to maintain insurance coverage on the collateral. Although borrowers are responsible for maintaining their own insurance, lenders often require collateral protection insurance as an additional safeguard to protect their interests. This type of insurance provides peace of mind for both lenders and borrowers, ensuring that the value of the collateral is protected in the event of an unforeseen circumstance.

In this article, we will delve deeper into what collateral protection insurance is, how it works, and the benefits and drawbacks associated with it. We will also discuss the types of collateral typically covered by collateral protection insurance, how to obtain it, and alternatives to consider. By understanding the intricacies of collateral protection insurance, you can make informed decisions regarding your borrowing and insurance needs.

What is Collateral Protection Insurance?

Collateral protection insurance (CPI) is a type of insurance coverage that provides financial protection to lenders in the event of borrower default or loss of collateral. It is designed to ensure that the lender’s interest in the collateral is adequately safeguarded. The insurance policy is typically initiated by the lender and is often attached to the loan or financing agreement.

When a borrower takes out a loan to purchase a valuable asset, such as a car or a piece of property, the lender may require the borrower to maintain insurance coverage on that asset. This is to protect the lender’s financial interest in the collateral in case of any damage, loss, or theft. However, borrowers may sometimes fail to maintain sufficient insurance coverage, leaving the lender exposed to potential financial loss.

This is where collateral protection insurance steps in. If the borrower fails to maintain the required insurance coverage on the collateral, the lender can activate the collateral protection insurance policy. In the event of a covered loss, such as an accident, natural disaster, or theft, the insurance policy reimburses the lender for the value of the collateral, helping to recoup any outstanding loan balance.

Collateral protection insurance is different from traditional insurance policies as it is not designed to protect the borrower’s interests. Instead, it solely focuses on protecting the lender by ensuring the value of the collateral is maintained throughout the loan term, even if the borrower fails to fulfill their insurance obligations.

It is important to note that collateral protection insurance is typically more expensive than standard insurance policies. This is due to factors such as the higher risk associated with insuring the lender’s interests, the coverage provided, and the administrative costs involved in managing the insurance program.

In the next section, we will explore how collateral protection insurance works and the key factors to consider when evaluating this type of insurance coverage.

How Does Collateral Protection Insurance Work?

Collateral protection insurance (CPI) works as an additional layer of insurance coverage that protects the lender’s interests in the collateral. Here is a step-by-step breakdown of how CPI works:

- Lender Implements CPI Requirement: When a borrower takes out a loan that requires collateral, the lender may include a clause in the loan agreement that mandates the borrower to maintain insurance coverage on the collateral throughout the loan term.

- Borrower’s Insurance Verification: The borrower is responsible for providing proof of insurance to the lender, typically in the form of an insurance policy declaration page. This document outlines the details of the insurance coverage, including the insured parties, policy limits, and effective dates.

- Borrower Fails to Maintain Insurance: If the borrower fails to maintain the required insurance coverage on the collateral, such as by allowing the policy to lapse or not renewing it, the lender becomes exposed to potential financial risk. At this point, the lender may activate the collateral protection insurance policy.

- Lender Enforces Collateral Protection Insurance: Once the lender activates the CPI, the borrower is typically notified and provided with an opportunity to rectify the insurance coverage issue. If the borrower fails to comply, the lender enforces the CPI and adds the cost of the insurance premium to the borrower’s loan balance, which may result in an increase in monthly payments.

- Claim Processing: In the event of a covered loss that affects the collateral, such as an accident, theft, or natural disaster, the lender submits a claim to the CPI provider. The provider evaluates the claim and, if approved, reimburses the lender for the value of the collateral up to the policy limits.

- Loan Balance Adjustment: Once the lender receives the insurance reimbursement, it can apply the funds to the borrower’s outstanding loan balance, reducing the amount owed. This helps protect the lender from incurring a financial loss due to the borrower’s failure to maintain insurance coverage.

- Borrower’s Responsibility: It is important for borrowers to understand that even though collateral protection insurance provides coverage for the lender, it does not absolve them of their responsibility to maintain insurance coverage on the collateral. Borrowers are still required to maintain their own insurance policies to protect their own interests and comply with legal requirements.

Overall, collateral protection insurance is a mechanism that offers an extra layer of protection for lenders by ensuring that the value of the collateral is safeguarded, even if the borrower fails to meet their insurance obligations. It helps mitigate the financial risks associated with borrower default or loss of the collateral and provides lenders with added peace of mind.

Benefits of Collateral Protection Insurance

Collateral protection insurance (CPI) provides several benefits for both lenders and borrowers involved in lending arrangements that require collateral. Here are some of the key benefits of collateral protection insurance:

- Protection for Lenders: The primary benefit of CPI is that it offers protection to lenders by ensuring that their financial interests in the collateral are safeguarded. In the event of borrower default or loss of the collateral, the insurance policy helps recoup the value of the collateral, reducing the lender’s potential financial loss.

- Streamlined Coverage: Collateral protection insurance is typically initiated by the lender and integrated into the loan agreement. This means that the coverage is established upfront, eliminating the need for individual borrowers to find and maintain separate insurance policies for the collateral. This streamlines the insurance process and ensures continuous coverage.

- Added Convenience for Borrowers: Borrowers benefit from collateral protection insurance by having the convenience of not having to search for or manage separate insurance policies for the collateral. Instead, the insurance coverage is seamlessly integrated into their loan, simplifying the insurance process and reducing administrative burdens.

- Peace of Mind: For both lenders and borrowers, collateral protection insurance provides peace of mind. Lenders can be confident that their interests are protected, while borrowers can have assurance that the collateral is safeguarded, even if unforeseen circumstances occur.

- Reduced Risk Exposure: By activating collateral protection insurance in cases where borrowers fail to maintain adequate insurance coverage, lenders minimize their exposure to financial risk. This added layer of protection helps protect their investment and ensures they can recover the value of the collateral if necessary.

- Avoidance of Costly Litigation: In situations where borrowers do not have insurance or have insufficient coverage, lenders could potentially take legal action to recover losses. Collateral protection insurance helps mitigate the need for costly legal proceedings by providing an alternative method to compensate lenders.

- Flexibility in Coverage: Collateral protection insurance can be tailored to meet the specific needs of lenders and borrowers. The coverage limits, terms, and conditions can be customized based on the type of collateral, loan amount, and other relevant factors, ensuring that the policy aligns with the specific requirements of the lending arrangement.

Overall, collateral protection insurance offers significant benefits to lenders and borrowers involved in loans secured by collateral. It provides a safety net in case of borrower default or loss of the collateral and offers peace of mind, convenience, and reduced financial risk exposure for all parties involved.

Drawbacks of Collateral Protection Insurance

While collateral protection insurance (CPI) offers benefits to lenders and borrowers, there are also some drawbacks to consider. It is essential to weigh these potential disadvantages before deciding to utilize collateral protection insurance. Here are some of the key drawbacks:

- Higher Cost: One of the significant drawbacks of CPI is that it tends to be more expensive compared to standard insurance policies. This is due to factors such as the higher risk associated with insuring the lender’s interests, the coverage provided, and the administrative costs involved in managing the insurance program. The additional cost can increase the overall borrowing expenses for the borrower.

- Double Coverage: Collateral protection insurance is typically required in addition to the borrower’s individual insurance coverage. This means that borrowers may end up paying for two insurance policies to protect against the same risks. It can result in unnecessary expenses and potential duplication of coverage.

- Limited Coverage: The coverage provided by collateral protection insurance is often limited to the value of the collateral and does not extend to other aspects such as liability coverage or personal property coverage. Borrowers may need to seek additional insurance coverage to adequately protect themselves and their assets as necessary.

- Reduced Control: When borrowers are required to obtain collateral protection insurance, they may have limited control over choosing the insurance provider or policy terms. The lender may have existing agreements with specific insurance providers and dictate the terms of the coverage, which may not align with the borrower’s preferences or needs.

- Addition to Loan Balance: If the lender activates the collateral protection insurance due to the borrower’s failure to maintain adequate insurance coverage, the cost of the insurance premium is typically added to the borrower’s loan balance. This can lead to an increase in monthly payments and the overall cost of the loan.

- No Benefit for Borrowers: While CPI provides an added layer of protection for lenders, it does not directly benefit the borrower. The insurance coverage focuses solely on protecting the lender’s interests, and the borrower still needs to maintain their own insurance policies to protect their assets and comply with legal requirements.

- Potential for Coverage Gaps: There is a risk of coverage gaps when borrowers rely solely on collateral protection insurance. The coverage may only kick in if the borrower fails to maintain insurance, leaving periods of potential vulnerability where the collateral is not adequately insured.

It is essential for borrowers and lenders to carefully evaluate the drawbacks associated with collateral protection insurance and weigh them against the benefits. Considering the specific financial situation, needs, and risk tolerance is crucial in determining whether CPI is a suitable option or if alternative solutions should be explored.

Types of Collateral Covered by Collateral Protection Insurance

Collateral protection insurance (CPI) can cover various types of collateral, depending on the lending arrangement and the insurance policy in place. Here are some common types of collateral that can be covered by collateral protection insurance:

- Automobiles: Vehicles, such as cars, trucks, motorcycles, and recreational vehicles, are often financed with loans that require collateral protection insurance. CPI can provide coverage for these assets in case of accidents, theft, or other covered losses.

- Real Estate: Real estate properties, including homes, condos, and commercial buildings, can also be protected by collateral protection insurance. This coverage may vary depending on the type of property and the specific terms of the insurance policy.

- Boats and Watercraft: Collateral protection insurance can extend to boats and other watercraft, ensuring that the lender is protected in the event of damage, loss, or theft related to these assets.

- Recreational Vehicles: Campers, motorhomes, and other recreational vehicles can be covered under CPI. This provides lenders with reassurance that their financial interest in these assets is protected.

- Equipment and Machinery: In commercial lending arrangements, collateral protection insurance can safeguard equipment and machinery used for business purposes. This coverage helps mitigate risks associated with damage or loss of these valuable assets.

- Fine Art and Collectibles: For loans secured by high-value artwork or collectibles, collateral protection insurance can provide coverage in case of damage or loss. This specialized coverage ensures that the lender’s investment in these assets is adequately protected.

- Other Valuable Assets: CPI can also cover other types of valuable assets, including jewelry, precious metals, stocks, bonds, and more. The specific coverage will depend on the terms of the insurance policy and the lender’s requirements.

It’s important to note that the availability and extent of collateral protection insurance for each type of asset may vary among lenders and insurance providers. Additionally, the coverage limits, deductibles, and terms and conditions will be outlined in the insurance policy and should be carefully reviewed by borrowers and lenders alike.

When applying for a loan that requires collateral protection insurance, borrowers should inquire about the specifics of the coverage and ensure that their chosen assets are eligible for protection under the policy. Lenders, on the other hand, should clearly communicate the requirements and expectations regarding collateral protection insurance to borrowers.

How to Obtain Collateral Protection Insurance

Obtaining collateral protection insurance (CPI) typically involves a collaborative effort between the lender, the borrower, and an insurance provider. Here are the general steps involved in obtaining CPI:

- Lender’s Requirements: The lender will specify the requirement for collateral protection insurance in the loan agreement. This includes details on the type of collateral that needs to be insured and the minimum coverage limits.

- Insurance Research: The borrower should research and identify insurance providers that offer collateral protection insurance. It may be beneficial to work with an insurance agent or broker who specializes in this type of insurance to navigate the process more efficiently.

- Insurance Quotes: The borrower can reach out to multiple insurance providers to request quotes for collateral protection insurance. It is important to provide accurate information about the collateral and the loan details to obtain accurate quotes.

- Compare Coverage and Costs: The borrower should compare the coverage options, policy terms, deductibles, and costs provided by different insurance providers. It is crucial to fully understand the extent of coverage and any limitations or exclusions.

- Select an Insurance Provider: Based on the research and comparison, the borrower can choose a suitable insurance provider that offers comprehensive coverage at a competitive price. The lender may have specific requirements or preferred providers that borrowers need to consider.

- Application Process: The borrower will need to complete an application form provided by the chosen insurance provider. The application requires information about the collateral, loan details, and any specific requirements from the lender.

- Underwriting and Approval: The insurance provider will review the application and underwrite the policy. This involves assessing the risk associated with insuring the collateral and evaluating the borrower’s insurance history and creditworthiness. Once approved, the insurance provider will issue the collateral protection insurance policy.

- Policy Activation: The borrower is responsible for providing proof of insurance to the lender to satisfy the requirements outlined in the loan agreement. This includes providing the policy documentation and any other required information.

- Ongoing Premium Payments: The borrower is required to make premium payments to the insurance provider to keep the collateral protection insurance policy active. Failure to maintain timely premium payments can result in policy cancellation or activation of the lender’s collateral protection insurance.

It is important for borrowers to thoroughly read and understand the terms and conditions of the collateral protection insurance policy before signing and committing to it. They should also communicate with the lender to ensure compliance with all requirements.

Working with an insurance professional who specializes in CPI can be beneficial in navigating the process and securing the most suitable coverage for the specific lending arrangement. Open communication between the lender, borrower, and insurance provider is crucial to ensure a smooth and effective process of obtaining collateral protection insurance.

Factors to Consider When Choosing Collateral Protection Insurance

When selecting collateral protection insurance (CPI), it is important to consider various factors to ensure that the coverage meets your specific needs and provides adequate protection. Here are some key factors to consider when choosing collateral protection insurance:

- Coverage Limits: Review the coverage limits provided by the insurance policy and ensure they align with the value of the collateral. It is essential to have sufficient coverage to protect the lender’s interests in the event of a loss.

- Deductibles: Take note of the deductibles associated with the collateral protection insurance policy. A higher deductible could mean lower premium costs but may require the borrower to pay a larger amount out-of-pocket in the event of a claim.

- Policy Terms: Read and understand the terms and conditions of the collateral protection insurance policy. Pay attention to any exclusions, limitations, or special requirements outlined in the policy to ensure they align with your specific lending arrangement.

- Insurance Provider: Research and evaluate the reputation, financial stability, and customer service of the insurance provider. Choose a provider with a strong track record in handling collateral protection insurance claims promptly and effectively.

- Premium Costs: Compare the premium costs offered by different insurance providers. While it is important to consider cost, remember that cheaper premiums may result in lower coverage limits or less favorable policy terms. Strike a balance between affordability and comprehensive coverage.

- Claims Process: Understand the process for filing a claim with the insurance provider. Determine how responsive and efficient the provider is in handling claims and how quickly they can provide reimbursement to the lender in the event of a covered loss.

- Additional Coverage Options: Consider whether the collateral protection insurance policy offers any additional coverage options, such as liability coverage or coverage for personal property within the collateral. Depending on your specific needs, these additional coverage options may be beneficial.

- Compliance with Lender’s Requirements: Ensure that the collateral protection insurance policy meets the requirements stipulated by the lender in the loan agreement. This includes verifying that the insurance provider is acceptable to the lender and that the coverage complies with the specified terms and conditions.

- Flexibility of Coverage: Assess whether the collateral protection insurance policy can be customized to meet specific needs. This may include adjusting coverage limits, deductibles, or adding riders to cover additional risks or types of collateral.

- Customer Reviews and Recommendations: Consider reading customer reviews and seeking recommendations from other borrowers or industry professionals who have experience with collateral protection insurance. Their insights can provide valuable information and help you make an informed decision.

By carefully considering these factors, you can choose the right collateral protection insurance that provides comprehensive coverage, aligns with your specific lending arrangement, and offers peace of mind to both you and your lender.

Alternatives to Collateral Protection Insurance

While collateral protection insurance (CPI) can provide an added layer of protection for lenders, there may be alternative options that borrowers can consider. Here are some alternatives to collateral protection insurance:

- Borrower’s Own Insurance: Instead of relying solely on collateral protection insurance, borrowers can maintain their own insurance coverage on the collateral. This involves obtaining a standard insurance policy that meets the requirements specified by the lender. By maintaining their own insurance, borrowers have more control over the coverage, deductibles, and policy terms.

- Loan Repayment: Another alternative is to focus on timely loan repayment to reduce the risk of default. By fulfilling the loan obligations, borrowers can mitigate the need for collateral protection insurance altogether. Repayment strategies such as increasing monthly installments or making extra principal payments can help pay down the loan faster and reduce the exposure to potential losses.

- Self-Insurance: In some cases, borrowers may choose to self-insure by setting aside funds in a reserve account to cover potential losses. This can be an option for individuals or businesses with strong financial stability and liquidity. Self-insurance requires careful financial planning and risk assessment.

- Credit Insurance: Credit insurance is an alternative form of coverage that protects lenders against borrower default. This insurance specifically covers the loan payments if the borrower becomes unable to make them due to unforeseen circumstances such as disability, unemployment, or death. Credit insurance is typically offered by insurance providers or financial institutions.

- Guarantors or Co-Signers: Borrowers may consider involving a guarantor or co-signer who agrees to be responsible for loan repayment in case of default. This provides an additional layer of security for the lender, as the guarantor’s assets can be used to cover the loan if the borrower fails to repay.

- Structured Repayment Plans: Instead of relying on insurance or collateral, borrowers can negotiate structured repayment plans with the lender. These plans may include adjustable payment schedules or loan modifications that can help reduce the risk of default, making collateral protection insurance unnecessary.

- Higher Down Payments or Additional Collateral: Lenders may be willing to reduce the need for collateral protection insurance if borrowers provide a higher down payment or additional collateral to secure the loan. This reduces the lender’s risk exposure and may lessen the requirement for insurance coverage.

It is important to evaluate the specific needs, financial stability, and risk tolerance of each borrower before considering alternatives to collateral protection insurance. Discussing the alternatives with the lender and seeking advice from insurance professionals or financial advisors can help determine the most suitable option for each individual borrower’s circumstances.

Conclusion

Collateral protection insurance (CPI) is an insurance policy that provides an additional layer of protection for lenders in case of borrower default or loss of collateral. It ensures that the lender’s financial interests in the collateral are safeguarded, offering peace of mind and reducing the risk of financial loss. While CPI offers benefits such as streamlined coverage and convenience for borrowers, it also has drawbacks like higher costs and potential coverage gaps.

When considering collateral protection insurance, it is important to carefully evaluate factors such as coverage limits, deductibles, policy terms, and costs. Additionally, alternative options, such as maintaining the borrower’s own insurance coverage, loan repayment strategies, or exploring credit insurance, should be considered. Each borrower’s specific needs, financial situation, and risk tolerance are crucial factors in determining the best approach.

Lastly, open communication between lenders, borrowers, and insurance providers is vital in facilitating the process of obtaining collateral protection insurance. Understanding the lender’s requirements, researching reputable insurance providers, and diligently reviewing policy details are essential steps to ensure comprehensive coverage.

In conclusion, collateral protection insurance serves as a resource for lenders and borrowers involved in lending arrangements that require collateral. By understanding the purpose, benefits, drawbacks, and alternatives of CPI, borrowers can make informed decisions to protect their financial interests and meet the requirements set forth by lenders. With the right insurance coverage or alternative risk management strategies in place, both lenders and borrowers can navigate lending arrangements with confidence and security.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance