Home>Finance>What Percentage Of Personal Finance Is Behavior?

Finance

What Percentage Of Personal Finance Is Behavior?

Published: January 22, 2024

Learn how behavior influences personal finance and discover the percentage of impact it has on financial decisions. Explore the psychology behind financial choices. Improve your financial habits today.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding the Impact of Behavior on Personal Finance

Personal finance is not just about numbers and calculations; it is deeply intertwined with human behavior. The way individuals manage their money, make financial decisions, and plan for the future is significantly influenced by their behaviors and attitudes towards money. Understanding the behavioral aspects of personal finance is crucial for achieving financial well-being and stability. This article delves into the intricate relationship between personal finance and behavior, shedding light on the pivotal role that behavior plays in shaping financial outcomes.

Behavioral economics, a field that combines insights from psychology and economics, has increasingly emphasized the significance of behavior in personal finance. Traditional financial theories often assume rational decision-making, but in reality, human behavior is far more complex and can deviate from rationality. This departure from rationality can have profound implications for financial choices, savings patterns, investment decisions, and overall financial success.

As we explore the impact of behavior on personal finance, it becomes evident that financial decisions are not solely based on objective analysis but are heavily influenced by emotions, cognitive biases, and social factors. By delving into the behavioral aspects of personal finance, individuals can gain a deeper understanding of their financial habits and tendencies, paving the way for informed and mindful financial management.

Understanding the intricate interplay between behavior and personal finance is essential for individuals seeking to enhance their financial well-being and make sound financial decisions. By recognizing the profound influence of behavior on financial outcomes, individuals can adopt strategies to improve their financial behaviors, ultimately leading to greater financial stability and long-term prosperity.

Understanding Personal Finance Behavior

Personal finance behavior encompasses the attitudes, habits, and decision-making processes that individuals exhibit in managing their financial resources. It delves into the psychological and behavioral aspects that underpin financial choices, spending patterns, saving behaviors, and investment decisions. Understanding personal finance behavior involves examining the cognitive, emotional, and social factors that influence how individuals interact with money and make financial decisions.

One crucial aspect of understanding personal finance behavior is recognizing the role of emotions in financial decision-making. Emotions such as fear, greed, and overconfidence can significantly impact financial choices, leading individuals to make impulsive decisions or deviate from their long-term financial goals. Additionally, behavioral biases, such as loss aversion and mental accounting, can influence how individuals perceive and respond to financial gains and losses, shaping their overall financial behavior.

Moreover, personal finance behavior is shaped by individual attitudes towards risk and uncertainty. Some individuals may exhibit a high tolerance for risk, leading them to pursue aggressive investment strategies, while others may be more risk-averse, preferring conservative financial approaches. Understanding these risk preferences is essential for tailoring financial plans and investment portfolios to align with individuals’ comfort levels and long-term objectives.

Furthermore, the social and environmental influences on personal finance behavior cannot be overlooked. Peer pressure, societal norms, and cultural factors can impact how individuals manage their finances, leading to varying spending habits and saving behaviors across different demographic groups. Additionally, the accessibility of financial education and resources can shape individuals’ financial behaviors, highlighting the importance of promoting financial literacy and providing equitable access to financial knowledge.

By comprehensively understanding personal finance behavior, individuals can gain insights into their financial strengths and areas for improvement. This understanding serves as a foundation for implementing effective strategies to enhance financial decision-making, cultivate healthy financial habits, and work towards long-term financial security.

The Role of Behavior in Personal Finance

The role of behavior in personal finance is multifaceted and profound, influencing every aspect of an individual’s financial journey. Behavioral economics has elucidated the significant impact of human behavior on financial decision-making, highlighting the complexities and nuances that underlie individuals’ financial choices and actions.

One pivotal role of behavior in personal finance is its influence on spending habits and consumption patterns. Individuals’ attitudes towards money, their propensity to indulge in discretionary spending, and their ability to resist impulsive purchases are all shaped by their behavioral inclinations. Understanding and addressing these behavioral drivers is crucial for promoting responsible spending and fostering a sustainable approach to managing financial resources.

Moreover, behavior plays a crucial role in savings and investment behaviors. The propensity to save, the willingness to delay gratification for long-term goals, and the inclination towards risk-taking in investment decisions are all underpinned by behavioral factors. Behavioral biases, such as present bias and overconfidence, can hinder individuals from making optimal savings and investment choices, emphasizing the need to recognize and mitigate these biases for improved financial outcomes.

Behavior also influences individuals’ approach to financial planning and goal setting. Procrastination, self-control issues, and the framing of financial objectives can all impact the effectiveness of financial planning efforts. By understanding the behavioral barriers to effective planning, individuals can adopt strategies to overcome these hurdles and establish robust financial plans that align with their aspirations and values.

Furthermore, behavior shapes individuals’ responses to financial setbacks and market fluctuations. Emotional reactions to financial losses, the tendency to engage in herding behavior during market volatility, and the impact of cognitive biases on investment decisions all underscore the profound role of behavior in navigating financial challenges and uncertainties.

Recognizing the multifaceted role of behavior in personal finance is instrumental in empowering individuals to make informed financial decisions, cultivate healthy financial habits, and build resilient financial futures. By integrating behavioral insights into financial planning and decision-making processes, individuals can harness the power of behavior to optimize their financial well-being and achieve their long-term financial goals.

Factors Affecting Personal Finance Behavior

The behavior exhibited in personal finance is influenced by a myriad of factors that encompass psychological, social, and environmental dimensions. Understanding these factors is essential for comprehending the complexities of financial decision-making and developing targeted strategies to improve financial behaviors.

Psychological factors play a pivotal role in shaping personal finance behavior. Cognitive biases, such as anchoring, confirmation bias, and availability heuristic, can lead individuals to make suboptimal financial decisions, impacting their savings, investment, and spending behaviors. Emotional factors, including fear, euphoria, and anxiety, can also sway financial choices, influencing risk tolerance levels and investment strategies. Moreover, individual personality traits, such as conscientiousness and impulsivity, can significantly impact financial behaviors, underscoring the importance of recognizing and addressing these psychological drivers of financial decision-making.

Social influences exert a profound impact on personal finance behavior. Peer pressure, social norms, and cultural values all shape individuals’ attitudes towards money, spending habits, and savings behaviors. Family dynamics and upbringing can also influence individuals’ financial behaviors, as early exposure to financial management practices and parental attitudes towards money can leave lasting imprints on individuals’ financial habits and behaviors. Additionally, societal trends and media influence can impact consumer behavior and financial decision-making, highlighting the interconnectedness of social factors with personal finance behavior.

Environmental factors, such as access to financial resources, educational opportunities, and economic conditions, can significantly affect personal finance behavior. Individuals’ financial behaviors are influenced by their level of financial literacy, the availability of financial planning services, and the overall economic climate. Moreover, technological advancements and the digitalization of financial services have transformed the landscape of personal finance behavior, shaping individuals’ preferences for financial management tools and platforms.

By recognizing the diverse array of factors that influence personal finance behavior, individuals can gain insights into the multifaceted nature of financial decision-making. Addressing these factors through targeted interventions, financial education, and behavioral nudges can empower individuals to overcome barriers to sound financial behaviors, fostering a culture of financial well-being and resilience.

The Importance of Behavior in Personal Finance

The significance of behavior in personal finance cannot be overstated, as it serves as a fundamental determinant of individuals’ financial well-being and success. Recognizing the importance of behavior in personal finance is essential for fostering informed decision-making, promoting healthy financial habits, and achieving long-term financial security.

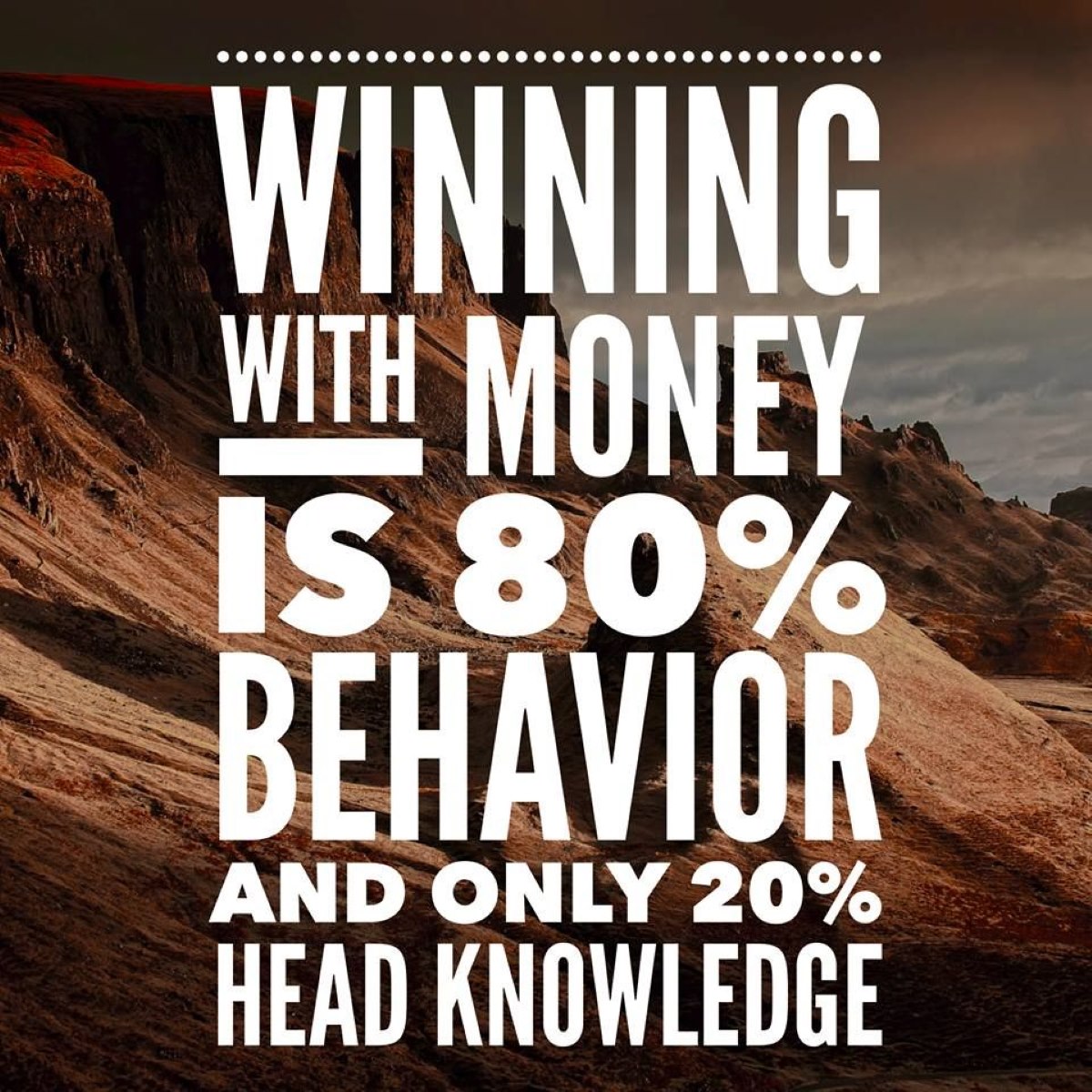

Behavioral patterns profoundly impact individuals’ financial outcomes, often overshadowing the purely numerical aspects of financial management. While traditional financial theories emphasize rational decision-making based on objective analysis, the reality of human behavior introduces complexities that can significantly influence financial choices, savings behaviors, and investment strategies. Understanding the behavioral underpinnings of personal finance is crucial for mitigating the impact of cognitive biases, emotional responses, and social influences on financial decision-making.

Moreover, the importance of behavior in personal finance extends to the realm of financial goal attainment and long-term planning. Behavioral barriers, such as procrastination, present bias, and self-control issues, can impede individuals from effectively planning for their financial futures and achieving their desired objectives. By acknowledging and addressing these behavioral hurdles, individuals can cultivate disciplined financial practices and align their behaviors with their long-term aspirations.

Behavioral finance research has underscored the role of behavior in influencing investment outcomes and market participation. Emotional reactions to market fluctuations, herding behavior during periods of volatility, and the impact of cognitive biases on investment decisions all highlight the profound influence of behavior on investment success. By integrating behavioral insights into investment strategies, individuals can make more informed and rational investment decisions, enhancing their overall investment performance.

Furthermore, the importance of behavior in personal finance extends to the realm of financial well-being and resilience. By cultivating healthy financial behaviors, individuals can build robust financial foundations, mitigate the impact of financial setbacks, and navigate economic uncertainties with greater confidence. The adoption of prudent financial behaviors, such as consistent saving habits, diversified investment approaches, and disciplined spending practices, fosters financial resilience and long-term prosperity.

Recognizing and harnessing the importance of behavior in personal finance empowers individuals to make conscious and deliberate financial choices, aligning their behaviors with their overarching financial goals. By integrating behavioral insights into financial planning, decision-making processes, and investment strategies, individuals can optimize their financial well-being and pave the way for enduring financial success.

Strategies for Improving Personal Finance Behavior

Improving personal finance behavior entails adopting targeted strategies that address the psychological, social, and environmental factors influencing financial decision-making. By implementing proactive measures to enhance financial behaviors, individuals can cultivate healthy financial habits and work towards achieving their long-term financial objectives.

One effective strategy for improving personal finance behavior is to prioritize financial education and awareness. By enhancing financial literacy and knowledge, individuals can gain a deeper understanding of financial concepts, investment principles, and risk management strategies. Access to comprehensive financial education equips individuals with the tools to make informed financial decisions, fostering responsible financial behaviors and empowering individuals to navigate the complexities of the financial landscape.

Behavioral nudges, such as setting up automated savings plans and investment contributions, can serve as powerful tools for improving personal finance behavior. By leveraging behavioral economics principles, individuals can design their financial environments to facilitate prudent financial behaviors. Automatic savings deductions, for instance, encourage consistent saving habits, while automated investment contributions promote disciplined and systematic wealth accumulation.

Setting clear and achievable financial goals is integral to improving personal finance behavior. By establishing specific, measurable, and time-bound financial objectives, individuals can align their behaviors with their desired outcomes. Goal setting provides a roadmap for financial planning and decision-making, guiding individuals towards prudent spending, saving, and investment behaviors that support their overarching financial aspirations.

Behavioral coaching and guidance can also play a pivotal role in improving personal finance behavior. Professional financial advisors and coaches can assist individuals in identifying and addressing behavioral barriers that hinder sound financial decision-making. Through personalized guidance, individuals can gain insights into their financial behaviors, develop strategies for overcoming behavioral biases, and cultivate disciplined financial practices.

- Cultivating mindfulness and self-awareness concerning financial behaviors

- Setting up automatic savings and investment contributions

- Seeking professional financial coaching and guidance

- Utilizing behavioral economics principles to design conducive financial environments

- Engaging in ongoing financial education and knowledge enhancement

- Adopting technology-driven financial management tools and resources

- Participating in peer support groups and financial communities to foster accountability and shared learning

By integrating these strategies into their financial journeys, individuals can proactively enhance their personal finance behavior, cultivate healthy financial habits, and work towards achieving enduring financial well-being and resilience.

Conclusion

Personal finance behavior serves as a cornerstone of individuals’ financial journeys, shaping their financial decisions, habits, and long-term outcomes. Understanding the profound impact of behavior on personal finance is essential for fostering informed decision-making, promoting healthy financial habits, and achieving enduring financial well-being.

As individuals navigate the intricacies of personal finance, they must recognize the multifaceted nature of behavior and its influence on financial outcomes. Psychological, social, and environmental factors intertwine to shape individuals’ financial behaviors, underscoring the complexities inherent in financial decision-making. By acknowledging these influences, individuals can gain insights into their financial behaviors, recognize behavioral biases, and implement strategies to improve their financial decision-making processes.

The integration of behavioral insights into financial planning and decision-making processes empowers individuals to make conscious and deliberate financial choices, aligning their behaviors with their overarching financial goals. Strategies such as financial education, behavioral nudges, goal setting, and professional guidance offer pathways for individuals to enhance their personal finance behavior, cultivate disciplined financial habits, and work towards achieving their long-term financial objectives.

Ultimately, the recognition of behavior as a pivotal determinant of financial well-being underscores the importance of addressing behavioral barriers and fostering a culture of mindful financial management. By embracing behavioral insights, individuals can optimize their financial decision-making, mitigate the impact of cognitive biases, and cultivate resilient financial behaviors that pave the way for enduring financial success.

As individuals embark on their financial journeys, the integration of behavioral principles and targeted strategies for improving personal finance behavior can serve as a catalyst for building robust financial foundations, fostering financial resilience, and working towards a future of financial security and prosperity.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance