Finance

What Is Correspondent Banking

Published: October 13, 2023

Discover the role of correspondent banking in the world of finance and learn how it facilitates international transactions and strengthens global economic relationships.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Correspondent Banking

- How Correspondent Banking Works

- Role of Correspondent Banks

- Advantages of Correspondent Banking

- Disadvantages of Correspondent Banking

- Regulatory Challenges in Correspondent Banking

- Anti-Money Laundering and Correspondent Banking

- Recent Trends in Correspondent Banking

- Conclusion

Introduction

Correspondent banking is an essential component of the global financial system that enables banks to conduct business and facilitate cross-border transactions. It serves as the backbone of international trade, allowing banks to provide services to their customers across different jurisdictions.

In simple terms, correspondent banking can be defined as a relationship between two banks, where one acts as the “correspondent” and provides various banking services to the other, known as the “respondent” or “local” bank. These services include facilitating payments, providing access to foreign currency, and offering trade finance solutions.

The correspondent banking system enables smaller or local banks to access services and expertise that they may not have in-house, allowing them to offer a wider range of financial products and services to their customers. It also helps in mitigating risks by enabling banks in different countries to collaborate and share information about customers and transactions.

Correspondent banking operates on a network of relationships established between banks around the world. This network is crucial for facilitating international trade and cross-border transactions, connecting banks across different countries and time zones.

In recent years, correspondent banking has faced various challenges, particularly related to compliance with regulations and risks associated with money laundering and terrorism financing. Therefore, it is important for banks and financial institutions to have a thorough understanding of how correspondent banking works and the potential risks and benefits it brings.

Definition of Correspondent Banking

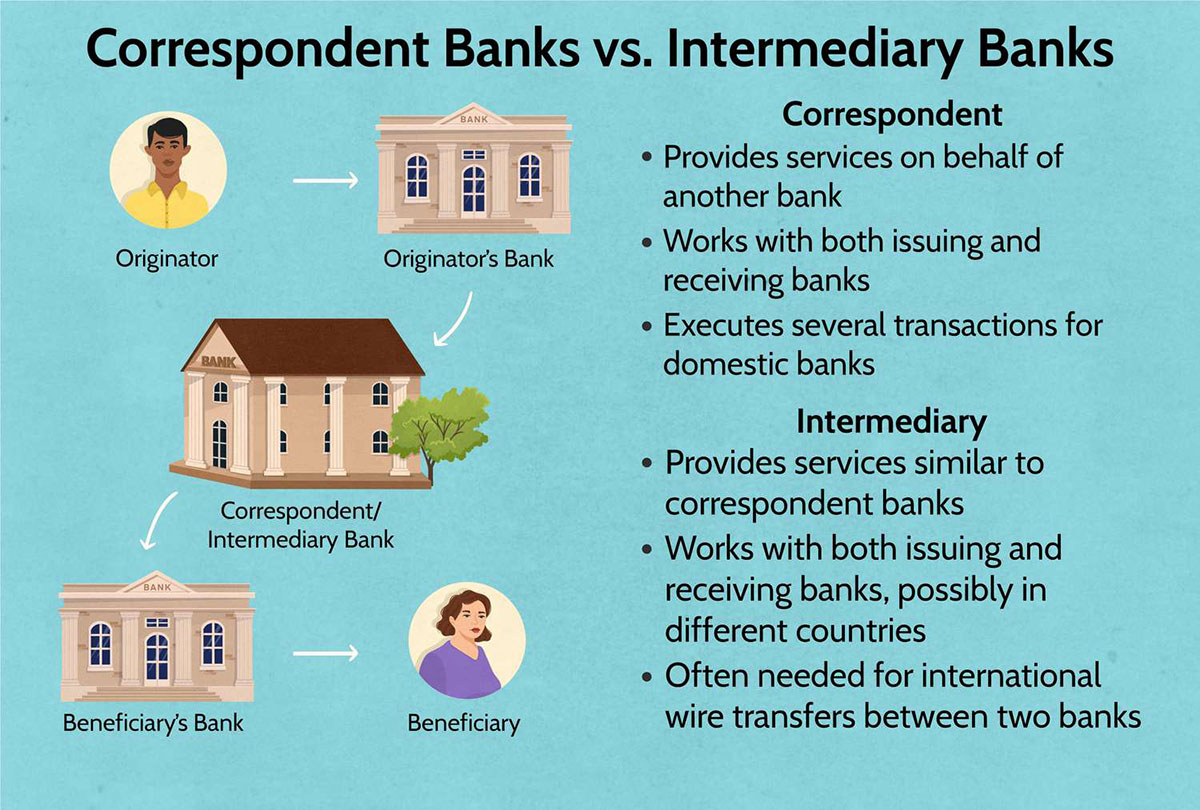

Correspondent banking is a relationship between two banks, where one bank (the correspondent bank) provides a range of banking services to another bank (the respondent or local bank) to facilitate cross-border transactions and international trade. It involves the exchange of funds, information, and services between banks located in different countries or regions.

Correspondent banking allows local banks to access services and capabilities that they may not have in-house. The correspondent bank acts as an intermediary, providing services such as foreign currency exchange, cash management, payment processing, trade financing, and even compliance with regulatory requirements.

In simpler terms, correspondent banking can be seen as a partnership between banks, where one bank utilizes the services and expertise of another bank to serve its customers’ global needs. This relationship enhances the global reach and capabilities of the local bank, strengthening its ability to conduct international business.

Correspondent banking operates through a network of relationships established between banks worldwide. Large international banks often act as correspondent banks, leveraging their vast networks and expertise to offer services to smaller, local banks.

These relationships are typically established through a contractual agreement that outlines the terms of the correspondent banking services, including fees, responsibilities, and the scope of services provided. The agreement also sets out the due diligence requirements and compliance standards that the respondent bank must adhere to.

The correspondent bank may require the local bank to maintain a correspondent account, which serves as a hub for processing transactions and facilitating communication between the two banks. This account allows the correspondent bank to hold funds on behalf of the local bank and conduct various banking activities on its behalf.

In summary, correspondent banking is a vital component of the global financial system that enables banks to facilitate cross-border transactions, access foreign currency, and provide a wide range of financial services to their customers. It strengthens the global connectivity of banks, supporting international trade and economic growth.

How Correspondent Banking Works

Correspondent banking operates through a series of interconnected relationships and processes that facilitate cross-border transactions. Here is a step-by-step overview of how correspondent banking works:

- Establishing a Correspondent Relationship: The respondent or local bank identifies a correspondent bank that has the desired capabilities and global reach. Both banks enter into a mutually beneficial agreement that outlines the terms of the correspondent banking services.

- Due Diligence and Know Your Customer (KYC) Requirements: The respondent bank undergoes a comprehensive due diligence process conducted by the correspondent bank. This process involves verifying the identity of the respondent bank, assessing its financial stability, and ensuring compliance with regulatory requirements. The correspondent bank also conducts in-depth checks on the respondent bank’s customers to mitigate the risk of money laundering or other illicit activities.

- Establishing Correspondent Accounts: The respondent bank opens a correspondent account with the correspondent bank. This account serves as the main channel for conducting correspondent banking transactions. Funds can be held in various currencies depending on the needs of the respondent bank.

- Transaction Initiation: The respondent bank initiates a cross-border transaction on behalf of its customer, such as an international payment or trade finance request. The local bank provides all necessary transaction details, including the beneficiary’s account information, payment amount, and purpose of the transaction.

- Payment Processing: The respondent bank sends the transaction details to the correspondent bank through secure communication channels. The correspondent bank verifies the transaction information and processes the payment, ensuring compliance with international regulations and guidelines.

- Funds Transfer: The correspondent bank deducts the required amount from the respondent bank’s correspondent account, debiting the local bank’s funds. The correspondent bank then transfers the funds to the beneficiary bank, either directly or through its own correspondent network, based on the beneficiary’s account information.

- Transaction Reporting: The correspondent bank provides transaction reports to the respondent bank, detailing the status and outcome of each transaction. This helps maintain transparency and enables both banks to track the flow of funds.

- Account Reconciliation: The respondent bank reconciles its correspondent account periodically to ensure accurate recording of transactions and availability of funds. Any discrepancies or issues are addressed through communication between the correspondent and respondent banks.

This cyclic process of communication, transaction initiation, payment processing, and reconciliation forms the foundation of correspondent banking. It enables banks to offer seamless cross-border services to their customers while ensuring compliance with regulatory requirements and risk mitigation.

Role of Correspondent Banks

Correspondent banks play a crucial role in facilitating global transactions and supporting the international operations of other banks. Here are some key roles that correspondent banks fulfill:

- Payment Facilitation: Correspondent banks serve as intermediaries in cross-border payments, enabling banks to settle transactions in different currencies. They facilitate the transfer of funds between the respondent bank and the beneficiary bank, ensuring timely and secure payments. This role is vital for international trade and enables businesses to engage in global transactions smoothly.

- Foreign Currency Services: Correspondent banks provide access to foreign currencies, allowing local banks to meet the needs of their customers engaged in international trade and cross-border transactions. The correspondent bank can hold various currencies in their correspondent accounts, making it easier for the local bank to conduct foreign currency exchange and cross-border remittances.

- Trade Finance: Correspondent banks offer trade finance solutions to support import and export activities. They provide letters of credit, guarantees, and other trade finance instruments that mitigate risks and facilitate international trade transactions. The correspondent bank’s expertise in trade finance ensures smooth and secure trade transactions between different countries.

- Liquidity Management: Correspondent banks provide liquidity management services to respondent banks, allowing them to efficiently manage their cash flows. This includes cash pooling, cash concentration, and cash forecasting solutions that help streamline the financial operations of the respondent bank.

- Risk Mitigation: Correspondent banks assist in mitigating risks associated with cross-border transactions. They perform due diligence on the respondent bank and its customers to ensure compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations. Through their comprehensive risk assessment processes, correspondent banks contribute to the stability and integrity of the global financial system.

- Financial Services Expertise: Correspondent banks possess in-depth knowledge and expertise in various financial services. They offer advice and guidance to respondent banks on matters related to international banking, regulatory compliance, and risk management. This support helps local banks strengthen their capabilities and expand their range of services.

- Networking Opportunities: Correspondent banks operate extensive networks of relationships with other banks around the world. This network provides respondent banks with opportunities to expand their reach, establish new partnerships, and access markets that may otherwise be challenging to enter. The correspondent bank’s network can serve as a valuable source of business connections and strategic alliances.

Overall, correspondent banks form an essential link in the global financial system, supporting the international operations of banks and facilitating seamless cross-border transactions. Their role in payment facilitation, foreign currency services, trade finance, liquidity management, risk mitigation, financial expertise, and networking opportunities enables banks to provide comprehensive and efficient services to their customers in the global marketplace.

Advantages of Correspondent Banking

Correspondent banking offers several advantages to both respondent banks and their customers. Here are some key benefits of utilizing correspondent banking services:

- Enhanced Global Reach: Correspondent banking allows local banks to expand their global reach and offer a wide range of international banking services to their customers. By partnering with correspondent banks, local banks can access foreign currency services, facilitate cross-border payments, and provide trade finance solutions, enabling them to meet the needs of their customers engaged in international transactions.

- Access to Expertise: Correspondent banks bring a wealth of expertise and knowledge in various financial services. Local banks can tap into this expertise to enhance their capabilities and offer specialized services that they may not have in-house. Correspondent banks can provide guidance on regulatory compliance, risk management, and other aspects of international banking, enabling local banks to navigate complex global markets more effectively.

- Efficient Payment Processing: Correspondent banking streamlines the process of international payments. Local banks can leverage the correspondent bank’s infrastructure and network to process cross-border transactions efficiently. This helps reduce settlement times, improve transparency, and enhance the overall payment experience for customers, especially in complex international transactions.

- Trade Finance Support: Correspondent banks offer trade finance solutions, such as letters of credit and guarantees, to support import/export activities. These services help mitigate risks associated with international trade and provide financial support to businesses engaged in cross-border transactions. Correspondent banks can provide expertise in trade finance regulations and practices, ensuring smooth and secure trade transactions.

- Access to Global Network: Correspondent banks have extensive networks of relationships with other banks worldwide. This network provides local banks with valuable opportunities for business expansion, establishing new partnerships, and accessing markets they may not have direct access to. The correspondent bank’s network can serve as a gateway to new business connections and strategic alliances.

- Liquidity Management: Correspondent banking offers liquidity management services that enable local banks to optimize their cash flows. These services include cash pooling, cash concentration, and cash forecasting, which help improve cash management efficiency and enhance the overall financial operations of the local bank.

- Risk Mitigation: Correspondent banks play a crucial role in mitigating risks associated with cross-border transactions. Through their stringent due diligence processes and compliance with regulatory requirements, correspondent banks help ensure that local banks and their customers are operating within legal frameworks. This helps combat money laundering, terrorism financing, and other illicit activities, contributing to the overall stability and integrity of the global financial system.

In summary, correspondent banking offers numerous advantages to respondent banks by enhancing their global reach, providing access to expertise, streamlining payment processing, supporting trade finance activities, facilitating networking opportunities, aiding in liquidity management, and mitigating risks. These benefits enable local banks to provide comprehensive and efficient international banking services to their customers, contributing to their growth and success in the global marketplace.

Disadvantages of Correspondent Banking

Despite its many advantages, correspondent banking also presents some challenges and disadvantages that banks and institutions need to consider. Here are some of the key drawbacks associated with correspondent banking:

- Costs: Engaging in correspondent banking can be costly for respondent banks. They may incur fees for services provided by the correspondent bank, such as foreign exchange transactions, payment processing, and trade finance services. These costs can affect the profitability of the respondent bank and may be passed on to their customers, leading to higher fees and charges for international transactions.

- Reliance on Correspondent Banks: Respondent banks rely heavily on the services and capabilities of correspondent banks. This dependency can create vulnerabilities, as disruptions or issues with the correspondent bank can impact the respondent bank’s ability to process transactions and serve its customers. Changes in correspondent banking relationships or the withdrawal of correspondent banks from certain regions can also create difficulties for respondent banks in finding alternative banking solutions.

- Regulatory Compliance Burden: Correspondent banking involves strict regulatory compliance requirements, particularly in the areas of anti-money laundering (AML) and counter-terrorism financing (CTF) measures. Respondent banks must meet these compliance standards set by correspondent banks and regulatory authorities. This requires significant resources and efforts to implement robust compliance frameworks, conduct due diligence on customers and transactions, and maintain accurate records. Non-compliance with these regulations can result in severe penalties and reputational damage.

- Risk of Money Laundering and Financial Crimes: Correspondent banking has been associated with higher risks of money laundering, terrorist financing, and other illicit activities. Given the complex nature of cross-border transactions and the multiple parties involved, it can be challenging to detect and prevent financial crimes. Respondent banks must have robust AML and CTF procedures in place to mitigate these risks, including thorough customer due diligence, transaction monitoring, and reporting suspicious activities to regulatory authorities.

- Limited Transparency: The nature of correspondent banking relationships can sometimes limit transparency in financial transactions. Due to the multitude of intermediaries involved, it can be challenging to trace the origin and movement of funds. This lack of transparency may raise concerns around illicit financial activities and hinder efforts to combat money laundering and terrorist financing.

- Complexity and Documentation Requirements: Correspondent banking transactions often involve complex documentation and verification processes. Respondent banks must gather and provide comprehensive information about their customers, transactions, and associated parties. This can create administrative burdens and potential delays in transaction processing, impacting the efficiency and speed of cross-border payments and trade finance activities.

Despite these disadvantages, many banks still find the benefits of correspondent banking outweigh the challenges. However, it is essential for banks and financial institutions to be aware of these drawbacks and take appropriate measures to mitigate the potential risks associated with correspondent banking relationships.

Regulatory Challenges in Correspondent Banking

Correspondent banking faces significant regulatory challenges, primarily due to the risks associated with money laundering, terrorist financing, and other illicit activities. Regulatory authorities have implemented stringent measures to ensure compliance and mitigate these risks, which has led to a number of challenges for banks and financial institutions involved in correspondent banking. Here are some of the key regulatory challenges:

- Anti-Money Laundering (AML) Compliance: Correspondent banks have the responsibility to ensure compliance with AML regulations to prevent money laundering activities. This requires applying robust Know Your Customer (KYC) procedures, conducting thorough due diligence on customers and counterparties, and implementing transaction monitoring systems. However, complying with these regulations can be complex and resource-intensive, requiring extensive documentation, ongoing monitoring, and reporting of suspicious activities.

- Counter-Terrorism Financing (CTF) Compliance: Correspondent banks also need to address the risks of financing terrorism. They are required to adopt measures to identify and prevent transactions that could fund terrorist activities or entities. This includes screening transactions, analyzing patterns, and reporting any suspicious activities. However, the evolving nature of terrorist financing methods presents ongoing challenges in identifying and mitigating these risks.

- Fragmented Regulatory Frameworks: Correspondent banking operates across borders, which means dealing with multiple regulatory frameworks. These frameworks can vary across jurisdictions, making it challenging for banks to navigate and ensure compliance with all applicable regulations. The lack of harmonization and standardization in regulatory requirements adds complexity and increases compliance costs for banks involved in correspondent banking relationships.

- De-Risking: As a result of increased regulatory scrutiny and compliance costs, some correspondent banks have chosen to reduce or terminate correspondent banking relationships with certain regions or categories of customers. This practice is known as de-risking and can lead to reduced access to correspondent banking services, particularly for smaller banks and individuals in higher-risk regions. De-risking can have negative consequences for financial inclusion and international trade, creating challenges for these affected regions.

- Data Protection and Privacy: Correspondent banking involves the exchange of sensitive customer information between banks. Maintaining data protection and privacy while complying with regulatory requirements can be a challenge. Banks must implement robust data protection measures to safeguard customer information while ensuring compliance with data privacy laws across jurisdictions.

- Regulatory Reporting and Record-Keeping: Regulatory authorities require banks to maintain comprehensive records and submit regular reports on correspondent banking activities. Compliance with these reporting obligations can be time-consuming and resource-intensive, putting a burden on banks to gather and analyze large volumes of data in a timely and accurate manner.

To address these regulatory challenges, banks and financial institutions involved in correspondent banking must allocate sufficient resources to compliance efforts, invest in advanced technology solutions for AML and CTF monitoring, enhance transparency in their operations, strengthen due diligence processes, and establish strong partnerships with correspondent banks to ensure adherence to regulatory requirements across jurisdictions.

Anti-Money Laundering and Correspondent Banking

Correspondent banking plays a critical role in the global financial system, but it also presents risks for money laundering and other illicit activities. As a result, correspondent banks and financial institutions involved in correspondent banking must adhere to robust anti-money laundering (AML) measures to prevent and detect money laundering activities. Here are some key aspects of AML in the context of correspondent banking:

- Know Your Customer (KYC) Procedures: Correspondent banks must implement stringent KYC procedures to verify the identity of their respondent banks and their customers. This involves gathering comprehensive information about the respondent bank’s ownership structure, management, and customer base. Additionally, correspondent banks must conduct ongoing due diligence to monitor changes in risk profiles and ensure compliance with AML regulations.

- Transaction Monitoring: Correspondent banks are responsible for monitoring transactions conducted through their correspondent accounts. They must implement robust transaction monitoring systems to detect any suspicious or unusual activities. Transaction monitoring involves analyzing transaction patterns, identifying high-risk transactions, and reporting suspicious activities to regulatory authorities.

- Enhanced Due Diligence (EDD): When correspondent banks deal with high-risk respondent banks or customers, they must apply enhanced due diligence measures. This includes conducting more in-depth checks on the respondent bank’s ownership, source of funds, anticipated transaction activity, and assessing the correspondent account’s purpose and expected use.

- Reporting Obligations: Correspondent banks have a duty to report suspicious transactions to the appropriate regulatory authorities. They are required to have robust reporting mechanisms in place and ensure timely submission of Suspicious Activity Reports (SARs) when they identify transactions that may be related to money laundering or illicit activities.

- Information Sharing: Correspondent banks often engage in information sharing to combat money laundering and criminal activities. They may share information about their respondent banks, customers, and transactions to enhance due diligence and mitigate risks. However, this information sharing is subject to strict confidentiality provisions and must comply with data protection and privacy regulations.

- Regulatory Compliance: Correspondent banks must adhere to AML regulations and guidelines set by regulatory authorities in their respective jurisdictions. This includes national AML laws and regulations, as well as international standards such as the Financial Action Task Force (FATF) recommendations. Correspondent banks need to keep up to date with changes in regulations and adjust their AML frameworks accordingly.

- Staff Training and Awareness: Correspondent banks must provide ongoing training and awareness programs to their staff to ensure they are well-informed about AML requirements and can effectively identify and report suspicious activities. Training programs should cover topics such as recognizing red flags, understanding typologies of money laundering, and staying up to date with emerging AML trends.

By implementing robust AML measures, correspondent banks contribute to the overall integrity and stability of the global financial system. Compliance with AML regulations helps prevent money laundering, terrorist financing, and other illicit activities, ensuring the transparency and trustworthiness of correspondent banking relationships.

Recent Trends in Correspondent Banking

Correspondent banking continues to evolve and adapt to the changing dynamics of the global financial landscape. Here are some recent trends shaping the industry:

- De-Risking and Decline in Correspondent Relationships: Over the past few years, there has been a trend of de-risking within correspondent banking. Large correspondent banks have reduced or terminated correspondent relationships with respondent banks in higher-risk regions or industries. This has led to reduced access to correspondent banking services for certain banks and individuals, impacting financial inclusion and international trade in these areas.

- Emerging Technologies: Correspondent banking is being influenced by advancements in technology. Distributed ledger technology, such as blockchain, is being explored as a potential solution for enhancing transparency, reducing settlement times, and improving efficiency in cross-border transactions. Artificial intelligence and machine learning are also being utilized to enhance AML and transaction monitoring processes.

- Collaboration and Partnerships: Financial institutions are increasingly recognizing the importance of collaboration and partnerships in correspondent banking. This includes forming alliances with fintech companies to leverage innovative solutions, partnering with other banks to expand their correspondent network, or joining consortiums to share resources and knowledge. These collaborations can enhance efficiency, reduce costs, and strengthen compliance efforts.

- Focus on Enhancing AML Efforts: Given the heightened global focus on combatting money laundering and terrorist financing, correspondent banks are dedicating more resources to strengthen their AML frameworks. This includes investing in advanced AML technology solutions, conducting thorough due diligence on respondent banks and customers, and ensuring ongoing compliance with evolving regulatory requirements.

- Regulatory Changes and Harmonization: Regulatory authorities are implementing changes to enhance AML controls and promote greater transparency in correspondent banking. There is an increased emphasis on information sharing and cooperation among regulatory institutions to combat financial crimes more effectively. Efforts are being made to harmonize AML regulations across jurisdictions to create consistency and reduce the complexity faced by correspondent banks.

- Focus on Financial Inclusion: Correspondent banking is also influenced by efforts to promote financial inclusion. Regulatory authorities and international organizations are working to address the challenges faced by regions and sectors that have limited access to correspondent banking services. Initiatives such as the Global Remittances Working Group and the Financial Stability Board’s Action Plan on Correspondent Banking aim to enhance access to safe and affordable financial services for all.

These recent trends reflect the ongoing evolution of correspondent banking as it seeks to address challenges related to AML compliance, technological advancements, regulatory changes, and financial inclusion. By adapting to these trends, correspondent banks can enhance their operations, strengthen risk management practices, and contribute to a more inclusive and secure global financial system.

Conclusion

Correspondent banking plays a critical role in facilitating global financial transactions and supporting international trade. It enables banks to access foreign currency, provide cross-border payment services, and offer trade finance solutions to their clients. While correspondent banking offers numerous advantages, such as enhanced global reach, access to expertise, and efficient payment processing, it also poses challenges and risks that need to be addressed.

Regulatory compliance, particularly in the areas of anti-money laundering (AML) and counter-terrorism financing (CTF), is a significant challenge for correspondent banks. They must adhere to stringent AML and KYC procedures, implement robust transaction monitoring systems, and report suspicious activities to regulatory authorities. The fragmented regulatory frameworks and the complexity of cross-border transactions make compliance a complex and resource-intensive task.

Recent trends in correspondent banking reflect a focus on enhancing AML efforts, exploring emerging technologies like blockchain, promoting collaboration and partnerships, and addressing the challenges of de-risking and financial inclusion. Regulatory changes and efforts towards harmonization are being made to strengthen controls and promote transparency in correspondent banking.

Despite the challenges, correspondent banking remains essential for the global financial system. It enables banks to serve their customers’ international financial needs, facilitates cross-border trade, and contributes to economic growth. Correspondent banks must remain vigilant, adapt to evolving regulatory requirements, and employ technological advancements to ensure the integrity and security of their operations.

In conclusion, correspondent banking is a vital component of the global financial ecosystem. By embracing regulatory compliance, adopting innovative technologies, fostering collaboration, and addressing issues related to de-risking and financial inclusion, correspondent banks can continue to facilitate seamless cross-border transactions and support the growth of global trade.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance