Home>Finance>How To Enter A Negative Statement Balance When Reconciling In QuickBooks

Finance

How To Enter A Negative Statement Balance When Reconciling In QuickBooks

Published: March 2, 2024

Learn how to enter a negative statement balance when reconciling in QuickBooks with our expert finance tips. Keep your records accurate and up-to-date.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding Negative Statement Balances

In the world of finance and accounting, reconciling accounts is a critical task that ensures the accuracy of financial records. When using QuickBooks for this purpose, encountering negative statement balances can be a common occurrence. Understanding how to navigate and address these negative balances is essential for maintaining the integrity of financial data within the QuickBooks platform.

Negative statement balances can arise for various reasons, such as bank errors, outstanding checks, or unrecorded expenses. While they may initially appear as discrepancies, they are integral components of the overall financial picture. Therefore, knowing how to enter and reconcile negative statement balances in QuickBooks is vital for maintaining accurate financial records and ensuring that the reconciliation process is completed effectively.

This article will delve into the intricacies of negative statement balances, providing comprehensive guidance on how to enter and reconcile them within the QuickBooks software. By the end, readers will gain a clear understanding of how to manage negative statement balances, empowering them to navigate these situations with confidence and precision. Let's embark on this journey to unravel the nuances of handling negative statement balances in QuickBooks.

Understanding Negative Statement Balances

When reconciling accounts in QuickBooks, encountering negative statement balances can initially appear perplexing. However, these negative balances often stem from legitimate financial transactions and are crucial for maintaining accurate records. It’s essential to comprehend the underlying causes of negative statement balances to effectively address them within the QuickBooks platform.

Negative statement balances typically arise due to several factors, including outstanding checks, bank errors, unrecorded expenses, or timing differences in transaction processing. For instance, if a check is issued but not yet cashed by the recipient, it can result in a negative balance until the check is presented for payment. Similarly, bank errors or unrecorded expenses can contribute to negative balances, warranting careful attention during the reconciliation process.

Moreover, timing disparities in transaction processing between the company’s records and the bank statements can lead to negative balances. Transactions initiated towards the end of a statement period may not be reflected in the bank statement, causing temporary negative balances until the subsequent statement is issued. Understanding these nuances is pivotal for accurately interpreting negative statement balances and facilitating their reconciliation within QuickBooks.

Furthermore, negative balances are integral components of the overall financial landscape and should not be disregarded as mere discrepancies. Instead, they represent valid financial activities that necessitate proper documentation and reconciliation. By comprehending the diverse origins of negative statement balances, users can navigate the reconciliation process in QuickBooks with clarity and precision, ensuring that financial records remain accurate and reliable.

By grasping the intricacies of negative statement balances, users can effectively discern between genuine financial transactions and reconciliation anomalies. This understanding empowers users to confidently address negative balances within QuickBooks, fostering a more streamlined and accurate reconciliation process. With this foundational knowledge in place, let’s explore the practical steps for entering and reconciling negative statement balances in QuickBooks.

Entering Negative Statement Balances in QuickBooks

Entering negative statement balances in QuickBooks is a fundamental aspect of the reconciliation process, allowing users to accurately reflect the financial state of their accounts. QuickBooks provides intuitive methods for entering negative balances, enabling users to maintain precise financial records and ensure reconciliation accuracy.

One approach to entering negative statement balances in QuickBooks involves leveraging the “Make Deposits” feature. When encountering negative balances resulting from outstanding checks or unrecorded deposits, users can utilize the “Make Deposits” function to address these discrepancies effectively. By offsetting the negative balances with corresponding deposits or adjusting entries, users can rectify the discrepancies within QuickBooks, aligning the system’s records with the actual financial status.

Additionally, QuickBooks offers the option to record adjusting journal entries to address negative statement balances. This method allows users to make precise adjustments to account balances, accommodating various scenarios such as bank errors, unrecorded expenses, or timing differences in transaction processing. By recording adjusting journal entries, users can ensure that negative balances are accurately reflected in the financial records, fostering reconciliation integrity and financial transparency.

Furthermore, QuickBooks facilitates the seamless entry of negative statement balances through its user-friendly interface, empowering users to navigate the reconciliation process with ease. By leveraging the platform’s robust features and functionalities, users can efficiently input negative balances and maintain comprehensive financial records that align with the actual state of their accounts.

Entering negative statement balances in QuickBooks is a pivotal step towards ensuring the accuracy and reliability of financial records. By utilizing the platform’s versatile tools and functionalities, users can effectively address negative balances, fostering a more streamlined reconciliation process and upholding the integrity of their financial data.

As we’ve explored the methods for entering negative statement balances in QuickBooks, the subsequent section will delve into the intricacies of reconciling these negative balances within the platform, providing users with a comprehensive understanding of the reconciliation process.

Reconciling Negative Statement Balances in QuickBooks

Reconciling negative statement balances in QuickBooks is a crucial aspect of ensuring the accuracy and integrity of financial records. By navigating the reconciliation process with precision and attention to detail, users can effectively address negative balances, fostering a comprehensive understanding of their financial status within the QuickBooks platform.

One fundamental step in reconciling negative statement balances involves conducting a thorough review of all financial transactions and account activities. By meticulously analyzing bank statements, transaction records, and account histories within QuickBooks, users can identify the underlying causes of negative balances and initiate the reconciliation process with clarity and insight.

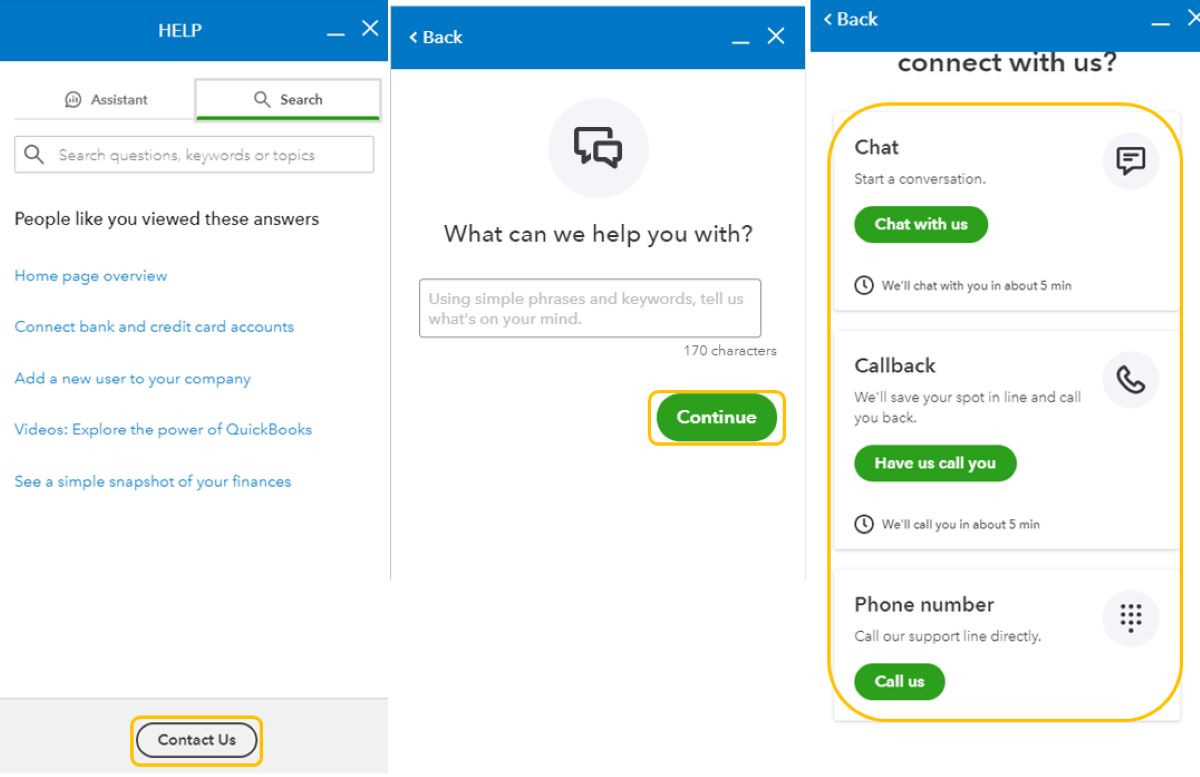

Furthermore, QuickBooks offers robust features for reconciling negative statement balances, such as the “Reconcile” tool, which enables users to compare their internal records with bank statements and address any disparities effectively. By leveraging this tool, users can systematically reconcile negative balances, ensuring that the financial records within QuickBooks accurately reflect the actual state of their accounts.

Moreover, proactive communication with financial institutions or relevant stakeholders can facilitate the reconciliation of negative statement balances. In cases where discrepancies persist or complex issues arise, reaching out to banks, vendors, or clients can provide valuable insights and resolutions, contributing to the comprehensive reconciliation of negative balances within QuickBooks.

Additionally, regular monitoring and periodic reconciliation of accounts are essential for detecting and addressing negative statement balances in a timely manner. By establishing consistent reconciliation practices and maintaining vigilance over account activities, users can promptly identify and reconcile negative balances, mitigating potential discrepancies and upholding the accuracy of financial records within QuickBooks.

By effectively reconciling negative statement balances in QuickBooks, users can cultivate a thorough understanding of their financial standing, mitigate discrepancies, and maintain the integrity of their financial records. This proactive approach to reconciliation fosters financial transparency and accuracy, empowering users to make informed decisions based on reliable and precise financial data.

As we’ve explored the intricacies of reconciling negative statement balances in QuickBooks, the subsequent section will culminate our journey by summarizing the key insights and practical considerations for managing negative balances within the platform.

Conclusion

Successfully managing negative statement balances in QuickBooks is an essential aspect of maintaining accurate financial records and ensuring reconciliation integrity. By comprehending the origins of negative balances, effectively entering them into the system, and navigating the reconciliation process with precision, users can foster a comprehensive understanding of their financial status within the QuickBooks platform.

Understanding the diverse factors that contribute to negative statement balances empowers users to discern between genuine financial transactions and reconciliation anomalies. By acknowledging the significance of outstanding checks, bank errors, unrecorded expenses, and timing disparities in transaction processing, users can approach negative balances with clarity and insight, fostering a proactive and informed reconciliation process.

Entering negative statement balances in QuickBooks is facilitated through intuitive methods such as leveraging the “Make Deposits” feature and recording adjusting journal entries. These approaches enable users to address negative balances effectively, aligning the system’s records with the actual financial state and maintaining comprehensive financial records within the platform.

Furthermore, reconciling negative statement balances in QuickBooks entails a meticulous review of financial transactions, proactive communication with relevant stakeholders, and consistent monitoring and reconciliation practices. By leveraging the platform’s robust features and tools, such as the “Reconcile” tool, users can systematically reconcile negative balances, fostering financial transparency and accuracy.

By actively managing negative statement balances in QuickBooks, users can cultivate a thorough understanding of their financial standing, mitigate discrepancies, and uphold the integrity of their financial records. This proactive approach to reconciliation empowers users to make informed decisions based on reliable and precise financial data, contributing to the overall financial health and stability of their business or organization.

In conclusion, navigating negative statement balances in QuickBooks is a pivotal aspect of financial management, requiring attention to detail, proactive reconciliation practices, and a comprehensive understanding of the reconciliation process. By embracing these principles and leveraging the platform’s functionalities, users can effectively manage negative balances, fostering financial transparency and accuracy within the QuickBooks environment.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance