Finance

How To Increase Personal Cash Flow

Modified: December 29, 2023

Learn effective strategies to increase your personal cash flow with our comprehensive finance guides and tips. Start managing your finances better today!

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Managing personal finances can sometimes be challenging, especially when it comes to cash flow. Cash flow is the measure of how money comes into and goes out of your bank account. It is important to have a positive cash flow, where the money coming in is greater than the money going out. This ensures financial stability and allows you to meet your financial goals and obligations.

Increasing personal cash flow is not an overnight process. It requires careful assessment of your current financial situation, analyzing your expenses and income, and implementing strategies to reduce expenses and increase income. By taking control of your cash flow, you can improve your financial well-being and have more financial freedom.

In this article, we will explore various strategies to increase personal cash flow. We will discuss how to assess your current cash flow, reduce expenses, increase income, create a budget, save and invest, manage debt, set financial goals, and track and monitor your cash flow. By following these steps, you will be well on your way to achieving a healthier and more sustainable financial future.

So, let’s dive in and discover the steps you can take to increase your personal cash flow and gain financial security.

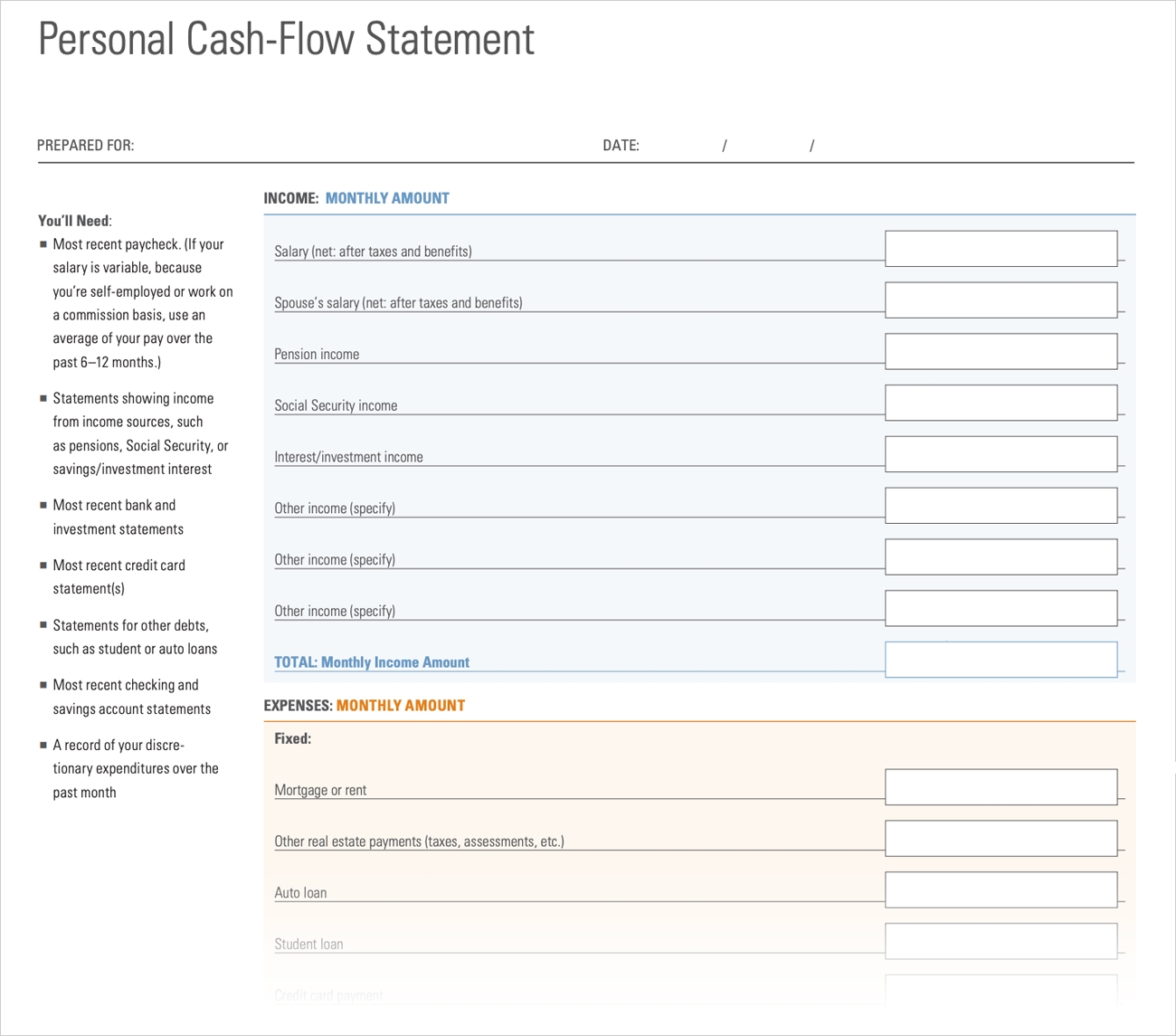

Assessing your current cash flow

Before you can start making changes to your cash flow, it’s important to have a clear understanding of your current financial situation. This involves assessing your current cash flow by analyzing your income and expenses.

Start by gathering all your financial records, such as bank statements, credit card statements, and receipts for the past few months. This will give you a comprehensive view of where your money is coming from and where it is going.

Next, categorize your expenses into different categories such as housing, transportation, groceries, entertainment, etc. This will help you identify areas where you may be overspending and where you can potentially cut back.

Take note of any income sources such as salaries, freelance work, rental income, or any other sources of income you may have. Calculate your total monthly income by adding up all these sources.

Once you have a clear picture of your income and expenses, calculate your net cash flow by subtracting your total expenses from your total income. If you have a positive net cash flow, it means you have more money coming in than going out, which is a good sign. However, if you have a negative net cash flow, it means you are spending more than you are earning, and you need to make adjustments to improve your cash flow.

Assessing your current cash flow will provide you with valuable insights on your spending habits and help you identify areas where you can make changes to increase your cash flow. It is the first step towards gaining control over your finances and working towards a healthier financial future.

Reducing expenses

One effective way to increase your personal cash flow is to reduce your expenses. By identifying areas where you can cut back and implementing cost-saving measures, you can free up more money to allocate towards savings or paying off debt. Here are some strategies to help you reduce your expenses:

- Create a budget: Start by creating a budget to track your income and expenses. This will give you a clear understanding of where your money is going, allowing you to identify unnecessary expenses.

- Review your recurring expenses: Take a close look at your monthly bills such as utilities, subscriptions, and memberships. Look for opportunities to switch to cheaper alternatives or eliminate those that are not essential.

- Lower your housing costs: Consider downsizing your home or renegotiating your rent or mortgage. You could also explore the option of refinancing your mortgage to secure a lower interest rate.

- Reduce transportation costs: Explore alternatives to driving, such as carpooling, using public transportation, or biking. If you own a car, make sure it is properly maintained to avoid costly repairs and consider downsizing to a more fuel-efficient model.

- Cut back on discretionary spending: Take a look at your discretionary expenses like eating out, entertainment, and shopping. Set limits on these expenses and look for ways to reduce or eliminate them entirely.

- Save on groceries: Consider meal planning, shopping sales, using coupons, and buying in bulk to save on your grocery bill. Look for ways to minimize food waste and cook at home more often.

- Manage your energy usage: Implement energy-saving practices like turning off lights and electronics when not in use, using programmable thermostats, and insulating your home to reduce energy costs.

- Eliminate high-interest debt: Pay off high-interest debt as soon as possible to minimize interest charges. Explore options like balance transfers or debt consolidation to lower your interest rates.

By implementing these strategies, you can significantly reduce your monthly expenses and increase your cash flow. It’s important to regularly review your budget and expenses to ensure you stay on track and continue finding ways to cut costs. Remember, even small savings can add up over time and make a big impact on your overall financial situation.

Increasing income

Reducing expenses is one side of the coin when it comes to increasing personal cash flow. The other side is finding ways to increase your income. By boosting your income, you can have more money available to save, invest, or allocate towards other financial goals. Here are some strategies to help you increase your income:

- Take on a side gig: Consider taking on a side job or freelancing to earn extra income. There are various opportunities available such as freelance writing, graphic design, tutoring, or driving for rideshare services.

- Negotiate a raise: If you are employed, gather evidence showcasing your contributions and accomplishments and consider negotiating a raise with your employer. Presenting a strong case for your value can increase your chances of receiving a salary increase.

- Pursue professional development: Invest in your skills and education to increase your earning potential. Take courses, attend workshops or seminars, or pursue certifications in your field to enhance your expertise and marketability.

- Rent out assets: If you have extra space in your home or own assets such as a car or equipment, consider renting them out to earn passive income. Platforms like Airbnb and Turo make it easy to connect with potential renters.

- Create and sell a product or service: If you have a talent or a passion, consider creating a product or offering a service that you can sell. This could be anything from handmade crafts to consulting services.

- Invest in income-generating assets: Explore ways to invest in assets that generate passive income, such as rental properties, dividend-paying stocks, or peer-to-peer lending platforms. These investments can provide a steady stream of income over time.

- Monetize your hobbies: If you have a hobby that you enjoy, consider finding ways to monetize it. This could be through selling handmade items, teaching classes or workshops, or offering services related to your hobby.

It’s important to remember that increasing your income may require time and effort. Be prepared to invest in yourself, explore new opportunities, and build your skills. In addition, it’s crucial to have a clear plan for your additional income, whether it’s to save, invest, or pay down debt.

By finding ways to increase your income, you can significantly improve your cash flow and achieve your financial goals faster. The key is to be proactive, open-minded, and willing to explore different avenues for generating additional income.

Creating a budget

Creating a budget is a crucial step in managing your personal finances and increasing your cash flow. A budget helps you track and control your income and expenses, giving you a clear picture of where your money is going. It allows you to allocate your resources effectively and make informed financial decisions. Here are some steps to help you create a budget:

- Calculate your income: Begin by calculating your total income, including your salary, freelance work, rental income, or any other sources. Make sure to consider your net income, which is your income after taxes and deductions.

- List your expenses: Make a list of all your monthly expenses, including both fixed expenses (such as rent or mortgage payments, utilities, and insurance) and variable expenses (such as groceries, transportation, entertainment, and personal expenses).

- Categorize your expenses: Categorize your expenses into different categories, such as housing, transportation, groceries, entertainment, and debt payments. This will help you understand your spending patterns and identify areas where you can potentially cut back.

- Set financial goals: Determine your short-term and long-term financial goals. These could include saving for emergencies, paying off debt, saving for a down payment on a home, or planning for retirement. Make sure your budget reflects these goals and allocates funds accordingly.

- Allocate your income: Allocate your income to cover your expenses, savings, and other financial goals. Start with essentials such as housing, utilities, and food, and then allocate funds to other categories based on their importance and priority.

- Track your spending: Keep track of your expenses to ensure they align with your budget. Use a budgeting app or a spreadsheet to record your expenses and compare them with your budget. This will help you identify any areas where you may be overspending.

- Adjust and refine: Regularly review and adjust your budget as needed. As your financial situation changes or your goals shift, you may need to reallocate funds or make adjustments to your expenses.

Creating a budget empowers you to make mindful financial decisions and prioritize your spending. It helps you identify areas where you can reduce expenses and find opportunities to save or invest your money. By sticking to your budget, you can effectively manage your cash flow and work towards achieving your financial goals.

Saving and investing

Building savings and investing is a crucial part of increasing personal cash flow and securing your financial future. By saving and investing, you can grow your wealth and generate passive income over time. Here are some strategies to help you save and invest:

- Set savings goals: Start by determining your savings goals. Whether it’s an emergency fund, a down payment on a house, or a retirement nest egg, having specific goals will motivate you to save consistently.

- Create an automatic savings plan: Set up automatic transfers from your paycheck to a dedicated savings account. This ensures that a portion of your income goes towards savings without you having to think about it.

- Reduce expenses and save the difference: Cut back on unnecessary expenses and redirect the savings towards your savings account. Small daily choices can add up over time and significantly impact your overall savings.

- Build an emergency fund: Aim to save three to six months’ worth of living expenses in an emergency fund. This provides a safety net in case of unexpected financial challenges or job loss.

- Explore different savings accounts: Research different types of savings accounts, such as high-interest savings accounts or certificates of deposit (CDs), to maximize the return on your savings. Choose accounts that offer competitive interest rates and low fees.

- Invest in retirement accounts: Contribute to retirement accounts such as employer-sponsored 401(k) plans or individual retirement accounts (IRAs). Take advantage of any employer matching contributions and consider increasing your contributions over time.

- Diversify your investments: Spread your investments across different asset classes, such as stocks, bonds, and real estate, to reduce risk. Consider consulting with a financial advisor to help you develop an investment strategy that aligns with your goals.

- Monitor and adjust your investments: Regularly review your investment portfolio and make adjustments based on your risk tolerance and market conditions. Rebalance your portfolio as needed to maintain a diversified and balanced investment strategy.

Remember, saving and investing is a long-term commitment. Start small if you need to, but be consistent in saving and investing over time. As you accumulate savings and investment returns, your personal cash flow will increase, and you’ll be on the path to achieving financial freedom.

Managing debt

Debt can be a significant drain on your cash flow and hinder your financial progress. Managing and reducing debt is an essential step in increasing your personal cash flow. Here are some strategies to help you effectively manage your debt:

- Organize and prioritize your debt: Make a list of all your debts, including the outstanding balance, interest rates, and minimum monthly payments. Arrange them in order of priority, focusing on high-interest debt first.

- Create a debt repayment plan: Develop a realistic plan to pay off your debts. Consider using the snowball or avalanche method, where you either start with the smallest debt or the one with the highest interest rate while making minimum payments on the others.

- Negotiate lower interest rates: Contact your creditors to negotiate lower interest rates. A lower interest rate can help reduce the amount of interest you pay over time, making it easier to pay off your debt faster.

- Consolidate debt: If you have multiple high-interest debts, consider consolidating them into a single loan with a lower interest rate. This can make it easier to manage and potentially save you money on interest payments.

- Avoid taking on new debt: While paying off existing debt, avoid incurring new debt whenever possible. Focus on living within your means and using cash or existing savings for your expenses instead of relying on credit.

- Increase your income: Find ways to increase your income to allocate more money towards debt repayment. Consider taking on a part-time job or freelancing to generate additional income specifically dedicated to paying off your debts.

- Seek professional help if needed: If your debt feels overwhelming and you’re struggling to make progress, consider seeking help from a credit counseling agency or a financial advisor. They can provide guidance and assistance in managing your debt.

- Celebrate milestones: Celebrate small victories along the way as you pay off your debt. This will keep you motivated and reinforce your commitment to becoming debt-free.

Remember, managing debt takes time and discipline. Stay committed to your debt repayment plan and avoid accumulating new debt. As you reduce and eliminate debt, your personal cash flow will increase, allowing you to allocate more money towards savings and achieving your financial goals.

Setting financial goals

Setting clear financial goals is essential for increasing your personal cash flow and achieving financial success. Goals give you direction, motivation, and a sense of purpose in your financial journey. Here are some steps to help you set effective financial goals:

- Identify your priorities: Determine what matters most to you and align your goals accordingly. Reflect on your values and aspirations to ensure that your financial goals are meaningful and in line with your long-term vision.

- Set SMART goals: Make your goals specific, measurable, achievable, relevant, and time-bound (SMART). For example, rather than saying “I want to save money,” set a goal like “I want to save $10,000 for a down payment on a house within the next two years.”

- Break down big goals into smaller milestones: Large goals can seem overwhelming, so break them down into smaller, manageable milestones. This allows you to track your progress and stay motivated along the way.

- Balance short-term and long-term goals: Consider both short-term goals, such as building an emergency fund, and long-term goals, such as saving for retirement. Finding a balance allows you to address immediate needs while also planning for the future.

- Make your goals realistic: Be realistic about your financial situation and capabilities when setting goals. Consider factors such as your income, expenses, and any existing debts. Setting unrealistic goals can lead to frustration and disappointment.

- Write your goals down: Documenting your goals makes them tangible and increases your commitment to achieving them. Write them in a place where you can refer to them regularly, such as a journal or a vision board.

- Review and revise your goals: Regularly review your goals and track your progress. Adjust your goals as needed based on changes in your circumstances or priorities. Stay flexible and adapt your goals as your financial situation evolves.

- Celebrate your achievements: Celebrate each milestone you achieve along the way. Rewarding yourself for your progress reinforces positive financial habits and keeps you motivated on your journey.

Setting financial goals gives you a roadmap for your financial success. It helps you stay focused, make intentional decisions with your money, and ultimately increase your personal cash flow. Remember to regularly review and adapt your goals as needed to ensure they remain relevant and aligned with your financial aspirations.

Tracking and monitoring your cash flow

Tracking and monitoring your cash flow is crucial to ensure that you are making progress towards your financial goals and maintaining a healthy financial situation. By keeping a close eye on your income and expenses, you can identify any areas of concern, make adjustments, and stay on track. Here are some steps to help you effectively track and monitor your cash flow:

- Track your income and expenses: Regularly record and categorize your income and expenses. This can be done using a spreadsheet, personal finance software, or a dedicated budgeting app. Having a clear breakdown of where your money is coming from and where it is going will provide valuable insights.

- Review your spending habits: Regularly review your expenses to identify any patterns or areas where you may be overspending. Look for opportunities to cut back or find more cost-effective alternatives.

- Compare your actual spending to your budget: Regularly compare your actual spending to your budgeted amounts. This will help you identify any discrepancies and make necessary adjustments to align with your financial goals.

- Analyze your cash flow: Assess your cash flow on a monthly or quarterly basis. Calculate your net cash flow by subtracting your total expenses from your total income. Analyze the trends and fluctuations in your cash flow to gain insights into your financial health.

- Identify areas for improvement: Pay attention to categories where you consistently overspend or areas where you can potentially reduce expenses. Look for opportunities to optimize your spending and increase your cash flow.

- Set financial milestones: Establish specific financial milestones that you want to achieve and track your progress towards them. This could include milestones such as paying off a certain amount of debt, reaching a savings target, or increasing your investment portfolio.

- Revisit and adjust your budget: Regularly review and update your budget based on changes in your income, expenses, or financial goals. Be flexible and make adjustments to ensure your budget remains realistic and aligns with your current circumstances.

- Use technology to your advantage: Take advantage of personal finance apps and online tools that can automate your budgeting and expense tracking. These tools can provide real-time updates and insights into your cash flow, making it easier to stay organized and informed.

By consistently tracking and monitoring your cash flow, you can stay in control of your finances, make informed decisions, and optimize your financial situation. It allows you to proactively manage your cash flow and ensure that you are making progress towards your financial goals. Remember, regular monitoring and ongoing adjustments are key to maintaining a healthy cash flow over time.

Conclusion

Increasing personal cash flow is a journey that requires diligence, discipline, and a clear understanding of your financial situation. By assessing your current cash flow, reducing expenses, increasing income, creating a budget, saving and investing, managing debt, setting financial goals, and tracking your cash flow, you can take control of your finances and work towards a healthier and more secure financial future.

Reducing expenses and finding ways to increase your income are two critical steps in increasing your cash flow. By analyzing your spending habits and making strategic adjustments, you can free up more money to save, invest, and allocate towards your financial goals.

A budget serves as a roadmap for your finances, helping you allocate your resources effectively and prioritize your spending. Regularly reviewing and adjusting your budget ensures that your cash flow remains in line with your financial goals and aspirations.

Remember to save and invest your money wisely. Building savings and investing in assets that generate passive income can have a significant impact on your overall cash flow. Setting specific financial goals helps you stay focused and motivated as you work towards achieving financial security.

Lastly, tracking and monitoring your cash flow is vital to ensure that you stay on track and make necessary adjustments along the way. By keeping a close eye on your income and expenses, you can identify areas for improvement and make informed decisions about your finances.

In conclusion, increasing personal cash flow requires consistent effort and a proactive approach to managing your finances. By implementing the strategies outlined in this article, you can take control of your cash flow, improve your financial well-being, and pave the way towards a more prosperous and secure future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance