Finance

What Is Participative Budgeting

Published: October 11, 2023

Learn about participative budgeting and its role in finance. Discover how this collaborative approach empowers stakeholders to have a say in budget creation and decision-making.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Participative budgeting is a management approach that involves including employees at all levels in the budgeting process. It is a collaborative and inclusive method that allows employees to contribute their knowledge and insights to the budget creation and decision-making processes. This approach goes beyond traditional top-down budgeting, where upper management dictates the budget without input from other team members.

Participative budgeting aims to foster a sense of ownership and accountability among employees, as they have a say in the resource allocation and financial planning of their department or organization. By involving employees in the budgeting process, organizations can tap into their expertise, creativity, and knowledge of day-to-day operations, resulting in more accurate and realistic budgets.

Participative budgeting is particularly prevalent in the finance industry, where financial planning and budgeting play a critical role in achieving organizational goals. In this fast-paced and competitive industry, organizations need to adapt quickly to changing market conditions, and involving employees in the budgeting process can help them respond more effectively.

In this article, we will explore the concept of participative budgeting in more detail, including its definition, benefits, process, potential challenges, and real-world examples. Whether you are a finance professional or simply interested in understanding how organizations involve their employees in financial decision-making, this article will provide you with valuable insights.

Definition of Participative Budgeting

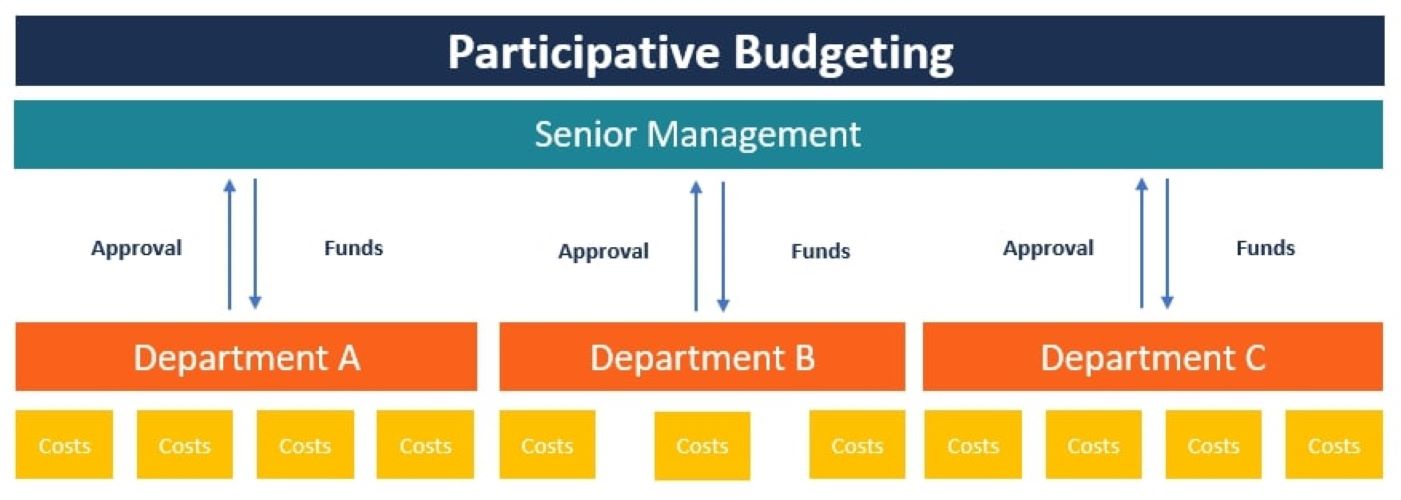

Participative budgeting, also known as inclusive budgeting or collaborative budgeting, is a management approach that involves employees at various levels in the budget creation and decision-making processes. It is a departure from the traditional top-down budgeting approach, where budgetary decisions are made solely by upper management without input from other team members.

In participative budgeting, employees, including managers and non-managers, are encouraged to actively contribute to the formation of the budget. They are given the opportunity to provide input based on their knowledge of day-to-day operations, departmental needs, and organizational goals.

Under this approach, the budget is seen as a shared responsibility, with employees having a direct stake in its creation and implementation. Rather than being dictated from above, the budget is a collaborative effort that takes into consideration the diverse perspectives and insights of those involved. Each department or team within the organization is typically responsible for creating their own budget, which is then consolidated into an overall organizational budget.

Participative budgeting can take different forms, depending on the level of employee involvement. It can range from consulting employees for input to delegating them the authority to make decisions regarding budget allocation. The level of participation may vary depending on factors such as organizational culture, management style, and the nature of the decision being made.

Overall, participative budgeting aims to promote transparency, accountability, and employee engagement. By involving employees in the budgeting process, organizations can harness their collective wisdom, improve decision-making, increase buy-in, and foster a sense of ownership and responsibility.

Benefits of Participative Budgeting

Participative budgeting offers several benefits for organizations that choose to adopt this collaborative approach. Let’s explore some of the key advantages:

- Increased Employee Engagement: By involving employees in the budgeting process, organizations can boost employee engagement and morale. Employees feel valued and empowered when their opinions and expertise are taken into account, leading to increased job satisfaction and motivation.

- Enhanced Accuracy and Realism: Participative budgeting allows for a more accurate and realistic budget. Employees who are directly involved in day-to-day operations have a better understanding of the resources needed to achieve their goals. Their input helps in identifying potential cost-saving measures and ensuring that revenue and expense projections are more in line with actual outcomes.

- Better Decision-Making: With a participative budgeting approach, decision-making becomes a collective effort. Employees bring diverse perspectives and insights to the table, leading to more well-rounded and informed decisions. This collaborative decision-making process can result in better resource allocation and strategic planning.

- Increased Ownership and Accountability: When employees participate in the budgeting process, they feel a sense of ownership and responsibility towards achieving the budget targets. This increased accountability can lead to improved performance and a greater focus on achieving financial goals.

- Improved Communication and Collaboration: Participative budgeting fosters open communication and collaboration between different departments and levels within the organization. It breaks down silos and encourages cross-departmental cooperation, leading to a more integrated and cohesive budgeting process.

- Adaptability to Changing Conditions: In an ever-changing business environment, organizations need to be agile and responsive. Participative budgeting allows for easier adaptation to changes by involving employees who are on the front lines of the operations. They can quickly identify emerging challenges or opportunities and suggest adjustments to the budget accordingly.

Overall, participative budgeting promotes a culture of collaboration, transparency, and engagement within an organization. It harnesses the collective intelligence of employees, leading to more accurate budgets, better decision-making, and improved overall performance. By involving employees in the budgeting process, organizations can create a more empowered and motivated workforce that is aligned with organizational goals.

Process of Participative Budgeting

The process of participative budgeting involves several key steps that organizations can follow to incorporate employee input into the budget creation and decision-making process. While the specific process may vary depending on the organization and its unique needs, the following steps provide a general framework:

- Communication and Goal Setting: The organization communicates the budgeting process, objectives, and timeline to all employees. Clear goals and expectations are established to ensure alignment with the overall strategic direction.

- Training and Education: Employees are provided with the necessary training and education to understand the budgeting process, financial concepts, and relevant organizational policies. This empowers them to actively participate and contribute effectively.

- Data Collection and Analysis: Employees collect and analyze data relevant to their respective departments or areas of responsibility. This includes historical financial data, market trends, customer insights, and any other information that can inform the budgeting process.

- Brainstorming and Idea Generation: Employees come together in cross-functional teams or departmental meetings to brainstorm ideas, identify opportunities for improvement, and propose budgetary adjustments. This collaborative process encourages creativity and innovation.

- Budget Preparation: Based on the input and suggestions from employees, departments create their individual budgets. They consider factors such as revenue projections, expense forecasts, and resource allocation needs. Budgets are prepared using the organization’s preferred budgeting format and guidelines.

- Review and Consolidation: Departmental budgets are reviewed by managers and finance personnel to ensure alignment with organizational goals and financial feasibility. Feedback is provided, and any necessary adjustments or clarifications are made. Once the individual budgets are finalized, they are consolidated into an overall organizational budget.

- Presentation and Approval: The budget is presented to relevant stakeholders, such as upper management or the board of directors, for approval. The rationale behind the budget, including the employee input and the expected benefits, is highlighted during the presentation.

- Implementation and Monitoring: The budget is implemented, and actual financial performance is monitored continuously. Regular reviews and updates are conducted to ensure that the budget remains on track and adjustments are made as needed.

- Evaluation and Feedback: At the end of the budget period, a thorough evaluation is conducted to assess the effectiveness of the participative budgeting process. Feedback from employees and managers is collected to identify areas for improvement and refine the process for future budgeting cycles.

The process of participative budgeting is iterative and requires ongoing communication, collaboration, and evaluation to be successful. By involving employees at each stage, the organization can benefit from their insights, expertise, and commitment. This inclusive approach not only leads to a more accurate and realistic budget but also fosters a culture of engagement and ownership among employees.

Potential Challenges of Participative Budgeting

While participative budgeting has numerous benefits, it is important to acknowledge the potential challenges that organizations may encounter when implementing this approach. Identifying and understanding these challenges will help organizations navigate the process more effectively. Here are some common challenges:

- Time and Resource Constraints: Participative budgeting requires time and resources to gather employee input, analyze data, and consolidate budgets. Organizations may face challenges in allocating sufficient time and resources to the budgeting process without impacting day-to-day operations.

- Resistance to Change: Some employees may resist the shift from a traditional top-down budgeting approach to participative budgeting. This resistance can be due to a fear of losing control or a lack of understanding or trust in the process. Proper communication, training, and change management strategies are necessary to address this challenge.

- Communication and Coordination: Involving multiple stakeholders and departments in the budgeting process can pose communication and coordination challenges. Ensuring effective communication and coordination among all participants is crucial to avoid misunderstandings, conflicts, or inconsistencies in the budgeting process.

- Conflict of Interest: Participative budgeting may bring to light differing priorities and objectives within the organization. This can result in conflicts of interest, as individuals or departments advocate for their own interests rather than the overall organizational goals. Effective leadership and clear decision-making processes are essential to manage and resolve such conflicts.

- Complex Decision-Making: Involving more people in the budgeting process can sometimes lead to delayed decision-making or indecisiveness, especially when there are numerous perspectives and opinions to consider. Organizations need to establish clear decision-making frameworks to ensure timely and effective decisions while allowing for sufficient input from employees.

- Accountability and Performance: For participative budgeting to be successful, it is crucial to maintain accountability. This includes ensuring that employees are responsible for meeting their budgetary targets and that performance evaluations align with the agreed-upon budget goals. Without proper accountability measures, participative budgeting can result in lackluster performance and a failure to achieve desired outcomes.

Addressing these challenges requires a proactive approach, effective communication, and a supportive organizational culture. Organizations can overcome these hurdles by providing training and education, fostering trust and collaboration, establishing clear guidelines and decision-making processes, and ensuring accountability at all levels.

By acknowledging and tackling these potential challenges, organizations can maximize the benefits of participative budgeting and create a culture of teamwork, innovation, and ownership in their financial management practices.

Examples of Participative Budgeting in Practice

Participative budgeting has been successfully implemented by various organizations across different industries. Let’s explore a few examples of how participative budgeting has been applied in practice:

- GORE-TEX: The outdoor apparel company, GORE-TEX, is known for its collaborative and inclusive approach to budgeting. They encourage employees at all levels to contribute to the budgeting process, as they believe that those who are closest to the work have valuable insights. This participative approach has led to increased employee engagement, improved budget accuracy, and a sense of ownership among employees.

- Toyota: Toyota, a leading automotive manufacturer, is known for its participative budgeting approach called “kaizen budgeting.” They emphasize continuous improvement and involve employees in identifying cost-saving measures and efficiency improvements. The budgeting process includes cross-functional teams that work together to identify waste, eliminate non-value-adding activities, and optimize resource allocation.

- Zappos: The online shoe and clothing retailer, Zappos, implements a unique form of participative budgeting known as “holacracy.” In this decentralized management structure, employees have the authority to make budget decisions within their teams or departments. This approach empowers employees to take ownership of their budget and fosters a culture of trust, collaboration, and innovation.

- Semco Partners: Semco Partners, a Brazilian conglomerate, is renowned for its participative budgeting philosophy. They involve employees in decision-making processes, including budget creation and financial planning. Employees are encouraged to provide input, challenge assumptions, and propose changes to improve financial performance. This approach has resulted in increased employee satisfaction and a sense of shared responsibility for organizational success.

- Google: Google applies participative budgeting through its practice called “bottom-up budgeting.” Employees are given the opportunity to propose projects and allocate budgets to support their ideas. This approach encourages innovation, employee empowerment, and ensures that resources are allocated to projects that have the most potential for success.

These examples demonstrate the diverse ways in which organizations have implemented participative budgeting to improve financial management, foster employee engagement, and drive innovation. While the specific methods may vary, the underlying principle remains the same – involving employees in the budgeting process leads to more informed decision-making, increased ownership, and better outcomes.

Organizations can adapt and tailor participative budgeting to suit their unique organizational culture, industry dynamics, and strategic objectives. By doing so, they can unlock the full potential of their workforce and create a collaborative and inclusive environment that drives financial success.

Conclusion

Participative budgeting is a management approach that has gained prominence in organizations seeking to foster employee engagement, improve decision-making, and align financial goals with operational realities. By involving employees at all levels in the budgeting process, organizations tap into their expertise, creativity, and knowledge of day-to-day operations, resulting in more accurate and realistic budgets.

In this article, we explored the concept of participative budgeting, its benefits, process, potential challenges, and real-world examples. We discovered that participative budgeting offers several advantages, including increased employee engagement, enhanced accuracy, better decision-making, increased ownership and accountability, improved communication and collaboration, and adaptability to changing conditions.

However, participative budgeting does come with potential challenges, such as time and resource constraints, resistance to change, communication and coordination issues, conflicts of interest, complex decision-making, and ensuring accountability and performance. By addressing these challenges through effective communication, training, and supportive organizational practices, organizations can overcome the hurdles and reap the benefits of participative budgeting.

We also examined real-world examples of participative budgeting in practice, including companies like GORE-TEX, Toyota, Zappos, Semco Partners, and Google. These examples showcased different approaches and demonstrated the positive outcomes that organizations can achieve through participative budgeting.

In conclusion, participative budgeting offers organizations the opportunity to leverage the collective wisdom and expertise of their employees in the budgeting process. By embracing this collaborative approach, organizations can enhance their financial management practices, foster employee engagement, and drive better overall performance. Implementing participative budgeting may require a shift in organizational culture and processes, but the potential benefits make it well worth considering for any organization seeking to improve its financial decision-making and empower its workforce.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: Rachel Chua • Finance