Finance

How Are Credit Unions Insured

Modified: January 15, 2024

Discover how credit unions are insured and protected in the finance industry. Find out what measures are in place to safeguard your financial investments.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- The National Credit Union Administration (NCUA)

- The National Credit Union Share Insurance Fund (NCUSIF)

- How Credit Union Deposits are Insured

- Coverage Limits for Credit Union Deposits

- Exclusions and Limitations of Insurance Coverage

- Additional Protections for Credit Union Members

- Understanding the Risks and Benefits of Credit Union Membership

- Conclusion

Introduction

When it comes to managing your finances, ensuring the safety and security of your deposits is a top priority. This is especially true when dealing with credit unions, as individuals may have questions regarding how their money is protected.

Credit unions are member-owned financial institutions that offer a range of services, including savings accounts, loans, and investment options. Unlike traditional banks, credit unions operate as not-for-profit entities, with a focus on serving their members’ best interests. One of the concerns that individuals often have when considering joining a credit union is how their deposits are insured.

In this article, we will delve into the topic of credit union insurance and explore how credit unions protect their members’ deposits. We will discuss the role of the National Credit Union Administration (NCUA) and the National Credit Union Share Insurance Fund (NCUSIF) in ensuring the safety of credit union accounts. Additionally, we will examine the coverage limits, exclusions, and additional protections that credit union members can enjoy.

The National Credit Union Administration (NCUA)

The National Credit Union Administration (NCUA) is an independent federal agency that regulates and supervises credit unions in the United States. Its primary mission is to ensure the safety and soundness of credit unions and protect the interests of their members.

The NCUA was established in 1970 and operates under the authority of the Federal Credit Union Act. It works to maintain the stability of the credit union system by conducting examinations and audits, providing guidance and support, and enforcing compliance with federal regulations.

One of the key responsibilities of the NCUA is to administer the National Credit Union Share Insurance Fund (NCUSIF), which provides deposit insurance coverage for credit union members. This fund is similar to the Federal Deposit Insurance Corporation (FDIC) that insures deposits in traditional banks.

To ensure the safety of credit union deposits, the NCUA examines credit unions on a regular basis. These examinations assess the financial condition of credit unions, evaluate their risk management practices, and ensure compliance with relevant laws and regulations.

The NCUA also provides resources and assistance to credit union management, offering guidance on issues such as lending practices, liquidity management, and cybersecurity. This support helps credit unions maintain strong financial health and operate in the best interest of their members.

Overall, the NCUA plays a vital role in promoting the stability and integrity of the credit union system. By overseeing the operations of credit unions and administering deposit insurance, the NCUA provides a layer of protection and confidence for credit union members.

The National Credit Union Share Insurance Fund (NCUSIF)

The National Credit Union Share Insurance Fund (NCUSIF) is a federal insurance program that provides deposit insurance coverage for credit unions in the United States. Established by the National Credit Union Administration (NCUA), the NCUSIF plays a critical role in safeguarding the deposits of credit union members.

Similar to the Federal Deposit Insurance Corporation (FDIC) that insures deposits in banks, the NCUSIF provides protection for the funds held in credit unions. This insurance coverage ensures that credit union members’ deposits are safe, even in the event of a credit union failure or insolvency.

The NCUSIF is funded by premiums paid by credit unions based on the total amount of insured shares held by their members. These premiums, along with interest earnings and recoveries from failed credit unions, contribute to the funds available to cover insured deposits.

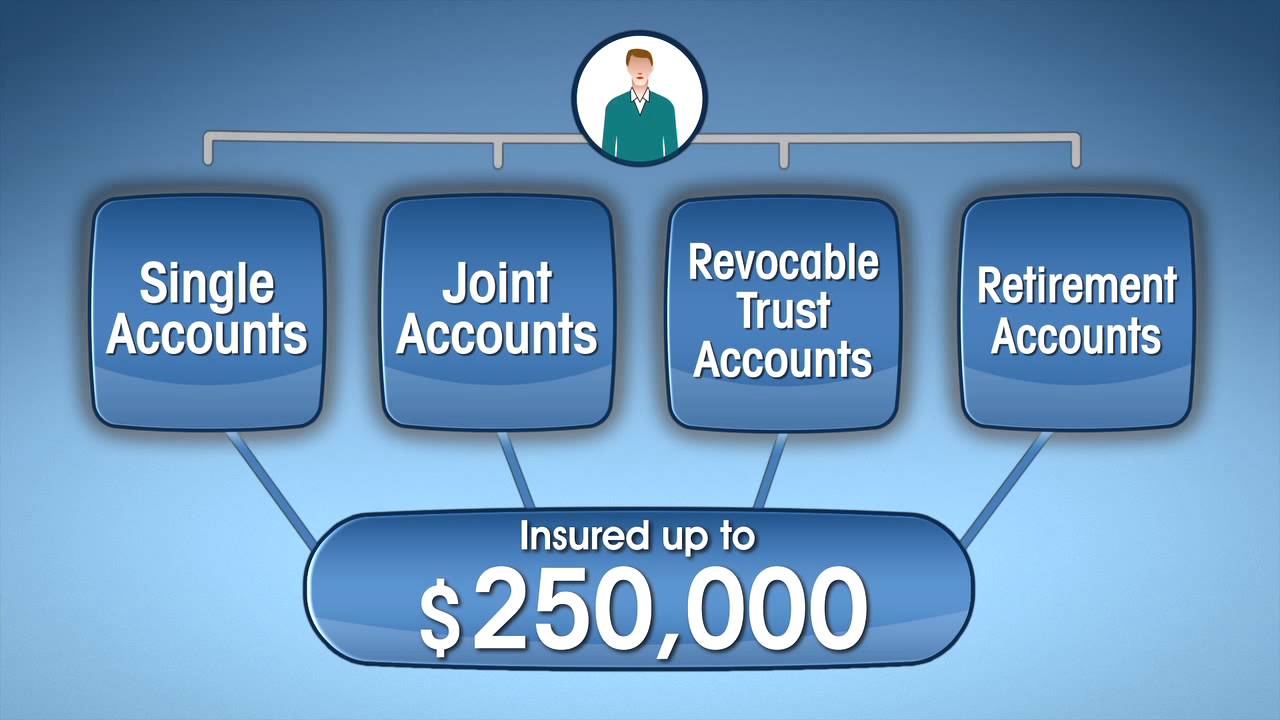

Under the NCUSIF, each individual member’s deposits are insured up to $250,000 per institution. This coverage extends to various types of accounts, including savings accounts, checking accounts, money market accounts, certificates of deposit (CDs), and individual retirement accounts (IRAs).

It’s important to note that the $250,000 insurance coverage limit applies to the combined total of an individual’s deposits in a single credit union. If a person has multiple accounts in the same credit union, such as a savings account and a CD, the total of these deposits must not exceed $250,000 to be fully insured.

Moreover, if a person holds accounts in different credit unions, each credit union is treated separately for insurance purposes. Therefore, deposits in different credit unions are each insured up to $250,000.

The NCUSIF provides a crucial safety net for credit union members, assuring them that their deposits are protected against loss. With the NCUSIF in place, individuals can have peace of mind as they engage in banking activities with credit unions, knowing that their money is secure and insured.

How Credit Union Deposits are Insured

Credit union deposits are insured through the National Credit Union Share Insurance Fund (NCUSIF), which is administered by the National Credit Union Administration (NCUA). This insurance program provides protection for the funds held by credit union members, similar to how the Federal Deposit Insurance Corporation (FDIC) ensures deposits in banks.

Under the NCUSIF, all deposits in participating credit unions are insured up to $250,000 per depositor, per institution. This includes various types of accounts, such as savings accounts, checking accounts, money market accounts, certificates of deposit (CDs), and individual retirement accounts (IRAs).

It’s essential to note that only credit unions that are federally insured by the NCUA offer deposit insurance through the NCUSIF. Members should confirm that their credit union is federally insured by the NCUA to ensure their deposits are protected.

When credit union members deposit money into their accounts, whether through direct deposits, cash deposits, or transfers, those funds become part of the credit union’s assets. The credit union then uses these assets to provide loans and other financial services to its members.

In the unlikely event that a credit union fails or becomes insolvent, the NCUSIF steps in to protect the deposits of its members. In such cases, the NCUSIF will pay out the insured amount to each depositor, up to the $250,000 coverage limit, helping to minimize potential losses for credit union members.

The NCUSIF’s deposit insurance coverage is backed by the full faith and credit of the U.S. government, providing an additional level of confidence and security for credit union members. This ensures that even in times of economic instability or financial uncertainty, credit union deposits remain protected.

It’s important for credit union members to understand that the NCUSIF only insures deposits and does not cover other financial products offered by credit unions, such as investments in securities or mutual funds. These non-deposit investment products are subject to market risks and are not insured by the NCUSIF or any government agency.

By understanding how credit union deposits are insured through the NCUSIF, individuals can have peace of mind, knowing that their hard-earned money is protected and secure within their chosen credit union.

Coverage Limits for Credit Union Deposits

When it comes to the insurance coverage provided by the National Credit Union Share Insurance Fund (NCUSIF), it’s important to understand the coverage limits for credit union deposits. These limits determine the maximum amount that is insured for each depositor in a given credit union.

The standard coverage limit provided by the NCUSIF is $250,000 per depositor, per institution. This means that each individual member’s deposits in a single credit union are insured up to $250,000.

It’s essential to note that the coverage limit applies to the combined total of an individual’s deposits in a single credit union, across various types of accounts. For example, if a person has $150,000 in a savings account and $100,000 in a certificate of deposit (CD) at the same credit union, the total amount of $250,000 would be fully insured.

If an individual has deposits exceeding the $250,000 coverage limit in a single credit union, the excess amount would be uninsured and not protected by the NCUSIF. In such cases, it may be wise to consider spreading deposits across different credit unions to ensure full coverage.

It’s worth noting that joint accounts, where multiple individuals are named as account holders, are insured separately from individual accounts. Each co-owner’s share of the joint account is insured up to the $250,000 limit. For example, a joint account with two co-owners would be insured up to $500,000 ($250,000 for each co-owner).

In addition to individual and joint accounts, certain retirement accounts such as individual retirement accounts (IRAs) are also subject to separate coverage limits. Traditional IRAs, Roth IRAs, and certain other retirement accounts are insured up to $250,000 per depositor, per credit union.

It’s important for credit union members to regularly review their deposits and assess whether they are within the coverage limits. If an individual has deposits in multiple credit unions, each credit union is treated separately for insurance purposes, and the $250,000 coverage limit applies to each institution.

By understanding the coverage limits for credit union deposits, individuals can make informed decisions about their banking arrangements and ensure that their deposits are fully protected by the NCUSIF.

Exclusions and Limitations of Insurance Coverage

While the National Credit Union Share Insurance Fund (NCUSIF) provides important insurance coverage for credit union deposits, it’s crucial to be aware of certain exclusions and limitations that may affect the extent of this coverage.

First and foremost, it’s important to note that the NCUSIF only provides coverage for deposits held in credit unions that are federally insured by the National Credit Union Administration (NCUA). If a credit union is not federally insured, the NCUSIF’s insurance coverage does not apply.

Furthermore, the NCUSIF’s deposit insurance coverage is specifically designed to protect funds held in accounts such as savings accounts, checking accounts, money market accounts, certificates of deposit (CDs), and individual retirement accounts (IRAs).

It’s essential to understand that the NCUSIF does not cover investments in non-deposit products, such as stocks, bonds, mutual funds, annuities, or life insurance policies. These investment products involve market risks and are not insured by the NCUSIF or any government agency.

Additionally, the NCUSIF imposes certain limitations on the amount of insurance coverage provided. The standard coverage limit is $250,000 per depositor, per institution. If an individual or joint account exceeds this limit, the excess amount is not insured and may be at risk in the event of a credit union failure.

It’s important to note that insurance coverage for joint accounts is based on the co-owners’ shares. Each co-owner’s portion of the joint account is insured up to the coverage limit. If the combined deposits of the co-owners exceed the limit, the excess amount is not insured.

Another limitation to consider is that the $250,000 coverage limit applies to an individual member’s deposits in a single credit union. If an individual holds deposits in multiple credit unions, each credit union is treated separately for insurance purposes, and the coverage limit applies to each institution.

Lastly, it’s worth mentioning that the NCUSIF does not protect against losses resulting from fraud, theft, or unauthorized transactions. While credit unions have procedures in place to safeguard against such incidents, it’s important for members to remain vigilant and take necessary precautions to protect their accounts.

By understanding the exclusions and limitations of insurance coverage, credit union members can make informed decisions about their financial arrangements and ensure they have adequate protection for their deposits.

Additional Protections for Credit Union Members

Aside from the National Credit Union Share Insurance Fund (NCUSIF), there are additional protections in place to safeguard the interests of credit union members. These protections are designed to provide peace of mind and ensure the overall integrity and stability of credit unions.

One such protection is the oversight and regulation of credit unions by the National Credit Union Administration (NCUA). The NCUA conducts regular examinations and audits to assess the financial health of credit unions and ensure compliance with applicable laws and regulations. This helps to maintain the safety and soundness of credit unions and protect the interests of their members.

Credit unions also have governance structures that include boards of directors elected by their members. These boards of directors are responsible for overseeing the management and operations of the credit union in the best interest of its members. This democratic structure ensures that members have a say in the decision-making processes of their credit union.

Moreover, credit unions are required to disclose pertinent information to their members, including terms and conditions of accounts, fees, and potential risks associated with their services. This transparency enables members to make informed decisions and stay informed about their financial affairs.

In addition, credit unions adhere to strict privacy policies to protect the personal and financial information of their members. These policies ensure that member data is kept confidential and is not shared with third parties without proper consent. By safeguarding member data, credit unions help prevent identity theft and fraudulent activities.

Credit union membership is generally limited to specific groups such as employees of a certain company, residents of a particular geographic area, or members of a particular organization. This exclusivity fosters a sense of community and allows credit unions to cater to the unique needs of their members. Members can benefit from personalized services and a more personalized banking experience.

Furthermore, credit unions often offer financial counseling and educational resources to their members. These resources aim to improve financial literacy, provide guidance on budgeting, and help members make informed financial decisions. By equipping members with knowledge and skills, credit unions empower individuals to achieve their financial goals.

Lastly, credit unions operate on the principle of “people helping people.” As member-owned institutions, credit unions prioritize the well-being of their members and strive to provide excellent customer service. Members can benefit from a personalized and relationship-based approach, with staff members who are often more accessible and attentive to their individual needs.

By providing additional protections and focusing on member-centric services, credit unions offer a unique and valuable alternative to traditional banking institutions. These protections, along with the deposit insurance provided by the NCUSIF, contribute to a strong and secure banking experience for credit union members.

Understanding the Risks and Benefits of Credit Union Membership

Joining a credit union offers several benefits for individuals looking for a financial institution that prioritizes their members’ interests. However, it’s important to understand the risks and benefits associated with credit union membership before making a decision.

One of the primary advantages of credit union membership is the personalized and member-centric approach to financial services. Credit unions operate as not-for-profit organizations, which means they are driven by the best interests of their members rather than shareholder profits. This often results in lower fees, competitive interest rates, and a more personalized banking experience.

Credit unions are known for their strong sense of community and the ability to serve the unique needs of their members. They often focus on local areas or specific affinity groups, fostering a sense of cohesiveness and shared values. Members can benefit from tailored products and services that address their particular financial goals and situations.

Moreover, credit unions prioritize excellent customer service and accessibility. Members often have direct access to decision-makers and can receive personalized attention from staff members who have a vested interest in their financial well-being. This can lead to a more positive and satisfying banking experience.

However, it’s important to be aware of the potential risks associated with credit union membership. One of the primary risks is the limited number of branches and ATMs compared to larger, national banks. Credit unions may have a smaller physical footprint, which could pose challenges for members who frequently travel or require access to widespread banking networks.

Additionally, credit unions may have more limited product offerings compared to larger banks. While they generally offer essential services such as savings accounts, checking accounts, and loans, their investment options or specialized financial products may be more limited. If an individual requires a wide range of investment options or complex financial products, they may need to explore other financial institutions.

It’s also essential to consider the eligibility requirements for credit union membership. As previously mentioned, credit unions often serve specific groups such as employees of a particular company or residents of a particular geographic area. Individuals who do not meet these eligibility criteria may not be able to join a specific credit union and may need to seek alternative banking options.

Lastly, while credit unions have deposit insurance through the National Credit Union Share Insurance Fund (NCUSIF), it’s important to remember that investment products and non-deposit accounts are not covered by this insurance. Credit union members interested in investing in securities or other non-deposit products may need to explore other avenues for these financial needs.

By understanding the risks and benefits of credit union membership, individuals can make informed decisions about whether it is the right financial institution for their needs. Considering factors such as eligibility requirements, product offerings, and accessibility will help individuals determine if a credit union aligns with their financial goals and preferences.

Conclusion

Joining a credit union provides individuals with a range of benefits, including personalized service, competitive rates, and a strong sense of community. By understanding how credit union deposits are insured through the National Credit Union Share Insurance Fund (NCUSIF), individuals can have confidence in the safety and security of their deposits.

The NCUSIF offers deposit insurance coverage up to $250,000 per depositor, per institution, ensuring that credit union members’ funds are protected even in the event of a credit union failure. This coverage provides peace of mind and reassurance for individuals as they engage in banking activities.

It’s important to be aware of the exclusions and limitations of insurance coverage, such as non-deposit investment products or the $250,000 coverage limit per institution. Understanding these factors helps individuals make informed decisions about their financial arrangements and maximize their deposit insurance coverage.

In addition to deposit insurance, credit union members benefit from the oversight and regulation of the National Credit Union Administration (NCUA), transparent information disclosure, privacy policies, and educational resources. These measures enhance the overall security and integrity of credit unions and further protect the interests of their members.

While credit union membership offers numerous advantages, it’s important to consider the potential limitations, such as limited branch and ATM networks or narrower product offerings. By assessing individual needs and weighing the risks and benefits, individuals can determine if credit union membership aligns with their financial goals and preferences.

In conclusion, credit unions provide a unique and member-centric banking experience, with deposit insurance through the NCUSIF offering an additional layer of protection. By choosing to join a credit union, individuals can enjoy the benefits of personalized service, competitive rates, and a sense of belonging to a community-focused financial institution.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance