Finance

How To Pick A Credit Union

Modified: February 21, 2024

Looking for finance solutions? Learn how to pick the perfect credit union for your financial needs and secure your future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Why Choose a Credit Union

- Researching Credit Union Options

- Membership Eligibility

- Membership Benefits

- Types of Services Offered

- Evaluating Financial Stability

- Fee Structure and Pricing

- Location and Accessibility

- Customer Service and Support

- Online and Mobile Banking Capabilities

- Reviews and Recommendations

- Making Your Decision

- Conclusion

Introduction

Welcome to the world of credit unions! If you’re in the market for financial services, you may have come across the term “credit union” and wondered what it meant. In simple terms, a credit union is a not-for-profit financial institution that provides a wide range of banking services to its members. Unlike traditional banks, which are for-profit institutions owned by shareholders, credit unions are owned and operated by their members.

So why should you consider choosing a credit union for your banking needs? Well, there are several reasons. Firstly, credit unions tend to have a strong focus on customer service and building relationships with their members. They often offer personalized attention and strive to understand the specific financial needs and goals of each individual. Secondly, credit unions typically offer competitive interest rates on loans and savings accounts, as their main goal is to serve their members rather than maximize profits. Lastly, credit unions often have a strong community focus, investing in local initiatives and supporting the neighborhoods they serve.

Now that you understand the basics of what a credit union is and why it might be beneficial, let’s dive into the process of choosing the right credit union for you. With so many options available, it’s important to do your research and consider various factors before making a decision. In the following sections, we will explore key aspects to consider when evaluating credit unions, such as membership eligibility, membership benefits, services offered, financial stability, fee structure, accessibility, customer service, online and mobile banking capabilities, and reviews from other customers.

By the end of this guide, you’ll have a better understanding of how to pick a credit union that aligns with your financial goals and values. So let’s get started!

Why Choose a Credit Union

Choosing a credit union for your banking needs offers a multitude of advantages over traditional banks. Here are some compelling reasons why you might consider joining a credit union:

- Member-focused Approach: Credit unions prioritize the well-being of their members. As not-for-profit organizations, their main objective is to provide affordable financial services and support the financial goals of their members, rather than maximizing profits.

- Competitive Interest Rates: Credit unions often provide more favorable interest rates on loans and savings accounts compared to traditional banks. This means you can potentially save money on interest payments or earn higher returns on your savings.

- Personalized Service: Credit unions are known for their personalized approach and commitment to building strong relationships with their members. They take the time to understand your unique financial situation and offer tailored solutions to help you achieve your goals.

- Community Involvement: Credit unions are deeply rooted in their local communities. They invest in local initiatives, sponsor events, and support community development projects. By banking with a credit union, you contribute to the well-being of your community.

- Shared Ownership: As a credit union member, you have a say in the institution’s decision-making process. You can participate in voting for the board of directors and be actively involved in shaping the future of the credit union.

- Lower Fees: Credit unions typically have lower fees compared to traditional banks. They aim to keep costs down and pass the savings on to their members. This can result in substantial savings over time.

- Financial Education: Credit unions often provide financial education resources and workshops to help their members make informed decisions and improve their financial literacy. This can empower you to make smarter choices with your money.

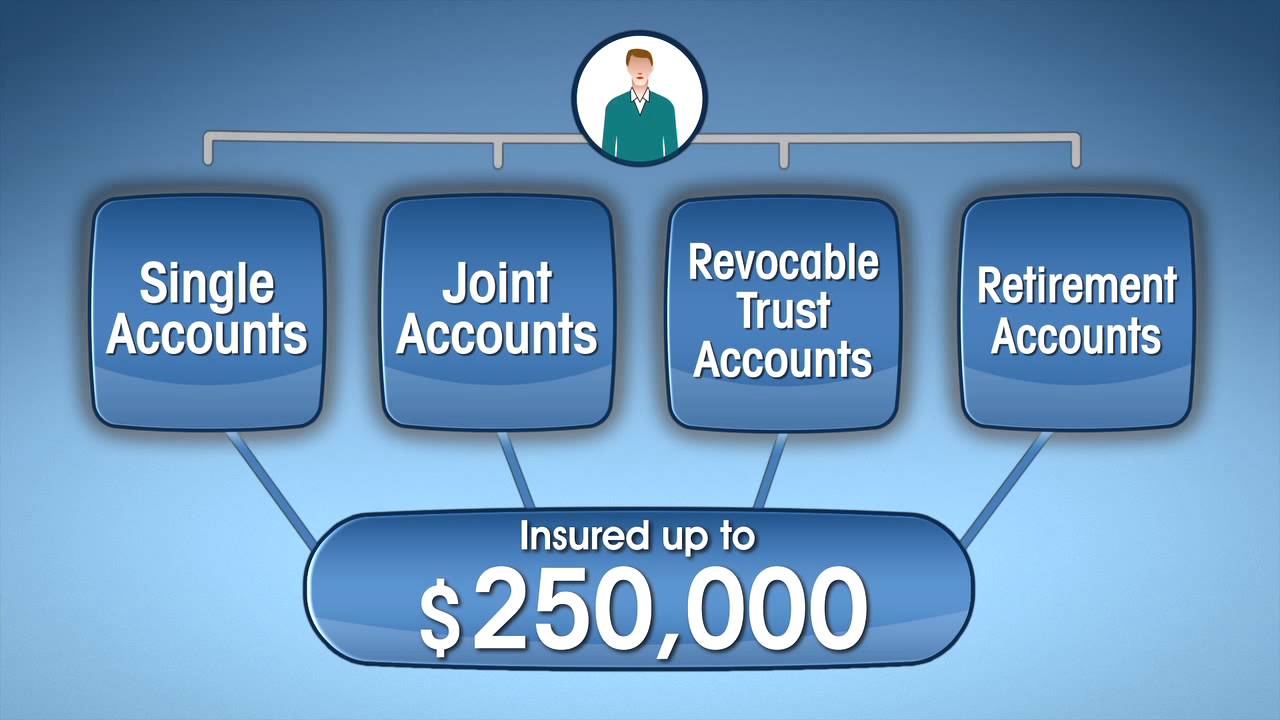

- Insured Deposits: Just like banks, credit union deposits are insured by the National Credit Union Administration (NCUA) up to $250,000 per account. This provides peace of mind knowing that your funds are protected.

Overall, credit unions offer a more personalized, member-centric approach to banking. By choosing a credit union, you become part of a community-focused institution that strives to provide affordable financial services, competitive rates, and outstanding customer service. The next step is to research different credit unions and find the one that best fits your needs and values.

Researching Credit Union Options

When it comes to choosing the right credit union, conducting thorough research is essential. Here are some steps you can take to evaluate different credit union options:

- Identify your needs: Start by understanding your specific banking needs. Consider the types of services you require, such as checking accounts, savings accounts, loans, credit cards, or investment opportunities. This will help you narrow down your options.

- Ask for recommendations: Reach out to friends, family, and colleagues who are credit union members and ask for their recommendations. Personal experiences and insights can be invaluable in making an informed choice.

- Check eligibility: Understand the membership eligibility criteria of each credit union. Some credit unions have specific requirements based on occupation, geographical location, or membership in certain organizations. Ensure that you are eligible to join before proceeding.

- Research online: Utilize online resources to research credit unions in your area. Visit their websites to gather information about their services, fees, rates, and membership requirements. Pay attention to their mission statements and values to see if they align with your own.

- Visit local branches: If possible, visit the physical branches of credit unions you are interested in. This will give you the opportunity to meet the staff, gauge the level of customer service, and get a sense of the overall atmosphere.

- Consider financial stability: Look at the financial health and stability of the credit unions you are considering. You can review their annual reports and financial statements, as well as look for any news or ratings about their performance. A financially stable credit union is more likely to provide reliable services.

- Compare fees and rates: Review the fee structures and interest rates offered by different credit unions. Pay attention to account maintenance fees, ATM fees, loan interest rates, and penalties for early account closure. Compare these charges to ensure that they align with your preferences and financial goals.

- Evaluate customer service: Read online reviews and testimonials from current and former members of the credit unions you are considering. Look for feedback on customer service, responsiveness, and problem resolution. A credit union with positive reviews for their customer service is likely to provide a better banking experience.

- Assess digital capabilities: In today’s digital age, it’s important to consider the online and mobile banking capabilities of credit unions. Check if they offer features like mobile banking apps, online bill payment, remote deposit capture, and access to ATMs and branches nationwide.

- Consider additional services: Think about any additional services or perks that are important to you. For example, some credit unions offer financial planning, insurance products, educational resources, or discounts on certain products and services.

By thoroughly researching credit union options, you’ll be equipped with the necessary information to make an informed decision. Remember to consider factors such as eligibility, services offered, financial stability, fees, customer service, digital capabilities, and any additional benefits provided. This will help you find the credit union that best meets your specific needs and financial goals.

Membership Eligibility

One key consideration when choosing a credit union is understanding the membership eligibility requirements. Unlike traditional banks, credit unions have specific criteria that determine who can become a member. Here are some common membership eligibility factors to consider:

- Employment-based: Many credit unions are established for the benefit of employees of a specific company or industry. These credit unions may require you to be an employee or a member of a certain organization or association to join. For example, there are credit unions specifically for healthcare professionals, teachers, or government employees.

- Geographical: Some credit unions serve a specific geographical area, such as a city, county, or state. To join these credit unions, you typically need to live, work, worship, or attend school within the designated area.

- Family Relationship: Certain credit unions allow members’ immediate family members, such as spouses, children, parents, and siblings, to join. This can be a great option if a family member is already a member of a credit union that you’re interested in.

- Membership Organizations: Some credit unions are open to members of certain organizations or associations. These can include professional organizations, alumni associations, trade unions, or other affiliations. If you belong to any of these organizations, you may be eligible to join their associated credit union.

- Community-based: In some cases, credit unions are open to anyone who resides in a specific community or neighborhood. These credit unions aim to serve the local community and may have more lenient membership requirements.

It’s important to carefully review the eligibility criteria of credit unions you are considering. Visit their websites or contact their customer service to determine if you meet the requirements. Keep in mind that some credit unions may have additional requirements, such as minimum age, specific identification, or opening a savings account with a minimum deposit.

If you find that you don’t meet the eligibility criteria for a specific credit union that you are interested in, don’t despair. There are many credit unions available, each with its own unique membership requirements. Take the time to explore different credit unions to find one that aligns with your eligibility criteria.

Remember, membership eligibility is an important factor, but it’s not the only one to consider when choosing a credit union. Evaluate other aspects such as services offered, fees, location, customer service, and online banking capabilities to ensure that the credit union meets all your needs.

Membership Benefits

When considering a credit union, it’s important to understand the benefits that come with membership. Credit union membership offers a variety of advantages that can enhance your banking experience and financial well-being. Here are some common membership benefits to consider:

- Competitive Interest Rates: Credit unions often offer more competitive interest rates on loans and savings accounts compared to traditional banks. This means you can potentially save money on interest payments or earn higher returns on your savings.

- Lower Fees: Credit unions generally have lower fees compared to traditional banks. They strive to keep costs down and pass on the savings to their members. This can result in substantial savings over time.

- Potential Dividends: As a member of a credit union, you may be eligible to receive dividends. Credit unions that generate profits can distribute a portion of those profits back to their members in the form of dividend payments.

- Personalized Service: Credit unions are known for their personalized approach and commitment to building strong relationships with their members. They take the time to understand your unique financial situation and offer tailored solutions to help you achieve your goals.

- Financial Education: Many credit unions provide financial education resources, workshops, and seminars to help their members improve their financial literacy. This can include topics like budgeting, saving, investing, and debt management.

- Access to Community Support: Credit unions have a strong community focus and often invest in local initiatives. By being a member, you indirectly support these community development projects and contribute to the well-being of your neighborhood.

- Shared Ownership: As a member, you have a say in the credit union’s decision-making process. You can participate in voting for the board of directors and be actively involved in shaping the future of the credit union.

- Increased Financial Security: Credit union deposits are insured by the National Credit Union Administration (NCUA) up to $250,000 per account, just like bank deposits. This means your funds are protected, providing peace of mind.

- Specialized Services: Some credit unions offer specialized services that cater to specific member needs. This can include services like small business banking, mortgage financing, student loans, or retirement planning.

- Discounts and Perks: Credit unions often partner with local businesses to offer discounts or other perks to their members. These can include reduced rates on loans, discounted tickets, or exclusive access to certain products or services.

Remember, the specific benefits you receive as a credit union member may vary depending on the institution. Be sure to research the benefits offered by the credit unions you are considering to ensure they align with your financial goals and preferences.

Membership benefits are an important aspect to consider when choosing a credit union. By joining a credit union, you gain access to personalized service, competitive rates, lower fees, and a host of additional perks that can improve your overall financial well-being.

Types of Services Offered

When choosing a credit union, it’s important to consider the range of services they offer. While the specific services may vary between credit unions, here are some common services you can expect:

- Savings Accounts: Credit unions offer various types of savings accounts, including regular savings, high-yield savings, certificates of deposit (CDs), and individual retirement accounts (IRAs). These accounts allow you to safely store and grow your funds.

- Checking Accounts: Credit unions provide checking accounts for everyday transactions. These accounts typically come with features such as check-writing, debit cards, online banking, and bill payment options.

- Loans: Credit unions offer a wide range of loan products, including personal loans, auto loans, mortgages, home equity loans, student loans, and small business loans. They often provide competitive interest rates and flexible repayment terms.

- Credit Cards: Many credit unions issue their own credit cards, offering competitive interest rates, rewards programs, and additional perks. Credit union credit cards can be a cost-effective way to manage your spending.

- Investment Services: Some credit unions offer investment options such as mutual funds, brokerage services, financial planning, and retirement accounts. These services can help you maximize your long-term financial growth.

- Online and Mobile Banking: Credit unions provide online banking platforms and mobile apps for convenient account access. This allows you to perform transactions, check balances, pay bills, transfer funds, and manage your finances from anywhere.

- Financial Education: Many credit unions prioritize financial education and offer resources to help you improve your financial literacy. This can include workshops, seminars, webinars, and educational materials.

- Business Services: Some credit unions cater to the needs of small businesses by offering business checking accounts, commercial loans, merchant services, payroll solutions, and business credit cards.

- Insurance Products: Certain credit unions collaborate with insurance providers to offer members access to various insurance products, including auto insurance, homeowners insurance, life insurance, and health insurance.

- Additional Services: Credit unions may also provide additional services such as wire transfers, notary services, safe deposit boxes, overdraft protection, and prepaid cards.

When selecting a credit union, it’s essential to assess which services align with your specific needs. Consider the services that you require currently and those that you may need in the future. Review the fees associated with these services to ensure they are reasonable and fit within your budget.

Remember, the range of services offered by credit unions can vary, so take your time to compare different options and find the credit union that offers the services you need to manage your finances effectively.

Evaluating Financial Stability

Ensuring the financial stability of a credit union is a crucial step in choosing the right institution for your banking needs. Here are some key factors to consider when evaluating the financial stability of a credit union:

- Financial Statements: Review the credit union’s financial statements, including the balance sheet, income statement, and cash flow statement. These documents provide insights into the credit union’s financial health, profitability, and liquidity.

- Asset Quality: Assess the quality of the credit union’s assets by reviewing their loan portfolio. Look for any indicators of higher default rates or delinquencies. A credit union with a low percentage of non-performing loans generally indicates better financial stability.

- Capital Adequacy: Evaluate the credit union’s capital adequacy ratio, which measures its ability to absorb potential losses. A higher capital ratio suggests stronger financial stability and a greater ability to withstand economic downturns.

- Asset Growth: Consider the credit union’s asset growth rate over time. Steady and sustainable growth indicates financial stability, while rapid or unsustainable growth may be a cause for concern.

- Profitability: Examine the credit union’s profitability, as indicated by their return on assets (ROA) and return on equity (ROE). A positive and consistent profitability trend demonstrates financial strength and the ability to generate income.

- National Credit Union Administration (NCUA) Reports: The NCUA provides reports and financial performance data for credit unions. Access their website to find information such as the credit union’s net worth, risk-based capital ratio, and regulatory compliance.

- Stability Ratings: Independent rating agencies may assign stability ratings to credit unions. These ratings assess the credit union’s financial strength and stability. Look for credit unions that have high ratings to ensure their financial soundness.

- Reserve Levels: Evaluate the credit union’s reserve levels and compare them to regulatory requirements. Adequate reserves indicate a proactive approach to managing potential risks and financial stability.

- Consistency: Look for consistent financial performance over time. A credit union that has maintained stability and financial strength through various economic cycles is more likely to continue providing reliable services in the future.

While evaluating the financial stability of a credit union can be complex, it is essential to ensure that your funds are in safe hands. Take the time to review financial statements, reports, and independent ratings to make an informed decision about the credit union’s financial stability.

Remember, financial stability is a critical aspect, but it shouldn’t be the sole basis for your decision-making. It is important to consider other factors such as membership eligibility, fees, services offered, customer service, and convenience to find the credit union that best meets your overall banking needs.

Fee Structure and Pricing

Understanding the fee structure and pricing of a credit union is crucial in selecting the right institution for your banking needs. Here are some considerations when evaluating the fee structure:

- Account Maintenance Fees: Check if the credit union charges any monthly or annual fees for maintaining your accounts. Some credit unions offer fee-free checking or savings accounts, while others may have fees for certain types of accounts.

- ATM Fees: Determine whether the credit union charges fees for using ATMs. Credit unions often have partnerships with other institutions or ATM networks, providing their members with access to fee-free ATMs.

- Transaction Fees: Consider any transaction fees associated with activities such as wire transfers, outgoing or incoming domestic or international transfers, stop payments, or excess transactions on savings accounts.

- Overdraft Fees: Find out the credit union’s policy on overdraft fees. Some credit unions do not charge overdraft fees, while others have a fee per occurrence. It is important to understand these fees and whether overdraft protection is available.

- Nonsufficient Funds (NSF) Fees: Determine the amount of the NSF fee charged for insufficient funds on checks or electronic debits. Knowing these fees can help you plan and avoid unnecessary charges.

- Credit Card Fees: If the credit union offers credit cards, review the fees associated with them, such as annual fees, balance transfer fees, cash advance fees, late payment fees, and foreign transaction fees.

- Loan Fees: Understand any fees related to loans, such as origination fees, application fees, or prepayment penalties. These fees can vary depending on the type of loan and the credit union’s policies.

- Account Closure Fees: Check if there are any fees associated with closing an account. Some credit unions may charge a fee if you close an account within a specific timeframe after opening it.

- Check Printing Fees: Determine whether there are fees for ordering checks or if the credit union offers free check printing services.

- Other Miscellaneous Fees: Be aware of any other miscellaneous fees that the credit union may charge, such as fees for returned mail, replacement cards, account research, or excessive coin deposits.

When comparing fee structures, consider the overall value of the services provided and how they align with your financial habits. A credit union with higher fees may offer additional benefits, such as higher interest rates, lower loan rates, or superior customer service.

It is essential to carefully read the credit union’s fee schedule and policies to fully understand the charges you may incur. Some credit unions may waive certain fees based on factors such as maintaining a minimum balance, direct deposit, or meeting specific transaction requirements.

By diligently reviewing the fee structure and pricing, you can choose a credit union that provides transparent and reasonable fees, ensuring that you can effectively manage your finances without incurring excessive charges.

Location and Accessibility

When selecting a credit union, considering the location and accessibility of its branches and services is important. Here are some key factors to consider:

- Branch Locations: Assess the proximity and number of branch locations to your home, workplace, or other frequently visited areas. Having branches conveniently located can make it easier to access in-person services and speak with a representative when needed.

- Branch Hours: Check the operating hours of the credit union’s branches to ensure that they align with your schedule. Some credit unions may offer extended hours or weekend hours, providing greater flexibility.

- Shared Branching: Find out if the credit union participates in a shared branching network. Shared branching allows members to conduct transactions and access services at other participating credit unions, expanding your access to services beyond your credit union’s own branches.

- ATM Network: Determine the size and accessibility of the credit union’s ATM network. Look for credit unions that have partnerships with other institutions or ATM networks to provide access to fee-free ATMs in your area or nationwide.

- Online and Mobile Banking: Evaluate the credit union’s online and mobile banking capabilities. Ensure that their digital platform offers features like mobile check deposit, bill payment, fund transfers, and transaction history. A robust online and mobile banking system can provide convenience and accessibility 24/7 from the comfort of your home or on the go.

- Telephone and Online Support: Consider the availability and quality of telephone and online customer support. A responsive and accessible customer service team can address your questions or concerns promptly.

- Accessibility for Individuals with Disabilities: Check if the credit union provides accessibility accommodations, such as wheelchair ramps, accessible ATMs, or braille and large-print materials for visually impaired individuals.

- Technology Integrations: Investigate whether the credit union integrates with popular personal finance management tools, allowing you to easily track and manage your finances across multiple platforms.

- Language Support: If English is not your primary language, confirm if the credit union offers support services in other languages. Language support can ensure clear communication and understanding.

Considering your preferences and banking habits, prioritize a credit union that provides convenient branch locations, extended hours, a robust ATM network, reliable online and mobile banking capabilities, and excellent customer support.

Keep in mind that while physical branch locations are important, advancements in digital banking have made location less of a determining factor. Many credit unions now offer a seamless online and mobile banking experience, making it easier to access services from anywhere.

Evaluating the location and accessibility factors will help you choose a credit union that aligns with your lifestyle, providing the convenience and ease of access you desire.

Customer Service and Support

When choosing a credit union, it is important to evaluate the level of customer service and support they provide. Here are some factors to consider:

- Accessibility: Assess the methods available to contact customer service, such as phone, email, live chat, or in-person visits. Look for a credit union that offers multiple channels of communication to address your needs and concerns.

- Response Time: Research the credit union’s reputation for responsiveness. Look for indications of prompt and efficient customer service, such as quick response times to inquiries or concerns.

- Staff Knowledge and Training: Consider the expertise and knowledge of the credit union’s staff. They should be well-trained and able to provide accurate information about the credit union’s products, services, and policies.

- Problem Resolution: Review feedback from current and past members regarding the credit union’s ability to resolve issues and problems effectively. Positive reviews about problem resolution indicate a commitment to member satisfaction.

- Member Feedback: Check online reviews and ratings to understand the experiences of other members. While individual reviews should be taken with a grain of salt, patterns and trends can provide valuable insights into the credit union’s overall service quality.

- Transparency: Look for a credit union that is transparent in their communication and disclosure of fees, policies, and terms. A transparent credit union aims to build trust and ensure that members are well-informed about their financial services.

- Financial Education: Evaluate whether the credit union provides educational resources such as workshops, seminars, or online materials to help members improve their financial literacy. A credit union that invests in member education demonstrates a commitment to the financial well-being of its members.

- Member Satisfaction: Consider the credit union’s track record in member satisfaction surveys or rankings. Positive ratings and feedback about the overall member experience indicate a credit union’s dedication to providing exceptional service.

- Complaint Resolution: Research the credit union’s procedures for handling member complaints. Check if they have a formal process in place and if they aim to resolve issues in a fair and timely manner.

- Corporate Values: Evaluate if the credit union’s values align with your own. Look for evidence of community involvement, corporate social responsibility, and a commitment to ethical standards.

By considering these factors, you can assess the credit union’s commitment to providing excellent customer service and support. A credit union with a strong focus on member satisfaction and effective communication can contribute to a positive banking experience.

Remember, customer service and support are essential throughout your banking relationship, from opening accounts to addressing any concerns or inquiries that may arise. Prioritizing a credit union with a reputation for exceptional customer service can ensure a smooth and satisfying banking experience.

Online and Mobile Banking Capabilities

In today’s digital age, online and mobile banking capabilities are a crucial consideration when choosing a credit union. Here are some key factors to evaluate:

- Mobile Banking App: Assess the features and functionality of the credit union’s mobile banking app. Look for a user-friendly interface, secure login processes, and the ability to perform essential banking tasks such as checking account balances, transferring funds, or making mobile deposits.

- Online Banking Platform: Review the credit union’s online banking platform. It should offer a comprehensive suite of services, including the ability to view account activity, pay bills, set up recurring payments, and manage external transfers.

- Security Measures: Ensure that the credit union employs robust security measures to protect your online and mobile banking transactions. Look for features such as multifactor authentication, encryption, and the ability to set up alerts for suspicious activity.

- Remote Deposit Capture: Determine if the credit union’s mobile banking app allows you to deposit checks remotely by capturing their images. This convenient feature eliminates the need to visit a branch or ATM to deposit checks.

- Bill Payment: Check if the credit union’s online and mobile banking platforms offer a bill payment feature. Look for the ability to add payees, schedule payments, and receive electronic or paper bill notifications.

- Transfers and Payments: Evaluate the ease and convenience of transferring funds between accounts within the credit union and to external accounts. Look for options such as one-time transfers, recurring transfers, and person-to-person payments.

- Account Alerts: Determine if the credit union’s online and mobile banking platforms allow you to set up custom account alerts. These alerts can notify you of important account activities, such as low balances, large withdrawals, or upcoming bill due dates.

- Budgeting and Financial Management Tools: Assess if the credit union’s online banking platform offers budgeting tools, spending categorization, or financial management features. These tools can help you track your expenses, set financial goals, and monitor your progress.

- Integrations: Check if the credit union’s online banking platforms integrate with personal finance management tools, such as Mint or Quicken. Seamless integration can simplify the process of managing your finances and provide a comprehensive view of your accounts.

- Customer Support: Evaluate the availability and quality of customer support for online and mobile banking. Look for responsive customer service channels, such as chat or phone support, to address any questions or issues you may encounter.

Online and mobile banking capabilities can greatly enhance your banking experience, providing convenience, accessibility, and real-time control over your finances. When comparing credit unions, prioritize the ones that offer robust and user-friendly online and mobile banking platforms.

Remember to also consider the credit union’s online and mobile banking security measures. It is crucial to choose a credit union that prioritizes the protection of your personal and financial information.

By selecting a credit union with advanced online and mobile banking capabilities, you can enjoy the convenience of managing your finances on the go and make banking transactions with ease, ensuring a seamless and efficient banking experience.

Reviews and Recommendations

Reading reviews and seeking recommendations from others can provide valuable insights into the experiences of current and past members of a credit union. Here’s how you can utilize reviews and recommendations:

- Online Reviews: Look for online reviews on reputable platforms such as Google, Yelp, or the Better Business Bureau. Read through a variety of reviews to get a balanced perspective on the credit union’s services, customer support, and overall member satisfaction.

- Member Testimonials: Check the credit union’s website for member testimonials or success stories. These testimonials can provide firsthand accounts of positive experiences and demonstrate the credit union’s ability to meet member needs.

- Seek Recommendations: Reach out to friends, family, and colleagues who are members of credit unions. Ask about their experiences, any challenges they encountered, and whether they would recommend their credit union. Personal recommendations can be a valuable source of information.

- Social Media Presence: Explore the credit union’s social media channels, such as Facebook, Twitter, or LinkedIn. Pay attention to comments and interactions from members, as it can give you an idea of the level of engagement and satisfaction within the community.

- Ask for Referrals: If you have narrowed down your choices to a few credit unions, consider reaching out to each one and asking for member referrals or references. Speaking directly with existing members can provide deeper insights into their experiences and level of satisfaction.

- Industry Rankings: Look for industry rankings or awards that recognize credit unions for their outstanding services and member satisfaction. These rankings can serve as an indicator of a credit union’s commitment to quality and member-centric banking.

- Consider Consistency: When reviewing feedback, consider patterns and consistency in the comments. Look for common themes or recurring positive and negative aspects of the credit union’s services. This can help you form a balanced view of their performance.

- Balance Reviews: Recognize that individual experiences can vary. Avoid making decisions solely based on one or two excessively negative or positive reviews. Instead, focus on overall trends and patterns to form a more informed opinion.

Reviews and recommendations can provide valuable insights into the satisfaction levels of current and past members. They can help you gauge the credit union’s reputation, customer service, fees, and overall banking experience.

Remember, while reviews and recommendations can be informative, they should not be the sole determinant of your decision. Consider other factors such as eligibility, services offered, fees, location, and accessibility to make a well-rounded decision when choosing a credit union.

Making Your Decision

After thoroughly researching and evaluating different credit unions based on eligibility, benefits, services, financial stability, fees, location, customer service, online and mobile banking capabilities, and reviews, it’s time to make your decision. Here are some steps to help you make an informed choice:

- Review Your Priorities: Take a moment to revisit your banking needs, financial goals, and personal preferences. Consider which factors are most important to you and prioritize them accordingly.

- Weigh the Benefits: Compare the membership benefits offered by each credit union, such as competitive interest rates, personalized service, financial education resources, and community involvement. Look for the credit union that aligns most closely with your needs.

- Consider Services and Fees: Review the services offered by each credit union and their fee structures. Consider your banking habits and financial activities to determine which credit union provides the most cost-effective solutions for your needs.

- Assess the Locations and Accessibility: Evaluate the convenience of branch locations, availability of fee-free ATMs, and online and mobile banking capabilities. Choose a credit union that provides the level of accessibility and convenience that fits your lifestyle.

- Evaluate Customer Service: Consider the quality and responsiveness of customer service based on reviews, recommendations, and personal interactions. Opt for a credit union committed to providing excellent customer support.

- Factor in Financial Stability: Take into account the financial health and stability of the credit unions you are considering. Look for evidence of strong financial performance, capital adequacy, and low default rates to ensure the long-term reliability of the institution.

- Trust Your Gut: Throughout the evaluation process, trust your instincts and intuition. Consider how comfortable and confident you feel with a particular credit union. A sense of trust and alignment with their values is essential for a successful banking relationship.

- Make a Decision: Based on your assessment of all the factors, weigh the pros and cons of each credit union and make your decision. Remember that no credit union is perfect, so focus on finding the one that best meets your needs and aligns with your financial goals.

- Join and Experience: Once you have made your decision, proceed with joining the selected credit union. Begin experiencing their services and interface firsthand. Evaluate if they live up to your expectations and address your financial needs.

Keep in mind that your banking needs may evolve over time. If you find that your chosen credit union no longer meets your requirements, remember that you can always reassess and switch to a different credit union in the future.

By following these steps and making an informed decision, you can confidently choose a credit union that aligns with your financial goals, provides excellent service, and contributes to your overall financial well-being.

Conclusion

Choosing the right credit union for your banking needs is a significant decision that can have a long-lasting impact on your financial well-being. By considering factors such as membership eligibility, benefits, services, financial stability, fees, location, customer service, online and mobile banking capabilities, and reviews, you can make an informed choice that aligns with your preferences and goals.

Remember that each individual’s banking needs and preferences may vary, so there is no one-size-fits-all solution. Take the time to assess your requirements, consider what matters most to you, and research different credit unions to find the best fit.

Once you have made your decision, join the credit union and start experiencing their services firsthand. Evaluate whether they meet your expectations in terms of service quality, convenience, and customer support.

Keep in mind that your financial journey is dynamic, and your needs may change over time. Regularly assess your banking relationship and make adjustments if necessary. It’s okay to switch to a different credit union or explore additional financial institutions that better suit your evolving needs.

Finally, remember that a credit union is more than just a place to keep your money. It is a community-focused institution that values its members and aims to provide personalized service, competitive rates, and financial education. By choosing the right credit union, you are not only gaining access to financial services but also becoming part of a community that supports your financial well-being.

So take the time to research, evaluate, and choose wisely. By selecting the right credit union, you can establish a trusted and valuable banking relationship that helps you achieve your financial goals and secure a solid financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance