Home>Finance>Why Is Personal Finance Dependent Upon Your Behavior?

Finance

Why Is Personal Finance Dependent Upon Your Behavior?

Published: January 22, 2024

Discover the crucial link between personal finance and behavior. Learn how your financial decisions impact your financial well-being. Explore effective strategies to manage your finances.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Personal finance is not just about numbers; it's about behavior. The way individuals manage their money, make financial decisions, and plan for the future is heavily influenced by their behavior and mindset. This interplay between personal behavior and financial outcomes forms the foundation of personal finance psychology. Understanding the psychological aspects of personal finance is crucial for achieving financial well-being and stability.

When we talk about personal finance, we often focus on budgeting, investing, and saving, but we tend to overlook the behavioral and psychological factors that underpin these actions. However, delving into the realm of personal finance psychology reveals the significance of emotions, habits, and cognitive biases in shaping financial behaviors and outcomes.

In this article, we will explore the intricate relationship between personal behavior and finance, shedding light on the psychological underpinnings that drive financial decisions. By understanding the psychology of personal finance, individuals can gain insight into their own financial behaviors, identify areas for improvement, and implement strategies to enhance their financial well-being. Let's delve into the fascinating world of personal finance psychology and discover why our behaviors play a pivotal role in shaping our financial reality.

The Psychology of Personal Finance

At its core, personal finance is deeply intertwined with human psychology. Our attitudes, beliefs, and emotions regarding money significantly impact our financial decisions and behaviors. The psychology of personal finance encompasses a wide array of factors, including our relationship with money, our financial goals, our decision-making processes, and our responses to financial success and setbacks.

One of the fundamental aspects of personal finance psychology is our money mindset. This encompasses our beliefs and attitudes towards money, which are often shaped by our upbringing, experiences, and societal influences. Whether one views money as a source of security, freedom, or stress can greatly influence their financial behaviors, such as spending habits, saving tendencies, and risk tolerance.

Moreover, our financial goals and aspirations are deeply rooted in our psychological makeup. The pursuit of financial security, wealth accumulation, or material possessions is often driven by underlying psychological needs and desires. Understanding the psychological drivers behind our financial goals can provide valuable insights into our motivations and help align our behaviors with our aspirations.

Furthermore, the decision-making processes involved in personal finance are heavily influenced by cognitive biases, emotions, and heuristics. Behavioral economics, a field that integrates insights from psychology and economics, has unveiled a myriad of cognitive biases that affect our financial choices, such as loss aversion, overconfidence, and present bias. Recognizing these biases and understanding how they shape our decision-making can empower individuals to make more rational and informed financial choices.

In essence, the psychology of personal finance delves into the intricate interplay between human behavior and financial outcomes. By unraveling the psychological underpinnings of our financial behaviors, individuals can gain a deeper understanding of their relationship with money and leverage this awareness to make positive changes in their financial lives.

Behavioral Economics and Personal Finance

Behavioral economics, a branch of economics that incorporates insights from psychology to understand economic decision-making, has significantly influenced the field of personal finance. Traditional economic models assume that individuals make rational decisions based on maximizing their utility, but behavioral economics challenges this notion by highlighting the systematic biases and irrational tendencies that shape human behavior, especially in the realm of finance.

One of the key principles of behavioral economics is bounded rationality, which suggests that individuals make decisions based on limited cognitive resources and often rely on heuristics and mental shortcuts. This concept is particularly relevant in personal finance, where individuals are faced with complex and multifaceted decisions regarding spending, saving, investing, and borrowing.

Moreover, behavioral economics has unearthed numerous cognitive biases that influence financial behaviors. For instance, the endowment effect leads individuals to overvalue what they already possess, impacting their willingness to sell or part with assets. Similarly, the framing effect demonstrates how the presentation of information can significantly alter decision-making, influencing choices related to investments, insurance, and other financial products.

Furthermore, behavioral economics sheds light on the phenomenon of present bias, wherein individuals disproportionately prioritize immediate rewards over long-term benefits. This bias has profound implications for saving and retirement planning, as individuals may struggle to forgo immediate consumption in favor of building long-term financial security.

By integrating insights from behavioral economics, personal finance practitioners and advisors can design strategies and interventions that account for individuals’ behavioral tendencies and cognitive limitations. From nudging individuals towards better saving habits to simplifying investment choices to mitigate decision fatigue, behavioral economics offers practical tools for improving financial decision-making and outcomes.

Understanding the principles of behavioral economics is pivotal for individuals seeking to navigate the complexities of personal finance. By acknowledging the influence of behavioral biases and heuristics, individuals can adopt strategies that align with their cognitive tendencies, ultimately fostering more prudent and effective financial behaviors.

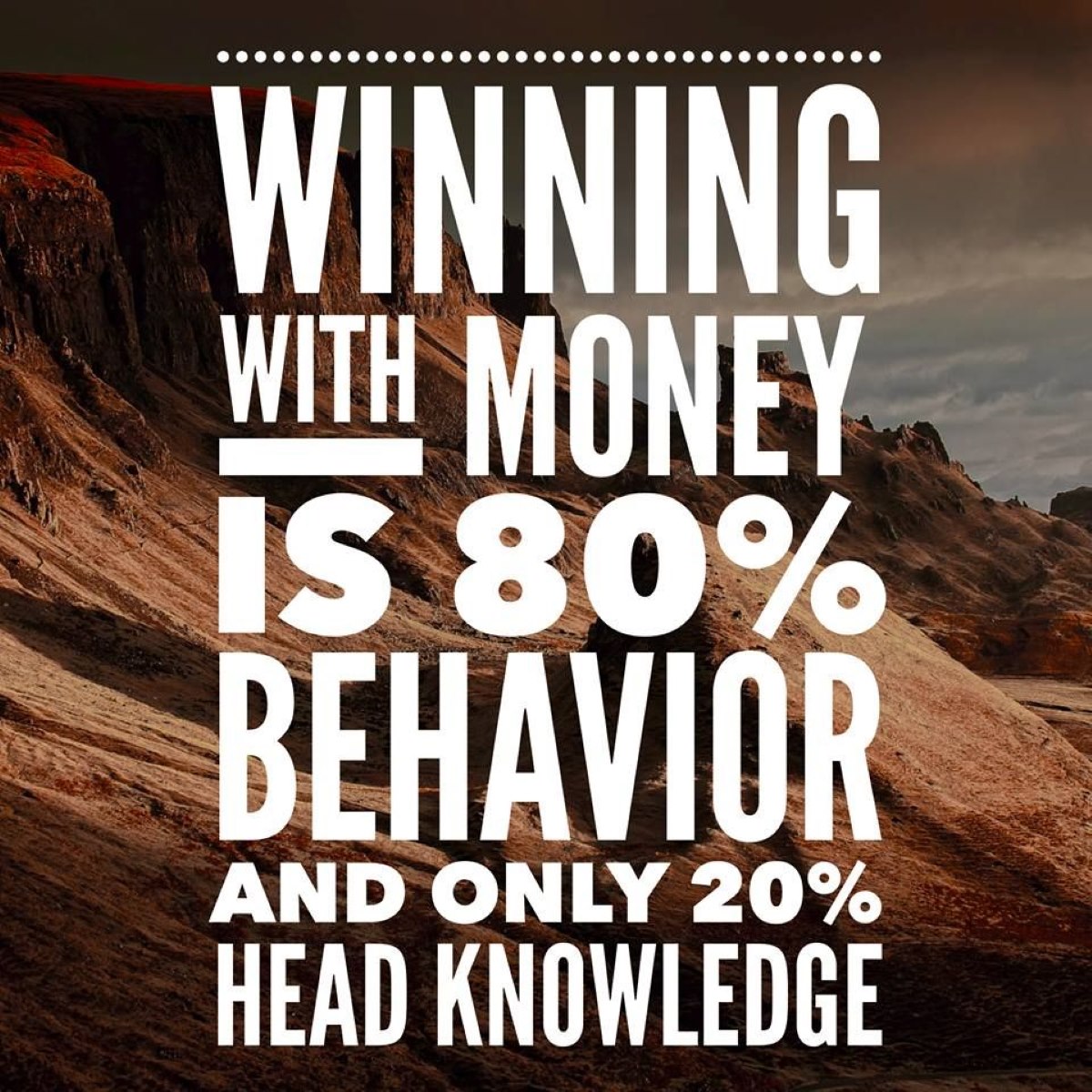

The Impact of Behavior on Financial Decision-Making

Behavior plays a pivotal role in shaping financial decision-making, influencing everything from spending habits to investment choices and long-term financial planning. The intricate interplay between human behavior and financial decisions often leads to outcomes that deviate from traditional economic models, underscoring the need to understand and address behavioral influences in personal finance.

One of the primary areas where behavior exerts a profound impact is in the realm of spending and consumption. Personal preferences, lifestyle choices, and emotional triggers significantly influence individuals’ spending habits, often leading to impulse purchases, lifestyle inflation, and excessive debt accumulation. Moreover, the pervasive influence of consumer culture and social comparison further shapes spending behaviors, driving individuals to make financial decisions influenced by social norms and status symbols.

When it comes to investment decisions, behavioral biases and emotions can heavily influence individuals’ choices, often leading to suboptimal outcomes. The fear of missing out (FOMO) may drive individuals to chase investment trends without conducting thorough research, while the aversion to losses can lead to a reluctance to sell underperforming assets, resulting in portfolio imbalances. Additionally, overconfidence in one’s investment acumen can prompt excessive trading and risk-taking, potentially undermining long-term financial goals.

Long-term financial planning is also profoundly impacted by behavior, particularly in the context of saving for retirement and managing financial risks. Procrastination, a prevalent behavioral tendency, can hinder individuals from initiating retirement savings early, leading to inadequate preparedness for the future. Moreover, individuals’ risk perceptions and aversion to uncertainty can influence their approach to financial risk management, impacting decisions related to insurance coverage, asset allocation, and estate planning.

Recognizing the pervasive influence of behavior on financial decision-making is essential for individuals and financial professionals alike. By acknowledging the psychological underpinnings that drive financial choices, individuals can proactively address behavioral biases, cultivate prudent financial habits, and seek guidance that accounts for behavioral influences in personal finance. Moreover, integrating behavioral insights into financial education and advisory services can empower individuals to make more informed and rational financial decisions, ultimately enhancing their financial well-being.

Strategies for Improving Financial Behavior

Improving financial behavior entails leveraging insights from behavioral economics and psychology to cultivate prudent money management habits and make informed financial decisions. By implementing targeted strategies, individuals can mitigate the impact of behavioral biases and enhance their financial well-being.

1. Financial Education and Awareness: Enhancing financial literacy and fostering awareness of behavioral biases are crucial steps in improving financial behavior. Educating individuals about common cognitive biases, such as loss aversion and herd mentality, can empower them to recognize and counteract these influences in their financial decision-making.

2. Goal Setting and Planning: Setting clear, achievable financial goals and formulating a comprehensive plan to attain them can mitigate impulsive decision-making and promote disciplined financial behavior. By aligning short-term actions with long-term objectives, individuals can cultivate a forward-looking approach to money management.

3. Automation and Behavioral Prompts: Leveraging automation for savings, investments, and bill payments can circumvent the impact of procrastination and present bias. Additionally, employing behavioral prompts, such as setting reminders for financial reviews and goal tracking, can reinforce prudent financial behaviors.

4. Mindful Spending and Budgeting: Practicing mindful spending involves being conscious of purchasing decisions, evaluating needs versus wants, and adhering to a well-defined budget. By incorporating mindfulness into spending habits, individuals can curb impulsive purchases and prioritize expenditures aligned with their financial goals.

5. Seeking Professional Guidance: Engaging with financial advisors who understand the nuances of behavioral finance can provide valuable insights and tailored strategies to address individual behavioral tendencies. Professional guidance can help individuals navigate complex financial decisions while accounting for their behavioral biases and emotional triggers.

6. Behavioral Nudges and Incentives: Implementing behavioral nudges, such as default enrollment in retirement savings plans and opt-out mechanisms for excessive spending, can steer individuals towards favorable financial behaviors. Furthermore, incentivizing positive financial actions, such as matching contributions for savings, can motivate individuals to adopt prudent money management practices.

By employing these strategies and integrating behavioral insights into their financial approach, individuals can cultivate resilient and disciplined financial behaviors, ultimately fostering greater financial stability and well-being.

Conclusion

Personal finance is undeniably intertwined with human behavior, emotions, and cognitive biases. The intricate interplay between psychology and finance shapes individuals’ financial decisions, influencing their spending habits, investment choices, and long-term financial planning. By delving into the realm of personal finance psychology and behavioral economics, individuals can gain a deeper understanding of their financial behaviors and motivations, paving the way for improved financial well-being.

Recognizing the profound impact of behavior on financial decision-making is pivotal for individuals seeking to navigate the complexities of personal finance. By acknowledging the psychological underpinnings that drive financial choices, individuals can proactively address behavioral biases, cultivate prudent financial habits, and seek guidance that accounts for behavioral influences in personal finance.

Moreover, integrating insights from behavioral economics and psychology into financial education and advisory services can empower individuals to make more informed and rational financial decisions. By enhancing financial literacy, setting clear goals, leveraging automation, and seeking professional guidance, individuals can mitigate the impact of behavioral biases and cultivate resilient and disciplined financial behaviors.

Ultimately, by implementing targeted strategies and embracing a mindful approach to money management, individuals can align their financial behaviors with their long-term aspirations, fostering greater financial stability and well-being. Understanding the psychology of personal finance equips individuals with the tools to navigate the complexities of financial decision-making, empowering them to make prudent choices that resonate with their values and goals.

As individuals strive to enhance their financial behavior, the integration of behavioral insights and practical strategies can pave the way for a more mindful and purposeful approach to personal finance, ultimately fostering greater financial resilience and well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance