Finance

When Can A Life Insurance Trust Be Created?

Modified: December 29, 2023

Learn about the creation of a life insurance trust in the world of finance. Discover when it is beneficial to establish this type of trust and protect your assets.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Life Insurance Trusts

- Legal Requirements for Creating a Life Insurance Trust

- Factors to Consider Before Creating a Life Insurance Trust

- Situations When a Life Insurance Trust Can Be Created

- Benefits and Advantages of Establishing a Life Insurance Trust

- Potential Drawbacks and Challenges of Life Insurance Trusts

- How to Create a Life Insurance Trust

- Seeking Professional Advice for Setting Up a Life Insurance Trust

- Conclusion

Introduction

Life insurance can provide financial security and peace of mind for your loved ones in the event of your passing. However, if not properly managed, the proceeds from a life insurance policy can be subject to estate taxes, potentially diminishing the intended benefits for your beneficiaries. That’s where a life insurance trust can play a crucial role.

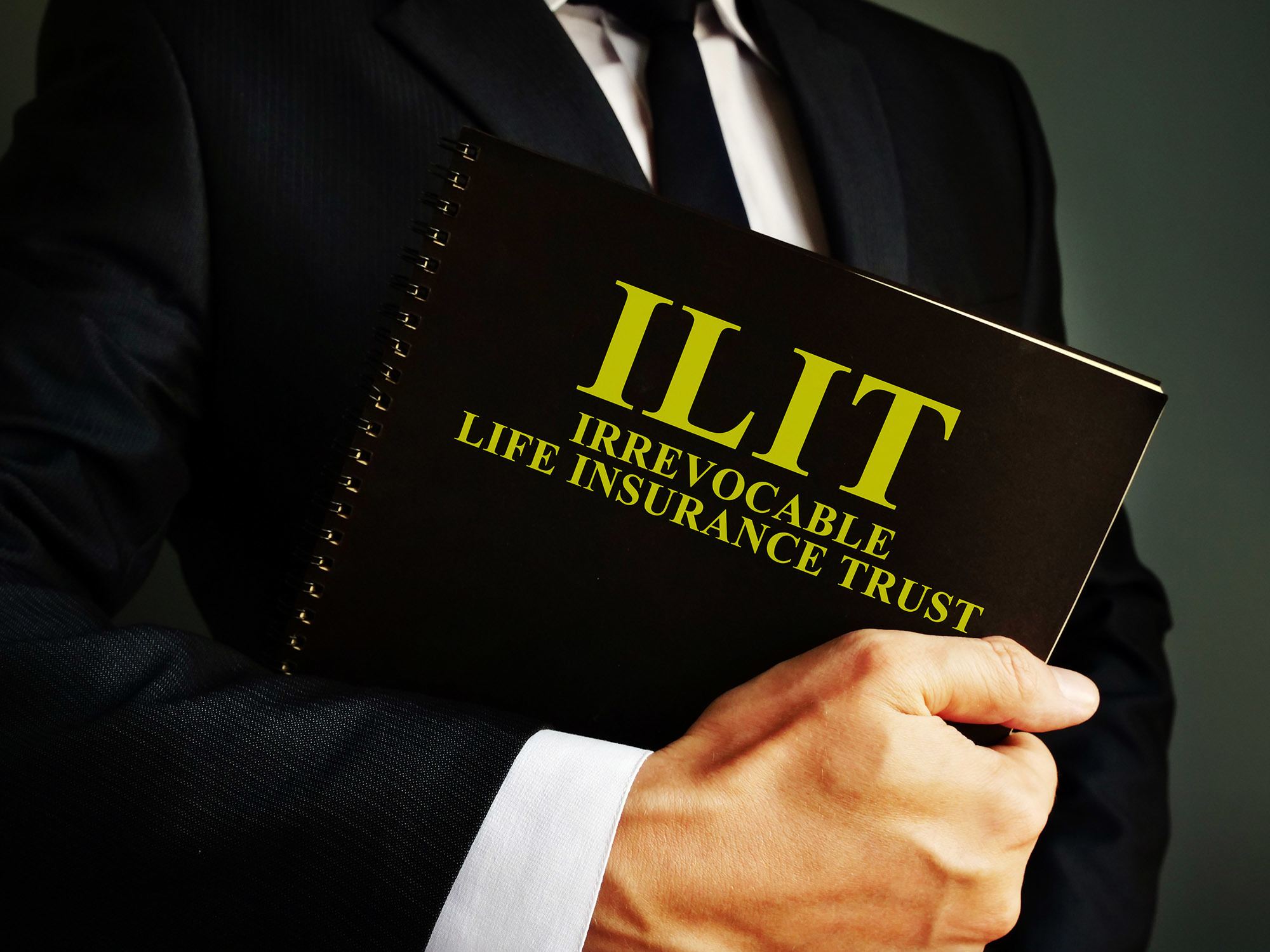

A life insurance trust, also known as an irrevocable life insurance trust (ILIT), is a legal arrangement that can help minimize estate taxes and provide control over the distribution of life insurance proceeds. It allows you to remove the life insurance policy from your estate, reducing the estate tax liability and ensuring that the funds are distributed according to your wishes.

In this article, we will delve into the intricacies of life insurance trusts, exploring their legal requirements, benefits, and potential challenges. Additionally, we will discuss when it is appropriate to create a life insurance trust and offer guidance on how to establish one. Whether you are an individual looking to protect your assets or a financial planner seeking to advise clients on estate planning strategies, this article will provide valuable insights.

Before delving into the specifics, it is important to note that life insurance trusts can be complex and involve legal and tax considerations. It is highly recommended to consult with a qualified estate planning attorney or financial advisor who specializes in estate planning and trusts. They will ensure that the trust is set up correctly and aligned with your individual circumstances and goals.

Now, let’s dive deeper into the world of life insurance trusts and explore the various aspects that make them an invaluable tool in estate planning.

Understanding Life Insurance Trusts

A life insurance trust is a legal entity that is specifically designed to own a life insurance policy on the life of the insured individual. By placing the policy within the trust, the policy proceeds are kept separate from the insured’s estate. This separation helps to minimize estate taxes and allows for greater control over the distribution of the funds.

One of the key features of a life insurance trust is its irrevocable nature. Once the trust is created and funded, it cannot be altered or revoked by the insured. This provides added protection against potential changes in circumstances or the insured’s wishes.

The trustee, who is typically an individual or a corporate entity, manages the trust and ensures that the terms of the trust agreement are followed. The trust agreement outlines how the life insurance proceeds will be distributed to the beneficiaries, who can be individuals, charities, or other organizations.

It is important to note that the trust must be the owner and beneficiary of the life insurance policy for it to be effective. This means that the trust, rather than the insured or their estate, will receive the proceeds upon the insured’s death. By doing so, the policy proceeds are not considered part of the insured’s taxable estate.

A life insurance trust offers several advantages, including:

- Estate tax savings: Placing the life insurance policy within the trust removes it from the insured’s estate, potentially reducing estate taxes. This can be particularly beneficial for individuals with large estates that may be subject to estate tax liabilities.

- Control over distribution: Through the trust agreement, the insured can dictate how the life insurance proceeds will be distributed among the beneficiaries. This allows for a more structured and controlled allocation of funds.

- Protection against creditors: Since the trust is separate from the insured’s estate, the life insurance proceeds are generally protected from creditors. This can be advantageous in safeguarding the intended benefits for the beneficiaries.

- Privacy: By using a life insurance trust, the distribution of proceeds is kept private, as the trust does not go through probate. This can help avoid public scrutiny and to maintain the confidentiality of the estate plan.

Legal Requirements for Creating a Life Insurance Trust

Creating a life insurance trust involves adhering to specific legal requirements to ensure its validity and effectiveness. While the exact legal requirements may vary depending on the jurisdiction, here are some common elements to consider:

1. Drafting the Trust Agreement: The first step in creating a life insurance trust is to draft a trust agreement. This document outlines the terms and conditions of the trust, including the trustee’s responsibilities, the beneficiaries, and the distribution of the life insurance proceeds. It is essential to work with a qualified estate planning attorney to ensure that the trust agreement complies with the relevant laws and meets your specific needs.

2. Funding the Trust: To establish a life insurance trust, the policy owner must transfer ownership of the life insurance policy to the trust. This transfer requires executing an assignment of the policy, which legally transfers ownership to the trust. The trust then becomes the policy owner and beneficiary, ensuring that the insurance proceeds are separate from the insured’s estate.

3. Irrevocability: To achieve the desired tax benefits and asset protection, a life insurance trust must be irrevocable. This means that once the trust is created, it cannot be amended or revoked by the insured, ensuring that the policy proceeds remain outside of the taxable estate.

4. Crummey Powers: To make contributions to the life insurance trust, often in the form of premiums payments, the trust may include provisions for Crummey powers. Crummey powers allow the beneficiaries to withdraw the gifted funds within a specified timeframe, usually 30 days. This withdrawal right ensures that the contributions qualify for the annual gift tax exclusion.

5. Compliance with Gift Tax Rules: Contributions to a life insurance trust are considered gifts. It is crucial to comply with gift tax rules and regulations, including filing any necessary gift tax returns if the contributions exceed the annual gift tax exclusion amount. Consulting with a tax professional or estate planning attorney can help ensure compliance with these rules.

6. Trustee Selection: The trust must have a trustee who will manage the trust assets and oversee the distribution of the life insurance proceeds according to the terms of the trust agreement. The trustee should be someone trustworthy and capable of fulfilling their fiduciary duties. Consideration should be given to selecting a successor trustee in case the initial trustee is unable or unwilling to continue in their role.

7. Compliance with State Laws: It is essential to adhere to the specific laws and regulations governing life insurance trusts in your jurisdiction. State laws may vary on certain aspects, such as trustee requirements, trust administration, and tax implications. Working with a knowledgeable attorney will help ensure compliance with these laws.

Remember, the creation of a life insurance trust is a legally binding process. It is crucial to consult with an experienced estate planning attorney who can guide you through the legal requirements and ensure that the trust is properly established and aligned with your individual circumstances and goals.

Factors to Consider Before Creating a Life Insurance Trust

While a life insurance trust can offer significant benefits, it is essential to carefully consider several factors before deciding to create one. Here are some key considerations to keep in mind:

1. Estate Planning Goals: Assess your estate planning goals and determine if a life insurance trust aligns with your objectives. If minimizing estate taxes, ensuring privacy, and controlling the distribution of life insurance proceeds are important to you, then a life insurance trust may be an appropriate strategy.

2. Financial Situation and Policy Ownership: Evaluate your financial situation and the ownership structure of the life insurance policy. If the policy is already held by an irrevocable trust, creating a separate life insurance trust may not be necessary. However, if the policy is individually owned, establishing a dedicated trust can provide additional benefits.

3. Tax Implications: Understand the tax implications associated with a life insurance trust. While the trust can help minimize estate taxes, it may have implications on gift taxes and income taxes. Working with a tax professional or estate planning attorney will help you navigate these complexities and ensure proper tax planning.

4. Cash Flow for Premium Payments: Consider your ability to fund the life insurance trust. Premium payments must be made to keep the policy in force. Ensure that you have a reliable source of income or assets that can be dedicated to premium payments, as these expenses can impact your overall financial plan.

5. Impact on Eligibility for Government Benefits: If you or your beneficiaries rely on government benefits such as Medicaid or Supplemental Security Income (SSI), creating a life insurance trust may affect eligibility. It is crucial to understand the impact on eligibility and consider alternative planning strategies if needed.

6. Flexibility and Control: Evaluate your desired level of control and flexibility over the life insurance policy and its proceeds. Keep in mind that once the life insurance policy is placed in an irrevocable trust, you generally surrender control over the policy. However, the trust agreement can provide specific instructions on how the proceeds should be distributed among your beneficiaries.

7. Professional Guidance: Seeking guidance from a qualified estate planning attorney or financial advisor is crucial. They can assess your individual circumstances, provide personalized recommendations, and ensure that the life insurance trust aligns with your overall estate plan.

Considering these factors will help you make an informed decision about whether creating a life insurance trust is the right choice for your specific situation. It is important to remember that estate planning is a complex process, and professional guidance is invaluable in navigating the legal, financial, and tax implications of establishing a life insurance trust.

Situations When a Life Insurance Trust Can Be Created

A life insurance trust can be beneficial in a variety of situations. Here are some scenarios where creating a life insurance trust may be appropriate:

1. High Net Worth Individuals: High net worth individuals who have substantial assets that may be subject to estate taxes can use a life insurance trust as part of their estate plan. Placing life insurance policies within the trust can help minimize estate taxes and preserve more wealth for future generations.

2. Business Owners and Professionals: Business owners and professionals who have significant financial obligations, such as business debts, professional liabilities, or potential lawsuits, may utilize a life insurance trust to protect the life insurance proceeds from potential creditors. By placing the policy within the trust, the funds can be shielded from these potential claims.

3. Blended Families: Individuals in blended families may want to ensure that their children from a previous marriage receive their intended share of the life insurance proceeds. A life insurance trust can provide a way to allocate the funds specifically to those beneficiaries, regardless of any subsequent changes to the insured’s circumstances or relationships.

4. Providing for Special Needs Individuals: If you have a dependent with special needs who relies on government benefits, directing life insurance proceeds to a special needs trust within a life insurance trust can help protect the beneficiary’s eligibility for those benefits. Special needs trusts are designed to supplement, rather than replace, government assistance while still providing for the beneficiary’s needs.

5. Charitable Giving: Those who wish to leave a charitable legacy can establish a life insurance trust to benefit their preferred charities. By naming the charity as a beneficiary, the life insurance trust can provide a substantial donation to the charity upon the insured’s passing, without affecting the taxable estate.

6. Business Succession Planning: Business owners can use a life insurance trust as part of their succession planning strategy. The trust can ensure that there is enough liquidity to fund the buyout of a deceased owner’s interests, protecting the smooth transition of the business to the remaining owners or family members.

7. Estate Equalization: In situations where certain heirs are receiving significant assets, such as a family business or real estate, a life insurance trust can help equalize the distribution of wealth among beneficiaries. The trust can provide life insurance proceeds specifically to those beneficiaries who would otherwise receive a smaller share of the estate.

These are just a few examples of situations where a life insurance trust can be instrumental in achieving specific estate planning goals. It is important to evaluate your individual circumstances and consult with a qualified professional to determine if a life insurance trust is appropriate for your specific needs.

Benefits and Advantages of Establishing a Life Insurance Trust

Creating a life insurance trust can offer various benefits and advantages in estate planning. Here are some key advantages of establishing a life insurance trust:

1. Minimizing Estate Taxes: One of the primary benefits of a life insurance trust is its ability to help minimize estate taxes. By transferring the life insurance policy to the trust, the proceeds are no longer considered part of your taxable estate. This can be particularly beneficial for individuals with sizable estates that exceed the estate tax exemption threshold.

2. Control over Distribution: With a life insurance trust, you have greater control over how and when the insurance proceeds are distributed. The trust agreement can provide specific instructions on who will receive the funds, in what amounts, and under what conditions. This allows you to ensure that the proceeds are distributed according to your wishes and can be especially useful in situations where you want to provide for dependents or protect beneficiaries from misusing the funds.

3. Protecting Assets from Creditors: Placing a life insurance policy within a trust can protect its proceeds from potential creditors. The trust is a separate legal entity, and as such, the insurance proceeds are generally shielded from the claims of creditors. This can be especially valuable if you have significant liabilities or are involved in a profession with potential lawsuits or legal disputes.

4. Privacy and Avoidance of Probate: Assets held in a life insurance trust are typically not subject to the probate process. This means that the distribution of the life insurance proceeds can be kept private, avoiding the public scrutiny that often accompanies probate proceedings. This can be beneficial if you value privacy or if you want to maintain confidentiality and avoid any potential challenges to the estate plan.

5. Providing for Special Needs Individuals: A life insurance trust can be a valuable tool for individuals who have dependents with special needs. By setting up a special needs trust within the life insurance trust, you can ensure that the beneficiary with special needs continues to qualify for government benefits while still receiving financial support from the life insurance proceeds.

6. Equalizing Inheritance: In situations where you want to ensure an equal distribution of assets among beneficiaries, a life insurance trust can help balance inheritances. For example, if you have a significant non-liquid asset that you want to leave to one beneficiary, you can use a life insurance trust to provide an equal value to other beneficiaries, essentially equalizing the overall inheritance.

7. Continuity of Business: If you are a business owner, a life insurance trust can help with continuity planning. By providing a source of funds to buy out a deceased owner’s interest, the trust ensures that the business can continue without financial disruption, benefiting both the remaining owners and the deceased owner’s family.

These benefits highlight the advantages of establishing a life insurance trust as part of an effective estate plan. However, it is crucial to consult with an experienced estate planning attorney or financial advisor who can guide you through the process and tailor the trust to your specific needs and goals.

Potential Drawbacks and Challenges of Life Insurance Trusts

While life insurance trusts offer numerous benefits, it is important to be aware of some potential drawbacks and challenges associated with their establishment and management. Understanding these potential pitfalls will help you make an informed decision and take appropriate steps to mitigate any challenges. Here are some key considerations:

1. Loss of Control: Once a life insurance policy is placed within a trust, the insured generally relinquishes control over the policy. The trustee becomes responsible for managing the trust and distributing the proceeds according to the trust agreement. This loss of control may be a concern for some individuals who prefer to have more flexibility and discretion over the distribution of their assets.

2. Irrevocability: A life insurance trust is typically irrevocable, meaning that it cannot be changed or terminated without the consent of the beneficiaries or a court order. This lack of flexibility can pose challenges if there are significant changes in your circumstances, family dynamics, or goals in the future. It is essential to carefully consider the long-term implications and seek professional advice before establishing an irrevocable trust.

3. Premium Payments: Funding a life insurance trust requires regular premium payments to keep the policy in force. These payments may pose financial challenges if your circumstances change, or if unforeseen financial burdens arise. Failing to make premium payments could result in the policy lapsing, potentially jeopardizing the intended benefits for the beneficiaries.

4. Tax Considerations: While life insurance trusts can offer tax benefits, they also come with certain tax implications. Contributions to the trust may be subject to gift tax rules, and there may be ongoing income tax considerations. It is essential to work with a tax professional or estate planning attorney to understand these implications and properly plan for any tax obligations associated with the trust.

5. Administrative Burden and Costs: Life insurance trusts require ongoing administration and compliance with legal and tax regulations. Trustees must manage the trust’s assets, file necessary tax returns, and ensure that the trust operates in accordance with the trust agreement. The administrative burden and associated costs can be significant and may require engaging professionals such as trustees, attorneys, and accountants to assist with trust administration.

6. Impact on Government Benefits: If a beneficiary receiving government benefits, such as Medicaid or Supplemental Security Income (SSI), is named in the life insurance trust, it could impact their eligibility for those benefits. It is crucial to navigate the restrictions and requirements of government assistance programs to ensure that the trust’s proceeds do not jeopardize the beneficiary’s eligibility for vital support.

7. Complexity and Professional Guidance: Establishing and managing a life insurance trust can be complex, involving legal, financial, and tax considerations. It is vital to work with qualified professionals experienced in estate planning to ensure that the trust is structured correctly, complies with relevant laws, and aligns with your specific goals and circumstances.

Considering these potential drawbacks and challenges can help you make an informed decision about whether a life insurance trust is suitable for your particular situation. It is crucial to carefully evaluate the benefits and disadvantages in consultation with professional advisors to ensure that the trust aligns with your overall estate planning objectives.

How to Create a Life Insurance Trust

Creating a life insurance trust involves several key steps to ensure its proper establishment and compliance with legal requirements. Here is a general overview of the process:

1. Determine Your Goals and Objectives: Begin by clarifying your estate planning goals and objectives. Understand why you want to create a life insurance trust and what specific benefits you hope to achieve through its establishment. Outline your desired distribution of assets, consider potential tax implications, and identify any specific provisions or instructions you want to include in the trust agreement.

2. Consult with Professionals: Seek guidance from qualified professionals who specialize in estate planning and trust administration. Engage an experienced estate planning attorney who can provide personalized advice based on your unique circumstances. Additionally, consider working with a financial advisor and a tax professional to ensure that the trust aligns with your financial goals and minimizes any tax implications.

3. Draft the Trust Agreement: With the help of your attorney, draft the trust agreement. This legally binding document outlines the terms and conditions of the trust, including the trustee’s duties, the beneficiaries, and the distribution of the life insurance proceeds. Ensure the trust agreement is clear, comprehensive, and tailored to your specific intentions.

4. Select a Trustee: Choose a trustee who will be responsible for managing the life insurance trust. The trustee should be someone you trust, preferably with experience in trust administration, fiduciary responsibilities, and financial management. Consider a backup or successor trustee in case the initial trustee is unable or unwilling to carry out their duties.

5. Fund the Trust: Transfer ownership of the life insurance policy to the trust by executing an assignment of the policy. This legal document transfers ownership from you to the trust, making the trust the policy owner and beneficiary. Consult with your insurance company and follow their guidelines to ensure a smooth transfer of ownership.

6. Communicate with Beneficiaries: Inform your intended beneficiaries about the existence of the life insurance trust and their status as beneficiaries. Explain their rights, distribution plans, and any other relevant details. Open and transparent communication can help prevent misunderstandings and ensure smoother trust administration in the future.

7. Maintain the Trust: Once the life insurance trust is established, it requires ongoing maintenance. Regularly review the trust agreement to ensure that it reflects your current wishes and make any necessary updates. Keep track of premium payments and ensure that the policy remains adequately funded to provide the intended benefits to your beneficiaries.

8. Seek Professional Assistance: Throughout the process of creating and managing a life insurance trust, it is essential to engage professionals for guidance and support. Consult with an attorney, financial advisor, and tax professional to ensure compliance with legal and tax requirements and to properly administer the trust over time.

Remember, establishing a life insurance trust is a complex legal process. Working with experienced professionals will help ensure that the trust is set up correctly, meets your specific goals, and provides the intended benefits to your loved ones.

Seeking Professional Advice for Setting Up a Life Insurance Trust

Creating a life insurance trust is a significant undertaking, laden with legal and financial complexities. Seeking professional advice is crucial to ensure that the trust is established properly and aligned with your specific needs and goals. Here are the key reasons why you should seek professional assistance when setting up a life insurance trust:

Expertise and Knowledge: Estate planning attorneys and financial advisors specializing in trusts have a deep understanding of the legal, financial, and tax implications associated with life insurance trusts. They are equipped with the knowledge and expertise to navigate these complexities, ensuring that the trust is structured correctly and complies with all relevant laws and regulations.

Individualized Approach: Professionals can provide personalized advice tailored to your unique circumstances. They will carefully assess your financial situation, estate planning goals, and family dynamics to recommend the most suitable options for your specific needs. This individualized approach ensures that the life insurance trust is aligned with your intentions and provides the intended benefits to your beneficiaries.

Tax Planning: Establishing a life insurance trust involves tax considerations, including potential gift tax implications, estate tax planning, and income tax concerns. Professionals well-versed in tax law can help you navigate these complexities and develop strategic tax planning strategies to minimize tax obligations and maximize the benefits of the trust.

Asset Protection: Professionals can advise on the best approach to protect your assets within the life insurance trust. They can help structure the trust to shield the life insurance proceeds from potential creditors, ensuring that the funds are preserved for the intended beneficiaries and not exposed to legal claims or liabilities.

Compliance and Documentation: Establishing a life insurance trust requires meticulous attention to detail and adherence to legal requirements. Professionals will ensure that the necessary legal documents, such as the trust agreement and policy assignments, are properly drafted and executed. They will also assist with filing any required tax returns, providing peace of mind that all legal and compliance aspects are taken care of.

Ongoing Trust Administration: Professionals can assist with the ongoing administration of the life insurance trust. They can help oversee premium payments, ensure compliance with trust terms, and facilitate proper distribution of the life insurance proceeds to beneficiaries. Their involvement provides expertise and guidance throughout the life of the trust.

Avoiding Costly Mistakes: Mistakes made during the creation of a life insurance trust can have significant financial and legal consequences. Working with professionals mitigates the risk of errors and oversights that could undermine the effectiveness or validity of the trust. They have the experience to anticipate potential pitfalls and proactively address them, saving you time, money, and potential legal troubles.

A life insurance trust is a powerful estate planning tool, but its establishment requires careful consideration and professional guidance. Engaging qualified estate planning attorneys, financial advisors, and tax professionals will ensure that you make informed decisions, maximize the benefits of the trust, and protect the interests of your loved ones.

Conclusion

Creating a life insurance trust can provide invaluable benefits and protections in the realm of estate planning. By establishing this legal entity, individuals can minimize estate taxes, maintain control over the distribution of life insurance proceeds, protect assets from creditors, and ensure privacy in their estate plans. Life insurance trusts are particularly advantageous for high net worth individuals, business owners, those with blended families, individuals with special needs dependents, and those seeking to leave charitable legacies. However, it is important to recognize potential drawbacks, such as loss of control, irrevocability, premium payment obligations, tax considerations, administrative burdens, and impacts on government benefits.

To successfully create a life insurance trust, individuals should engage qualified professionals with expertise in estate planning, trust administration, tax planning, and financial management. These professionals have a deep understanding of the legal and financial complexities surrounding life insurance trusts and can provide personalized guidance tailored to individual circumstances. Seeking their assistance ensures proper trust structuring, tax planning, compliance with legal requirements, and ongoing administration.

Ultimately, the decision to establish a life insurance trust should be based on careful consideration of personal goals, financial situations, and estate planning objectives. By availing professional expertise, individuals can navigate the intricacies of life insurance trusts and achieve long-term financial security and peace of mind for themselves and their loved ones.

In conclusion, a well-structured and appropriately managed life insurance trust is a powerful tool that empowers individuals to protect their assets, minimize taxes, control asset distribution, and achieve their estate planning goals. With professional guidance and a thorough understanding of the advantages, disadvantages, and legal requirements associated with life insurance trusts, individuals can make informed decisions that have the potential to shape their financial legacies for generations to come.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance