Finance

What Does Collateral Insurance Cover?

Published: November 12, 2023

Learn what collateral insurance covers in the world of finance and ensure your assets are protected.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

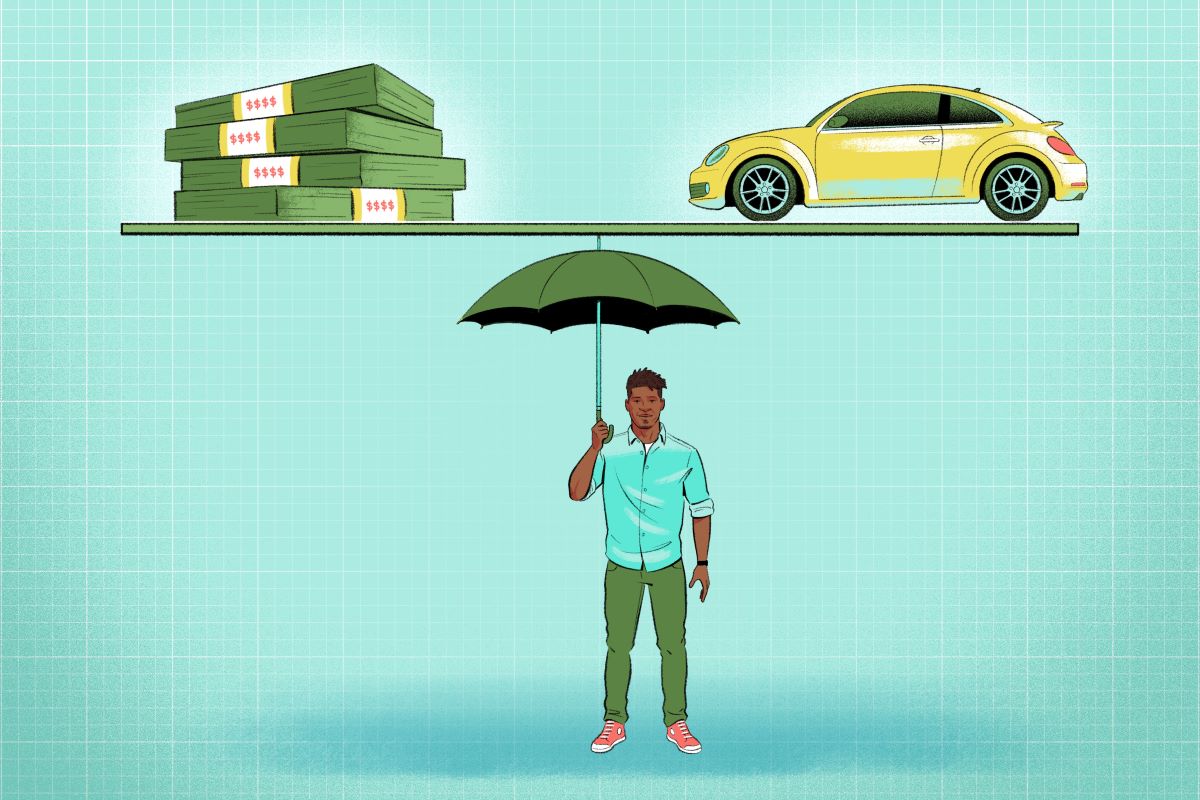

Collateral insurance is a crucial component of financial risk management. It provides protection for lenders and borrowers by offering coverage for assets or property used as collateral for a loan. This type of insurance ensures that in the event of a loss, the lender’s interest is protected and the borrower’s financial liability is limited.

When individuals or businesses obtain a loan, they may be required to pledge collateral as security for the loan. This collateral can range from real estate properties and vehicles to equipment or other valuable assets. Collateral insurance acts as a safeguard, offering financial compensation in case of damage, destruction, or loss to the pledged collateral.

It is important to understand that collateral insurance is different from traditional property or asset insurance. While property or asset insurance generally provides coverage for the owner’s interest, collateral insurance focuses on protecting the lender’s investment.

The purpose of this article is to shed light on the various types of collateral insurance, the coverage it provides, and its importance in risk management.

In the sections that follow, we will delve deeper into the different types of collateral insurance and the specific types of coverage they offer, including coverage for property and assets, coverage for loans, coverage for liabilities, and additional coverage options. We will also discuss the exclusions and limitations of collateral insurance and highlight its significance in mitigating financial risks for both lenders and borrowers.

So, let’s explore the world of collateral insurance and gain a comprehensive understanding of its benefits and implications.

Definition of Collateral Insurance

Collateral insurance refers to a type of insurance coverage that protects the interests of lenders and borrowers when collateral is utilized to secure a loan or financial transaction. Collateral refers to assets or property that is pledged as security or guarantee for a loan, providing the lender with a means to recover their investment in the event of default or non-payment.

Collateral insurance is designed to mitigate the risk associated with lending money by ensuring that the value of the collateral is protected. In the event of damage, loss, or destruction of the collateral, the insurance policy kicks in to provide financial compensation to the lender, limiting their potential losses and helping to maintain the borrower’s obligations.

One of the key distinctions between collateral insurance and traditional property or asset insurance is the focus on protecting the interests of the lender rather than the owner. While property or asset insurance commonly covers the owner’s interest, collateral insurance specifically safeguards the lender’s investment.

Collateral insurance provides lenders with a sense of security by reducing their exposure to risk. It assures them that their financial interest will be protected, even if the borrower defaults on the loan. This protection enables lenders to offer loans at favorable terms and interest rates, as they have additional security in the form of collateral insurance.

For borrowers, collateral insurance provides an opportunity to secure loans more easily and at more competitive rates. By pledging collateral and obtaining collateral insurance, borrowers not only enhance their chances of loan approval but also benefit from reduced interest rates due to the decreased risk perceived by the lender.

Overall, collateral insurance serves as a vital risk management tool in the world of lending and finance. It ensures that both lenders and borrowers have a safety net in place, protecting their respective interests and promoting financial stability.

Types of Collateral Insurance

Collateral insurance comes in various forms to cater to the different types of collateral utilized in financial transactions. Here are some common types of collateral insurance:

- Property Collateral Insurance: This type of collateral insurance offers coverage for real estate properties that are pledged as collateral. It protects the lender’s interest in case of damage or destruction to the property, such as due to fire, natural disasters, or vandalism.

- Asset Collateral Insurance: Asset collateral insurance provides coverage for valuable assets that are pledged as collateral, including vehicles, equipment, or inventory. It safeguards the lender’s investment in case of theft, damage, or loss of these assets.

- Loan Collateral Insurance: Loan collateral insurance focuses on providing coverage for the outstanding loan amount in case of default or non-payment by the borrower. It ensures that the lender is compensated for any losses incurred due to the borrower’s inability to repay the loan.

- Liability Collateral Insurance: Liability collateral insurance offers protection to lenders when the collateral involves a liability, such as personal guarantees or surety bonds. It compensates the lender for any losses arising from default on these obligations.

- Additional Coverage Options: Some collateral insurance policies also offer additional coverage options. This may include coverage for legal expenses related to enforcing the rights of the lender, coverage for loss of income if the collateral is income-generating, or coverage for the costs of appraisals or inspections.

The specific type of collateral insurance required will depend on the nature of the collateral being used in the financial transaction. Lenders will assess the risk associated with the collateral and determine the appropriate type and level of coverage needed to protect their investment.

It is worth noting that the availability of these different types of collateral insurance may vary depending on the insurance providers and the jurisdiction in which the transaction takes place. It is important for borrowers and lenders to carefully review and understand the terms and conditions of the collateral insurance policy to ensure it meets their specific needs and offers adequate protection.

In the next sections, we will explore the coverage provided by collateral insurance policies for different types of collateral in more detail.

Coverage for Property

Collateral insurance provides coverage for various types of property that is pledged as collateral for a loan or financial transaction. Here is a closer look at the coverage offered for different types of property:

- Real Estate Property: Collateral insurance for real estate property offers protection in case of damage, destruction, or loss. It typically covers events such as fire, natural disasters, theft, vandalism, and other hazards. In the event of a covered loss, the insurance policy compensates the lender for the value of the damaged or destroyed property, reducing their financial risk.

- Vehicles: Collateral insurance for vehicles protects the lender’s interest in the event of theft, accidents, or damage to the pledged vehicle. It covers repair or replacement costs and helps mitigate potential losses for the lender.

- Equipment: When equipment is pledged as collateral, collateral insurance provides coverage in case of damage, breakdown, or loss. It ensures that the lender is protected financially and can recover the value of the equipment in case of any unforeseen incidents.

- Inventory: For businesses that use inventory as collateral, collateral insurance covers loss due to theft, damage, or destruction of the inventory. This coverage aids in reducing the lender’s exposure to risk and safeguards their investment in case of stock-related losses.

The coverage provided by collateral insurance policies for property collateral may vary based on the specific terms and conditions set forth by the insurer. It is important for both borrowers and lenders to carefully review the policy and ensure that it adequately covers the value of the property being used as collateral.

Additionally, borrowers should ensure that they maintain the required level of property insurance to protect their interests as well. This may involve obtaining property insurance that covers their own ownership interest beyond what is covered by the collateral insurance policy.

By offering coverage for property collateral, collateral insurance helps to mitigate the risk associated with loans and financial transactions. It safeguards the lender’s investment, promotes financial stability, and provides borrowers with the opportunity to secure loans at favorable terms.

Coverage for Assets

Collateral insurance also provides coverage for various types of assets that are pledged as collateral for loans or financial transactions. Here is an overview of the coverage offered for different asset types:

- Vehicles: Collateral insurance for vehicles offers protection in the event of theft, accidents, or damage to the pledged vehicle. It covers repair or replacement costs, ensuring that the lender’s investment is protected in case of unforeseen incidents.

- Equipment: When equipment is used as collateral, collateral insurance provides coverage for damage, breakdowns, or loss. It helps mitigate the financial risk for the lender, compensating them for the value of the equipment in case of any unforeseen events.

- Inventory: Businesses that use inventory as collateral can benefit from collateral insurance coverage for loss due to theft, damage, or destruction of the inventory. This coverage reduces the lender’s exposure to risk and ensures that they can recover the value of the inventory in case of stock-related losses.

- Securities: In some cases, securities such as stocks, bonds, or other investments can be pledged as collateral. Collateral insurance for securities may offer protection against fluctuations in market value or loss of value, safeguarding the lender’s investment.

- Accounts Receivable: Collateral insurance that covers accounts receivable provides protection to lenders against non-payment or default by the borrower’s customers. It compensates the lender for the outstanding amount owed by the borrower’s customers, reducing the financial impact on the lender.

The coverage provided for asset collateral through collateral insurance policies may differ depending on the specific terms and conditions outlined by the insurer. It is essential for both borrowers and lenders to carefully review the policy and ensure that the coverage aligns with the value of the assets being used as collateral.

While collateral insurance protects the lender’s interest in the assets, borrowers should maintain appropriate levels of insurance to safeguard their own ownership interest in the assets. This may include obtaining separate insurance coverage beyond what is provided by the collateral insurance policy.

By providing coverage for assets used as collateral, collateral insurance helps to mitigate the risk associated with loans and financial transactions. It ensures that both lenders and borrowers have a safety net in place, protecting their respective interests and promoting financial stability.

Coverage for Loans

Collateral insurance plays a crucial role in providing coverage for loans, offering protection to lenders in the event of default or non-payment by borrowers. Here’s a closer look at the coverage provided for loans through collateral insurance:

Loan collateral insurance focuses on protecting the outstanding loan amount when borrowers are unable to make payments. In the event of default, the insurance policy compensates the lender for any losses incurred due to the borrower’s failure to repay the loan.

The coverage provided by collateral insurance for loans typically includes the following:

- Default: When a borrower defaults on a loan, collateral insurance covers the outstanding loan balance. This ensures that the lender does not bear the full burden of the borrower’s default and minimizes their financial risk.

- Non-Payment: If a borrower fails to make the required loan payments, collateral insurance assists the lender by compensating them for the unpaid amounts. This coverage helps protect the lender’s financial interests and provides a safety net in case of delinquency.

- Repurchase: In certain loan agreements, collateral insurance may provide coverage in the event that the lender is forced to repurchase the loan from another entity due to the borrower’s default. This coverage helps the lender recoup their investment and limit potential losses.

- Legal Costs: Some collateral insurance policies may also cover legal expenses incurred by the lender in pursuing legal action against the borrower for defaulting on the loan. This coverage assists lenders in recovering their losses and enforcing their rights.

- Disputed Claims: If there is a dispute between the lender and borrower regarding the loan repayment, collateral insurance may cover the costs associated with resolving the dispute, including arbitration or mediation fees.

It is important for lenders to carefully review the terms and conditions of the collateral insurance coverage for loans to understand the extent of protection provided. Borrowers should also be aware that their obligations in the loan agreement extend to maintaining the collateral insurance policy on the pledged assets or property.

By offering comprehensive coverage for loans, collateral insurance mitigates the risks for lenders and provides them with an added layer of protection. It enables lenders to extend credit with confidence, knowing that their interests are safeguarded even in challenging situations.

Coverage for Liabilities

Collateral insurance also extends coverage to situations where liabilities are pledged as collateral for loans or financial transactions. This type of coverage protects lenders against default or non-payment of these liability-based obligations. Here’s a closer look at the coverage provided for liabilities through collateral insurance:

- Personal Guarantees: When personal guarantees are used as collateral, collateral insurance offers protection to the lender in case the guarantor fails to fulfill their obligations. It compensates the lender for any losses incurred due to the default of the personal guarantor.

- Surety Bonds: Collateral insurance for surety bonds covers situations where a surety bond is used as collateral for a loan or financial transaction. It compensates the lender in case of default by the bond issuer, ensuring that the lender’s investment is protected.

- Indemnities: In situations where indemnities are pledged as collateral, collateral insurance provides coverage in case the indemnifier fails to fulfill their obligations. It offers financial compensation to the lender for any losses incurred due to the indemnifier’s default.

- Other Liability Collateral: Collateral insurance can also extend coverage to other types of liability collateral, such as performance bonds or letters of credit. It ensures that lenders are protected in case of default or non-payment by the borrower or issuer of these liability-based instruments.

The specific terms and conditions of the collateral insurance coverage for liabilities may vary depending on the insurer and the nature of the liability being used as collateral. It is crucial for both borrowers and lenders to carefully review the policy to ensure that it adequately covers the value of the liability and offers the desired level of protection.

Collateral insurance for liabilities gives lenders peace of mind, knowing that they are protected in case of default or non-payment by the borrower or guarantor. By offering coverage for liabilities used as collateral, this type of insurance minimizes the financial risks associated with such transactions and promotes a more secure lending environment.

Additional Coverage Options

In addition to the standard coverage provided for collateral assets and liabilities, collateral insurance may also offer various additional coverage options. These options can enhance the level of protection for lenders and borrowers involved in loan or financial transactions. Here are some commonly available additional coverage options:

- Legal Expenses: Some collateral insurance policies may include coverage for legal expenses incurred by the lender in enforcing their rights or pursuing legal action related to the collateral. This coverage helps offset the costs associated with legal proceedings and strengthens the lender’s position in protecting their investment.

- Loss of Income: Certain collateral insurance policies may offer coverage for the loss of income if the collateral is income-generating, such as rental properties or equipment. This coverage compensates the lender if the income stream from the collateral is disrupted due to damage, destruction, or other covered events.

- Appraisal and Inspection Costs: Collateral insurance policies may also provide coverage for the costs associated with appraisals or inspections of the collateral. This ensures that lenders can assess the value or condition of the collateral without incurring additional out-of-pocket expenses.

- Environmental Liability: In cases where the collateral involves properties or assets with potential environmental risks, collateral insurance may offer coverage for environmental liabilities. This protects the lender from financial burdens arising from pollution, contamination, or other environmental issues related to the collateral.

- Force Majeure Events: Some collateral insurance policies may have provisions to cover losses resulting from force majeure events, such as natural disasters, political unrest, or other unforeseen circumstances. This additional coverage protects both lenders and borrowers from sudden and uncontrollable events that could impact the collateral’s value.

It is important for both lenders and borrowers to carefully review the collateral insurance policy to understand which additional coverage options are available and whether they align with their specific needs. Not all insurance providers may offer the same set of additional coverage options, so it is essential to choose a policy that best suits the requirements of the given loan or financial transaction.

By incorporating these additional coverage options, collateral insurance provides an extra layer of protection and allows for a more comprehensive risk management strategy. It ensures that both lenders and borrowers are adequately covered against unexpected events or expenses related to the collateral.

Exclusions and Limitations

While collateral insurance provides valuable coverage for lenders and borrowers, it is important to be aware of the exclusions and limitations within the policy. Understanding these restrictions is crucial for managing expectations and ensuring that the insurance coverage meets the specific needs of the loan or financial transaction. Here are some common exclusions and limitations to consider:

- Pre-Existing Damage: Collateral insurance policies typically do not cover pre-existing damage or conditions. This means that any damage already present at the time the policy is issued may not be eligible for coverage. It is important to thoroughly inspect the collateral and address any existing damage before obtaining the insurance policy.

- Intentional Acts: Insurance policies generally do not cover losses resulting from intentional acts or fraud. If a borrower intentionally causes damage to the collateral, the insurer may deny the claim. It is important for borrowers to act responsibly and avoid any actions that may undermine the coverage provided by the collateral insurance policy.

- Normal Wear and Tear: Collateral insurance typically does not cover losses resulting from normal wear and tear. This includes natural deterioration over time or expected maintenance issues. It is the responsibility of the borrower to properly maintain and care for the collateral to prevent damage and minimize the risk of loss.

- Excluded Events: Insurance policies often list specific events or circumstances that are excluded from coverage. This may include certain natural disasters, acts of war, or specific types of losses. Borrowers and lenders should carefully review the policy to understand which events or circumstances are excluded from coverage.

- Policy Limits and Deductibles: Collateral insurance policies may have limits on the maximum amount of coverage provided or deductibles that must be paid before the insurance coverage applies. Borrowers and lenders should be aware of these limits and deductibles to ensure they align with their needs and expectations.

- Non-Compliance with Policy Terms: Failure to comply with the terms and conditions set forth by the collateral insurance policy may result in the denial of coverage. For example, if the borrower fails to pay the insurance premium or breaches any other policy requirement, the insurer may not provide coverage in the event of a loss. It is crucial for both borrowers and lenders to understand and adhere to the policy terms to maintain the validity of the coverage.

It is recommended to carefully review the collateral insurance policy and discuss any questions or concerns with the insurer or an insurance professional. Understanding the exclusions and limitations helps manage expectations and ensures that both borrowers and lenders have a clear understanding of the coverage provided by the collateral insurance policy.

Importance of Collateral Insurance

Collateral insurance plays a crucial role in the world of lending and financial risk management. It offers a myriad of benefits for both borrowers and lenders involved in loan or financial transactions. Here are some key reasons why collateral insurance is important:

- Protection for Lenders: Collateral insurance provides a level of protection for lenders by ensuring that their investment is safeguarded in case of borrower default. It reduces the lender’s exposure to risk and enhances their confidence in extending credit, thereby enabling them to offer loans at more favorable terms and interest rates.

- Enhanced Borrowing Opportunities: For borrowers, collateral insurance allows them to secure loans more easily and at more competitive rates. By offering additional security in the form of collateral insurance, borrowers strengthen their creditworthiness and increase their chances of loan approval.

- Reduced Financial Risk: Collateral insurance helps mitigate financial risks for both lenders and borrowers. Lenders can recover a portion of their investment in the event of collateral loss or damage, minimizing their potential losses. Similarly, borrowers have the assurance that their liability is limited to the value of the collateral, reducing their financial risk as well.

- Promotes Financial Stability: By providing protection for lenders and borrowers, collateral insurance contributes to overall financial stability. It reduces the likelihood of loan defaults and financial crises, as the risks associated with lending are mitigated. This stability benefits individuals, businesses, and the economy as a whole.

- Facilitates Risk Management: Collateral insurance is an essential risk management tool. It allows lenders to assess and manage the risks associated with their loans and financial transactions more effectively. By providing coverage for various types of collateral and liability, collateral insurance helps lenders identify and mitigate potential risks in their lending portfolio.

- Promotes Greater Trust and Confidence: Collateral insurance instills trust and confidence in both borrowers and lenders. Borrowers feel more secure knowing that their collateral is protected, while lenders have greater confidence in extending credit when collateral is backed by insurance. This mutual trust enhances the overall lending environment and fosters stronger relationships between borrowers and lenders.

Overall, the importance of collateral insurance cannot be overstated. It provides a safety net for lenders, enables borrowers to access financing more easily, and promotes stability and risk management in the lending industry. Whether it is coverage for property, assets, liabilities, or loans, collateral insurance plays a vital role in mitigating risks and ensuring the smooth functioning of the lending ecosystem.

Conclusion

Collateral insurance is an essential component of financial risk management, providing protection for lenders and borrowers involved in loan or financial transactions. It offers coverage for property, assets, liabilities, and loans, ensuring that the interests of both parties are safeguarded.

By offering comprehensive coverage for various types of collateral, collateral insurance mitigates the financial risks associated with lending. It protects lenders by reducing their exposure to risk, allowing them to provide loans at more favorable terms and interest rates. For borrowers, collateral insurance enhances their creditworthiness and increases their chances of loan approval, providing them with access to financing and competitive rates.

The importance of collateral insurance extends beyond individual transactions. It promotes financial stability, as the risks associated with lending are mitigated, reducing the likelihood of loan defaults and financial crises. Collateral insurance also facilitates effective risk management for lenders, allowing them to assess and manage the risks associated with their lending portfolio more efficiently.

Furthermore, collateral insurance enhances trust and confidence between borrowers and lenders. Borrowers feel secure knowing that their collateral is protected, while lenders have greater confidence in extending credit when backed by insurance. This mutual trust strengthens the lending ecosystem and fosters stronger relationships between borrowers and lenders.

In conclusion, collateral insurance is a vital tool in the world of lending and finance. It provides protection, reduces financial risk, promotes stability, facilitates risk management, and enhances trust between borrowers and lenders. By understanding the various types of collateral insurance coverage, borrowers and lenders can effectively navigate the lending landscape and ensure the security of their financial transactions.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance