Home>Finance>Beacon Credit Score: Definition, Vs. FICO Score & Pinnacle Score

Finance

Beacon Credit Score: Definition, Vs. FICO Score & Pinnacle Score

Published: October 14, 2023

Learn more about beacon credit score, its difference from FICO score and pinnacle score, and how it impacts your financial status. Improve your finance with a better understanding of credit scores.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Beacon Credit Score: Definition, vs. FICO Score & Pinnacle Score

When it comes to managing your finances, understanding your credit score is crucial. It can determine your ability to get approved for loans, rent an apartment, or even land that dream job. While you may be familiar with the widely recognized FICO score, you may not be aware of another scoring system called the Beacon credit score. In this blog post, we will demystify the Beacon credit score and explore how it compares to the FICO score and the lesser-known Pinnacle score.

Key Takeaways:

- The Beacon credit score is a credit scoring system developed by Equifax.

- The FICO score is the most commonly used credit scoring system by lenders.

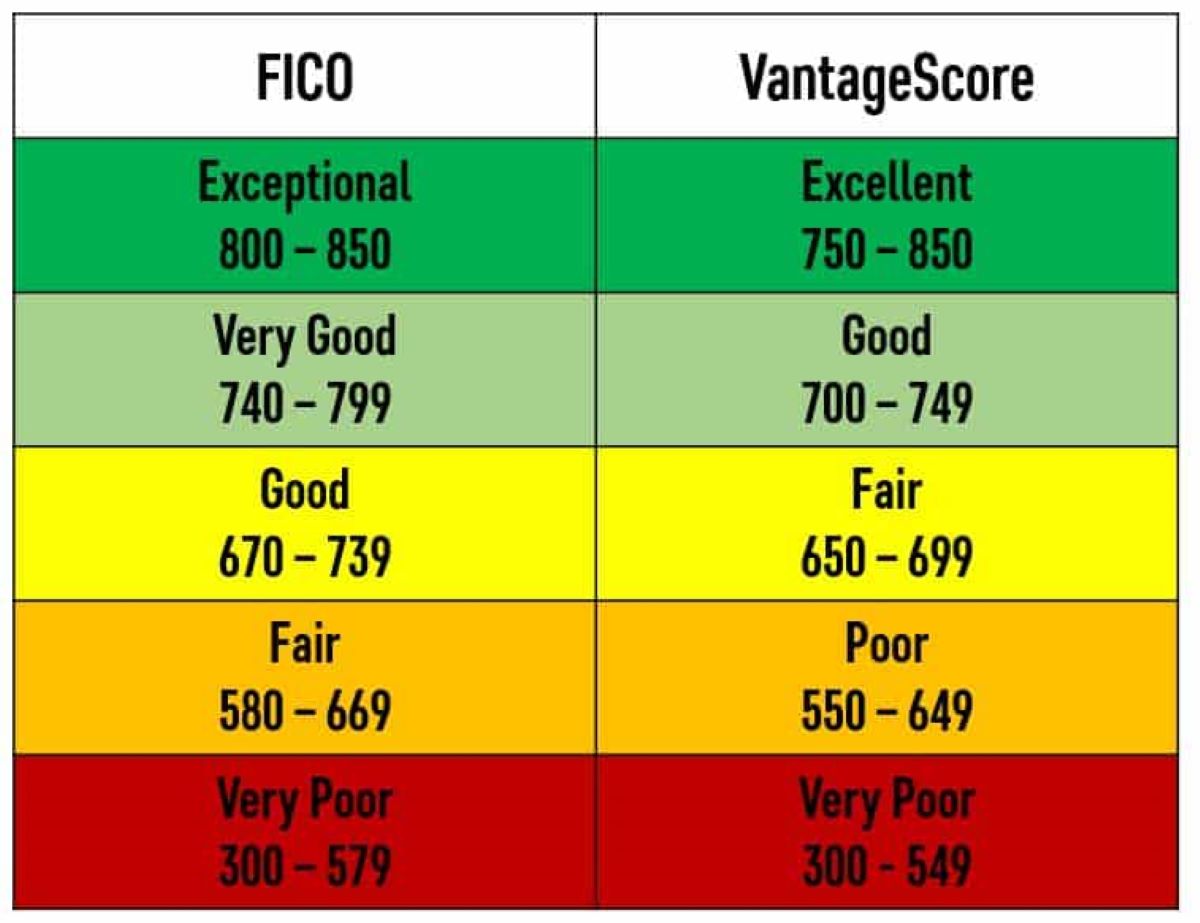

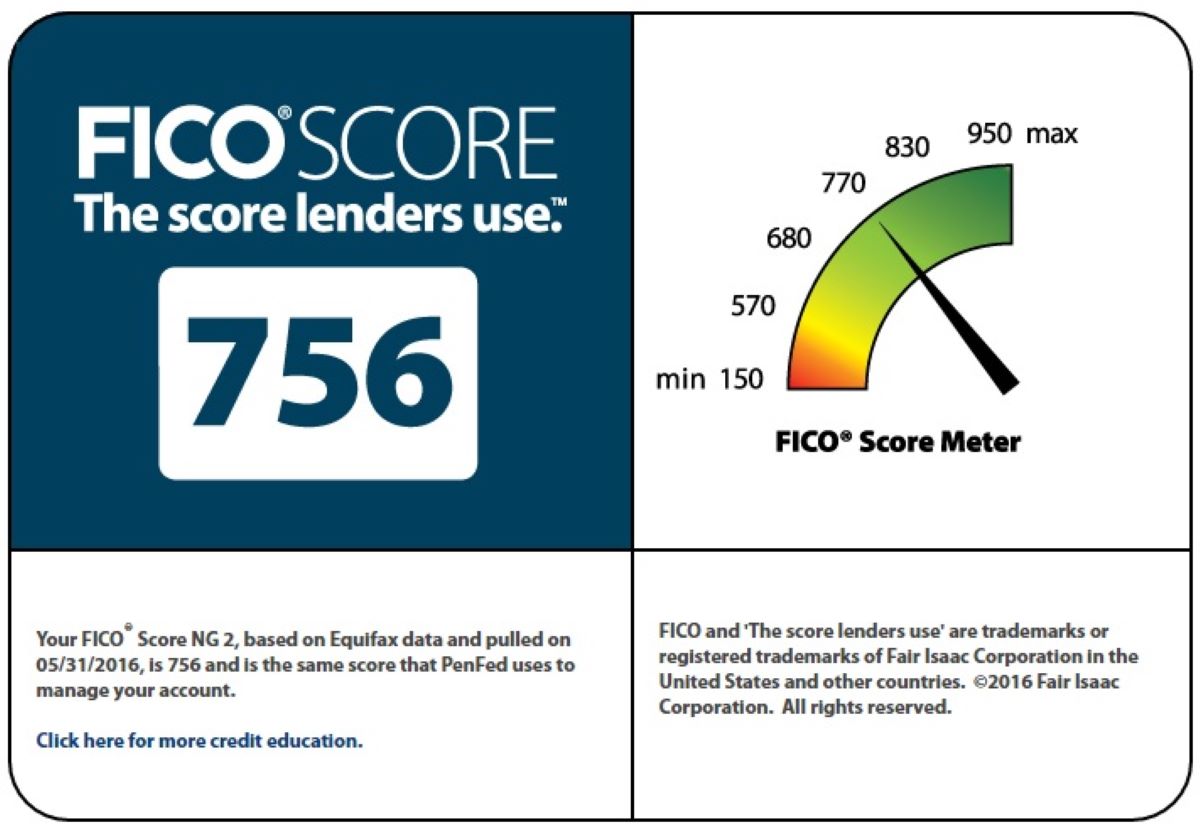

Let’s start by unraveling the mystery of the Beacon credit score. Developed by Equifax, one of the three major credit bureaus, the Beacon credit score is a numerical representation of an individual’s creditworthiness. It takes into account various factors, including payment history, credit utilization, length of credit history, and new credit inquiries. Like the FICO score, the Beacon credit score ranges from 300 to 850, with a higher score indicating better creditworthiness.

Now, let’s compare the Beacon credit score with the FICO score, which is widely used by lenders:

Beacon Credit Score vs. FICO Score:

Both the Beacon credit score and the FICO score serve the same purpose of evaluating creditworthiness, but they use slightly different algorithms and weightings to calculate scores. Here are some key differences:

- Data Sources: The FICO score is calculated using data from all three major credit bureaus – Equifax, Experian, and TransUnion. In contrast, the Beacon credit score is based solely on Equifax data.

- Algorithm: The specific algorithm used to calculate the Beacon credit score is not publicly available. On the other hand, the FICO score’s algorithm is widely known and has undergone several revisions over the years.

- Weightings: Both scores take into account factors such as payment history, credit utilization, and length of credit history. However, the weightings assigned to these factors may differ between the two scoring models. For example, the Beacon score may place more emphasis on certain factors compared to the FICO score.

It’s important to note that while the Beacon credit score is used by some lenders, the FICO score remains the most commonly used scoring model. When you apply for a loan or credit card, it’s more likely that the lender will review your FICO score to determine your creditworthiness.

Pinnacle Score:

Now that we’ve covered the Beacon credit score and its comparison to the FICO score, let’s briefly touch on the Pinnacle score. The Pinnacle score is yet another credit scoring system developed by TransUnion, one of the major credit bureaus. Although less well-known than the Beacon and FICO scores, the Pinnacle score uses similar factors to evaluate creditworthiness.

Ultimately, understanding your credit score is essential for managing your finances effectively. Whether it’s the Beacon credit score, FICO score, or Pinnacle score, knowing where you stand can help you make informed financial decisions and work towards improving your creditworthiness.

Now that you’re equipped with knowledge about the Beacon credit score, how it compares to the FICO score, and a glimpse into the Pinnacle score, you can confidently navigate the world of credit scoring. Remember, building and maintaining good credit takes time and responsible financial habits. Stay on top of your credit by regularly monitoring your credit scores and reports.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance