Finance

What Is The Best Definition Of A Credit Score

Modified: March 10, 2024

Looking for the best definition of a credit score? Gain insights into the world of finance and understand how credit scores impact your financial health.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of credit scores! If you’ve ever applied for a loan, a credit card, or even rented an apartment, chances are your credit score was taken into consideration. But what exactly is a credit score? In simple terms, it is a numerical representation of an individual’s creditworthiness, which lenders use to assess the risk of lending money or extending credit. A credit score can impact various aspects of your financial life, from the interest rates you’re offered on loans to the types of credit cards you qualify for.

Understanding the ins and outs of credit scores is crucial for anyone looking to build a strong financial foundation. In this article, we will delve into the world of credit scores, exploring what they are, how they are calculated, and the factors that influence them. We will also highlight the importance of having a good credit score and provide insights on how you can improve your creditworthiness.

Whether you’re a seasoned pro or completely new to the concept, this guide will equip you with the knowledge to navigate the complexities of credit scores and make informed financial decisions.

Understanding Credit Scores

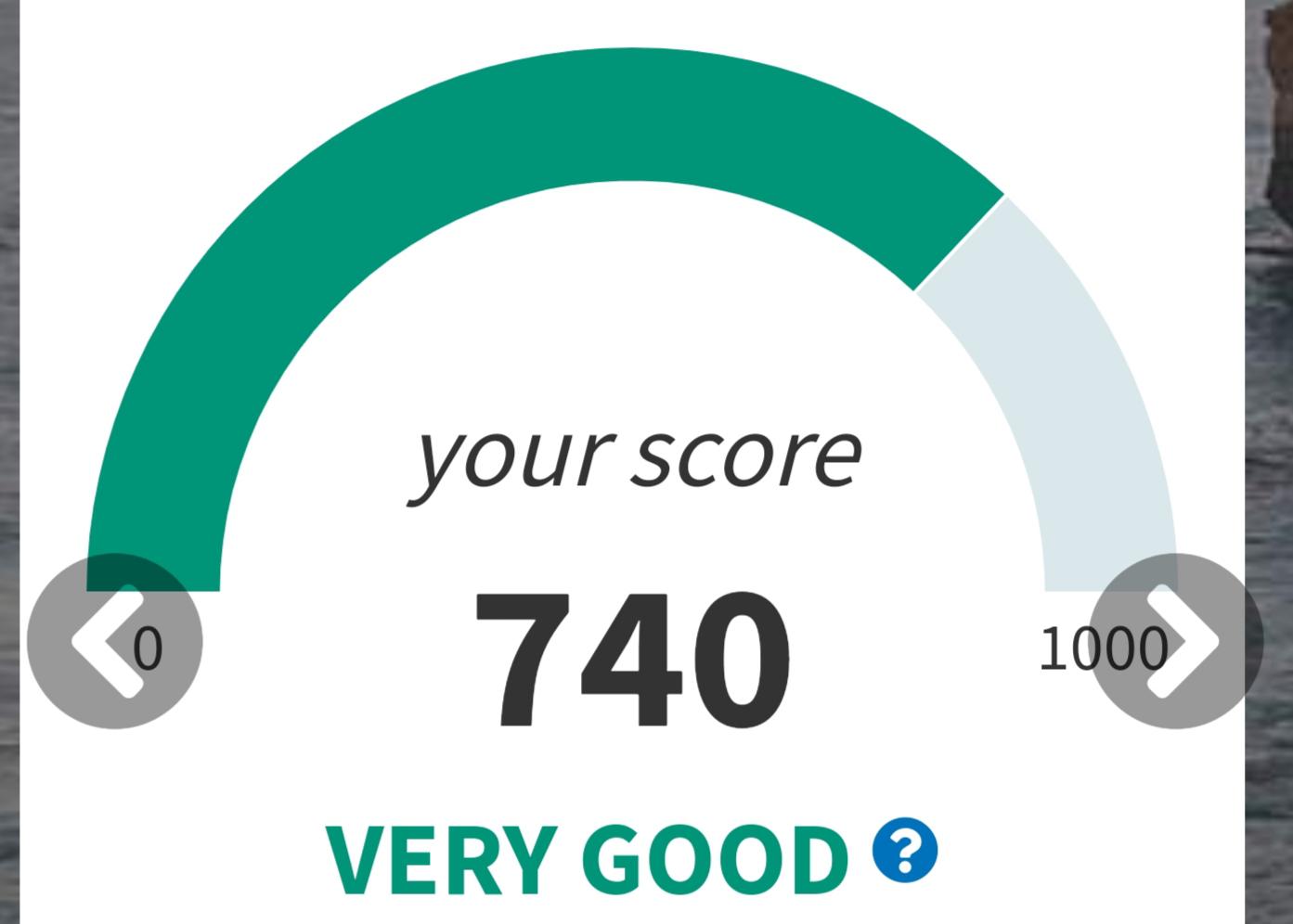

A credit score is a three-digit number that reflects a person’s creditworthiness and provides lenders with an assessment of their ability to repay debts. It is based on the individual’s credit history, which includes their borrowing and repayment behavior. Credit scores range from 300 to 850, with higher scores indicating better creditworthiness.

The most commonly used credit scoring model is the FICO Score, developed by the Fair Isaac Corporation. This model takes into account five key factors to calculate a person’s credit score:

- Payment history: This is the most influential factor in determining a credit score, as it reflects an individual’s track record of making timely payments. Any missed or late payments can have a negative impact on the score.

- Amounts owed: This factor considers the total amount of debt a person has, including credit card balances, loans, and mortgages. The ratio between the amount owed and the available credit, known as the credit utilization ratio, is also taken into account.

- Length of credit history: A longer credit history generally improves a credit score. It takes into account the age of the person’s oldest account, the average age of all accounts, and the time since the last activity on each account.

- New credit: Opening multiple new credit accounts in a short period of time can indicate financial instability and negatively affect credit scores. This factor considers the number of recently opened accounts and credit inquiries.

- Credit mix: Having a variety of credit types, such as credit cards, loans, and mortgages, can positively impact a credit score. It demonstrates responsible credit management and diversification.

It’s important to note that each credit reporting agency may have variations in their credit scoring models and the weight given to each factor. However, the general principles remain the same across the board.

A higher credit score indicates a lower risk of defaulting on payments, making it easier for individuals to access credit at favorable terms. Lenders use credit scores to evaluate loan applications and determine the interest rates and credit limits offered to borrowers. Landlords, insurance companies, and even potential employers may also consider credit scores to assess an individual’s financial reliability and responsibility.

Now that we have a basic understanding of credit scores, let’s explore the factors that can positively or negatively impact them.

Factors That Affect Credit Scores

Several factors can influence your credit score, both positively and negatively. Understanding these factors can help you make informed financial decisions and take steps to improve your creditworthiness. Here are some key factors that affect credit scores:

- Payment history: Your payment history has the most significant impact on your credit score. Making payments on time and in full demonstrates responsible financial behavior, while late or missed payments can severely harm your score.

- Amounts owed: The amount of debt you owe, particularly in relation to your available credit, affects your credit score. High credit utilization ratios can indicate financial strain and lower your score. It’s generally recommended to keep your credit utilization below 30%.

- Length of credit history: The length of time you’ve had credit accounts impacts your credit score. A longer credit history can show a track record of responsible credit management, while a shorter history may have less data for assessing creditworthiness.

- New credit: Opening multiple new credit accounts within a short period can be seen as risky behavior and lower your credit score. Similarly, a high number of credit inquiries, which occur when you apply for new credit, can have a negative impact.

- Credit mix: Having a diverse mix of credit types, such as credit cards, mortgages, and loans, can positively impact your credit score. It shows that you can handle different types of credit responsibly.

It’s important to note that these factors carry different weights in determining your credit score. Payment history and amounts owed typically have the most significant impact, followed by credit history length, new credit, and credit mix. Additionally, negative information such as bankruptcies, foreclosures, or collection accounts can have a severe and long-lasting impact on your credit score.

It’s crucial to manage these factors wisely to maintain a healthy credit score. Regularly reviewing your credit report and addressing any inaccuracies or discrepancies can also help protect your creditworthiness. By understanding the factors that influence credit scores, you can proactively take steps to improve and maintain a positive credit profile.

Importance of a Good Credit Score

A good credit score is essential for a variety of financial reasons. It plays a crucial role in determining your ability to access credit, secure favorable loan terms, and even impact other aspects of your life. Here are some reasons why maintaining a good credit score is important:

- Access to credit: A good credit score opens doors to various credit options, including loans, credit cards, and mortgage financing. Lenders use credit scores to evaluate an individual’s creditworthiness, and a higher score increases your chances of approval.

- Lower interest rates: With a good credit score, you are more likely to qualify for loans and credit cards with lower interest rates. This can save you significant amounts of money in interest payments over the life of a loan or credit card balance.

- Better credit card benefits: Credit cards tailored for individuals with good credit scores often come with attractive perks and rewards programs. These may include cash back, travel rewards, or other incentives that can add value to your financial management.

- Higher credit limits: A good credit score increases your chances of obtaining higher credit limits. This can be advantageous during emergencies or when you need to make larger purchases.

- Insurance premiums: Some insurance companies consider credit scores when determining premiums for auto, homeowners, or renters insurance. A good credit score can result in lower insurance premiums, saving you money over time.

- Housing opportunities: Landlords often use credit scores to assess potential tenants’ financial responsibility. A good credit score can increase your chances of securing a desirable rental property.

- Employment prospects: In certain industries, employers may consider credit scores as part of the hiring process. While it is not a direct reflection of job performance, a good credit score can demonstrate financial responsibility and integrity.

Building and maintaining a good credit score requires responsible financial management, such as making payments on time, keeping credit card balances low, and limiting new credit applications. Regularly monitoring your credit report and addressing any errors or discrepancies promptly is also crucial in maintaining a healthy credit profile.

Remember, a good credit score is not only advantageous in securing credit and favorable terms, but it also reflects your financial responsibility and can open up opportunities in various areas of your life. So take steps to establish and maintain a strong credit score to enhance your financial well-being.

Different Credit Score Models

While the FICO Score is the most commonly used credit scoring model, it’s important to note that there are other credit score models in use as well. These alternate models may have slight variations in how they calculate credit scores and the factors they prioritize. Here are a few notable credit score models:

- VantageScore: Developed by the three major credit reporting agencies (Equifax, Experian, and TransUnion), VantageScore is gaining popularity as an alternative to the FICO Score. It uses a similar scoring range of 300 to 850 and considers factors like payment history, credit utilization, credit mix, and recent credit behavior.

- PLUS Score: The PLUS Score is another credit scoring model commonly used by lenders. It ranges from 330 to 830 and is used primarily for educational purposes to provide consumers with a general idea of their creditworthiness.

- CE Score: The CE Score, also known as the CreditXpert Credit Score, is used by mortgage lenders to assess credit risk specifically for mortgage applications. It uses credit data to develop a credit score range of 350 to 850.

- Industry-specific scores: Some industries have developed their own credit scoring models tailored to their specific needs. For example, the FICO Auto Score and FICO Bankcard Score are used by auto lenders and credit card issuers, respectively, to evaluate creditworthiness in their respective industries.

It’s important to understand that while the basic principles of evaluating creditworthiness remain the same, credit scores may vary depending on the specific scoring model used. Each model may place different weights on certain factors or consider additional data points to generate the final credit score.

It’s also worth noting that credit scores can vary slightly between the three major credit reporting agencies due to differences in the information each agency has on file. When applying for credit, lenders may pull credit reports from one or more of these agencies, resulting in slightly different credit scores.

While the FICO Score is still the most widely accepted and used credit score model, it’s a good idea to be aware of alternative scoring models, especially when applying for specific types of credit. Understanding these different models can help you better interpret and manage your creditworthiness across different industries and lenders.

How to Check Your Credit Score

Keeping track of your credit score is essential in managing your financial health. Fortunately, checking your credit score is easier than ever. Here are several ways you can access your credit score:

- Credit monitoring services: Many credit monitoring services provide access to your credit score as part of their membership offerings. These services allow you to regularly monitor your credit report, receive alerts about changes to your credit file, and access your credit score from one or more credit bureaus.

- Free credit score services: Several websites and financial institutions offer free credit score services. These platforms provide you with your credit score, along with tools and educational resources to help you understand and improve your credit.

- Credit card statements: Some credit card issuers now include your credit score on your monthly statements. Check your credit card statement or online account to see if this feature is available to you.

- Banking apps: Many banks and credit unions now offer credit score tracking within their mobile banking apps. Check with your financial institution to see if they provide this feature as part of their banking services.

- Credit bureaus: Each of the three major credit reporting agencies—Equifax, Experian, and TransUnion—provide access to your credit score. You can request a free credit report once a year from each agency through AnnualCreditReport.com, and some agencies may offer access to your credit score through their websites for a fee.

When checking your credit score, it’s essential to use reputable sources and ensure the security of your personal information. Be cautious of scams or phishing attempts while pursuing your credit information.

It’s worth mentioning that you may have multiple credit scores depending on the scoring model used or which credit bureau’s data is used to calculate the score. Different lenders may also use different scoring models when evaluating your creditworthiness.

Regularly monitoring your credit score allows you to stay informed about your financial standing and detect any potential inaccuracies or fraudulent activities. By understanding your credit score, you can take steps to improve it and make informed decisions when seeking credit or applying for loans.

Ways to Improve Your Credit Score

If you have a less-than-ideal credit score, don’t worry. There are steps you can take to improve it over time. Here are several strategies you can implement to boost your creditworthiness:

- Pay bills on time: Consistently making timely payments is one of the most effective ways to improve your credit score. Set up automatic payments or reminders to ensure you never miss a payment.

- Reduce debt: Lowering the amount of debt you owe can positively impact your credit score. Create a debt repayment plan and focus on paying off high-interest debts first.

- Keep credit utilization low: Aim to keep your credit card balances below 30% of your available credit. High credit utilization ratios can negatively affect your credit score.

- Avoid opening unnecessary accounts: While having a mix of credit is beneficial, avoid opening new accounts unless necessary. Multiple new accounts can lower the average age of your credit history and impact your score.

- Regularly review your credit report: Check your credit report for errors or inaccuracies and dispute any information that is incorrect. Reporting agencies are required to investigate and correct errors within a certain timeframe.

- Limit credit inquiries: Too many credit inquiries, especially within a short period, can negatively affect your credit score. Only apply for credit when necessary and be strategic about your applications.

- Establish a credit history: If you are new to credit, consider starting with a secured credit card or becoming an authorized user on someone else’s credit card. Building a positive credit history takes time, so it’s important to start early.

- Don’t close old accounts: Closing old accounts can shorten your credit history. If you have a long-standing account with a positive payment history, consider keeping it open, even if you don’t use it frequently.

- Manage different types of credit: Having a diverse mix of credit, such as credit cards, loans, and mortgages, can positively impact your credit score. However, only take on credit that you can manage responsibly.

- Practice patience and consistency: Improving your credit score takes time and consistent effort. Stay committed to positive financial habits, and you’ll see gradual improvements in your creditworthiness.

It’s important to note that there is no quick fix for improving your credit score. It requires responsible financial behavior and consistent efforts over time. Be cautious of credit repair companies that promise instant improvements, as they often engage in unethical practices.

By implementing these strategies and developing good financial habits, you can gradually improve your credit score and enhance your overall financial well-being.

Common Misconceptions About Credit Scores

Credit scores can be complex, and there are several misconceptions surrounding them. It’s crucial to separate fact from fiction to make informed decisions about your financial health. Here are some common misconceptions about credit scores:

- Closing a credit card will immediately improve your credit score: Closing a credit card can actually have a negative impact on your credit score. It can decrease your available credit and shorten your credit history, both of which are factors considered in credit scoring models.

- Checking your own credit score will harm your credit: When you check your own credit score, it is considered a soft inquiry and does not impact your credit score. It’s important to regularly monitor your credit for accuracy and potential fraud.

- Poor credit scores are permanent: Your credit score is not set in stone. It can improve over time as you demonstrate positive financial behavior, such as making timely payments and reducing debt. Consistency and patience are key when working towards a better credit score.

- Having no credit history means a perfect credit score: While not having a credit history may result in a “thin file,” it does not automatically mean a perfect credit score. Lenders prefer to see a track record of responsible credit management before extending credit, so building a positive credit history is essential.

- Closing accounts with a delinquent payment removes it from your credit report: Closing an account with a delinquent payment does not remove it from your credit report. The payment history, both positive and negative, will remain on your report for a specified period, typically seven years, according to credit reporting regulations.

- Paying off all debt will guarantee an excellent credit score: While paying off debt is beneficial, it may not guarantee an excellent credit score. Other factors, such as credit utilization and credit history length, also play a role. It’s important to maintain responsible credit habits even after paying off debt.

Understanding these misconceptions can help you make better financial decisions and navigate the world of credit scores more effectively. It’s always a good idea to consult reputable sources, such as financial advisors or credit counseling services, for accurate information and guidance.

Remember, knowledge is power when it comes to managing your credit score. By dispelling these misconceptions, you can make informed decisions and work towards building and maintaining a healthy credit profile.

Conclusion

Understanding and managing your credit score is essential for your financial well-being. Your credit score impacts various aspects of your financial life, from accessing credit to securing favorable loan terms and even influencing insurance premiums and housing opportunities. By familiarizing yourself with the factors that affect your credit score and taking proactive steps to improve it, you can enhance your financial standing and open up more opportunities.

Remember that building a good credit score takes time and consistent effort. It requires responsible financial behavior, such as making timely payments, keeping debt levels in check, and managing a diverse mix of credit. Regularly monitoring your credit score and reviewing your credit report for errors or discrepancies is also crucial to maintaining a healthy credit profile.

Additionally, it’s important to debunk common misconceptions surrounding credit scores. Understanding the truth behind these misconceptions can help you make informed decisions and avoid taking actions that may harm your creditworthiness unintentionally.

By implementing the strategies outlined in this article, you can take control of your credit score and improve your financial future. Whether you’re starting from scratch or working on rebuilding your credit, remember that every positive financial choice you make contributes to your overall creditworthiness. So stay informed, be proactive, and watch your credit score rise as you navigate the world of personal finance.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance