Finance

How To Set Up Retirement Planning When Young

Published: January 21, 2024

Learn how to strategically plan for your retirement from a young age. Discover the best finance tips and tricks to secure your financial future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

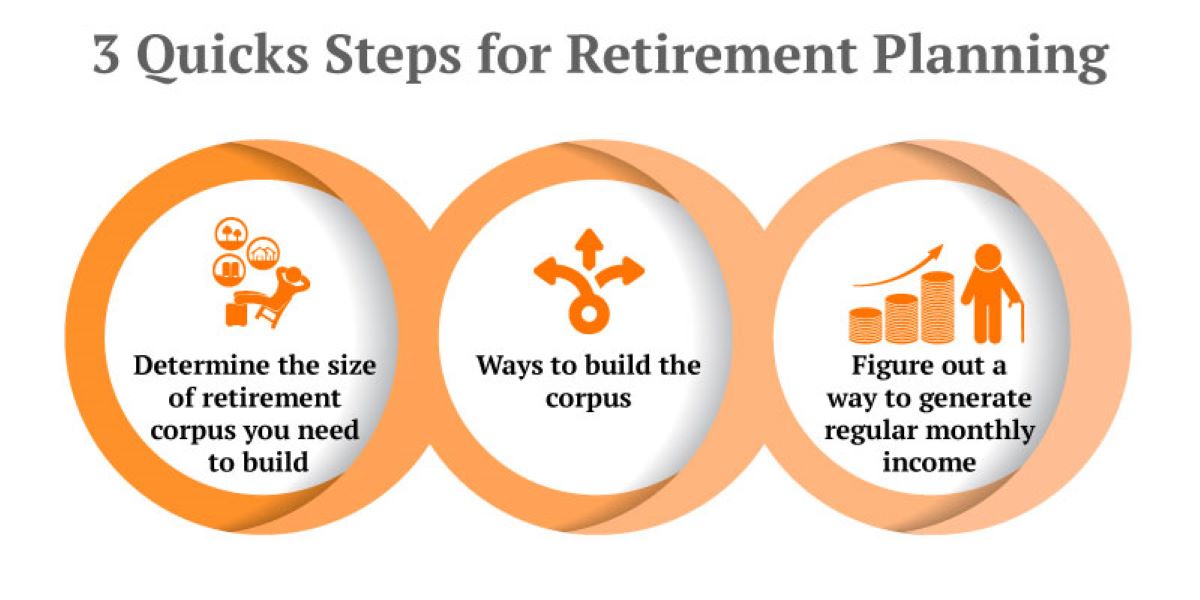

- Introduction

- Why is retirement planning important for young adults?

- Start saving early

- Determine your retirement goals

- Assess your current financial situation

- Create a budget

- Explore retirement account options

- Maximize employer contributions

- Consider additional retirement savings options

- Invest wisely

- Review and adjust your retirement plan regularly

- Conclusion

Introduction

Retirement planning is often seen as something that only older adults need to worry about. However, starting to plan for retirement at a young age is crucial for setting a strong financial foundation and ensuring a comfortable future. While it may seem like retirement is a distant goal, the earlier you start planning, the more time you have to save and invest, increasing your chances of achieving your retirement goals.

Many young adults are burdened with student loans and other financial responsibilities, making it challenging to think about retirement. However, by implementing some key strategies and making informed decisions, you can set up a solid retirement plan that will put you on the path to financial security.

In this article, we will explore the various steps involved in setting up retirement planning when you are young. From starting to save early to investing wisely, we will provide insights and tips to help you establish a comprehensive retirement strategy that meets your future financial needs.

While retirement planning may seem overwhelming, taking the time now to understand your options and make smart decisions will pay off in the long run. So let’s dive in and learn how to set up retirement planning when you are young!

Why is retirement planning important for young adults?

Retirement planning is often overlooked by young adults who are focused on building their careers, paying off debt, or enjoying their youth. However, starting to plan for retirement at a young age is crucial for several reasons:

- Increased Time Horizon: One major advantage young adults have is time. By starting to save and invest early, you can take advantage of the power of compounding. Even small contributions made now can grow significantly over time, allowing you to accumulate a substantial nest egg for retirement.

- Rising Life Expectancy: Life expectancies are increasing, which means that retirement may last for several decades. Without proper planning, you may risk outliving your savings and struggling to maintain a comfortable lifestyle during your retirement years.

- Uncertain Social Security Benefits: Social Security benefits may not be sufficient to cover all your retirement expenses. The future of Social Security is uncertain, and depending solely on it may leave you financially vulnerable. By having your own retirement savings, you can supplement your income and maintain your desired standard of living.

- Changing Job Market: The job market is constantly evolving, and there are no guarantees that your current job will provide a pension or retirement plan. By taking control of your retirement planning, you are not reliant on an employer to secure your future.

- Financial Independence and Flexibility: Retirement planning allows you to achieve financial independence and gives you the flexibility to make choices based on your preferences, rather than financial necessity. Whether it’s starting a business, traveling the world, or pursuing hobbies, proper planning ensures that you have the means to live out your dreams.

Overall, retirement planning is important for young adults to secure their financial future and maintain a comfortable lifestyle when they can no longer generate a regular income from work. By starting early and being proactive, you can build a solid financial foundation, maximize your savings potential, and enjoy a worry-free retirement.

Start saving early

When it comes to retirement planning, one of the most crucial factors is to start saving early. The power of compounding can work wonders for your retirement savings if you give it enough time. Here are some key reasons why starting early is important:

- Maximizing the Benefits of Compound Interest: Compound interest is the magic that allows your savings to grow exponentially over time. By starting early, you give your money more time to compound, generating additional interest on both your initial contributions and the accumulated earnings. This can significantly boost your retirement savings in the long run.

- Less Pressure on Monthly Contributions: Starting to save early means smaller monthly contributions, as you have a longer time horizon to accumulate your desired retirement fund. This can alleviate some financial burden in the present, making it easier to incorporate saving into your budget.

- Flexibility and Room for Error: Starting early gives you the flexibility to take risks and make mistakes along the way. You can learn from any investment losses and adjust your strategy accordingly, without jeopardizing your retirement plans.

- Building Good Saving Habits: Starting early instills discipline and good saving habits. By making saving a priority from a young age, you develop self-discipline and financial responsibility, which will be beneficial not just for retirement, but for other financial goals throughout your life.

While it may seem challenging to save when you are in the early stages of your career or have other financial obligations, every little bit counts. Even small contributions can make a significant difference over time, thanks to the power of compounding. Here are some tips to help you start saving early:

- Set a Budget: Determine your income and expenses, and create a budget that includes a portion for retirement savings. It’s important to prioritize saving for your future.

- Avoid Lifestyle Inflation: As your income increases, it’s tempting to increase your spending. However, try to keep your expenses in check and save the extra money towards your retirement goals.

- Automate Savings: Set up automatic transfers from your paycheck to a retirement account or savings account. This way, you won’t be tempted to spend the money and it will grow without much effort on your part.

- Take Advantage of Employer Matches: If your employer offers a 401(k) match, contribute at least enough to receive the maximum match amount. This is essentially free money and can significantly boost your retirement savings.

- Start with Small Amounts: If you’re finding it difficult to save a large percentage of your income, start with a smaller amount and gradually increase it as your income grows.

By starting to save early and cultivating good saving habits, you can set yourself up for a financially secure retirement. Remember, the key is to take the first step and start saving as soon as possible.

Determine your retirement goals

Before you can effectively plan for retirement, it’s important to have a clear understanding of your retirement goals. Defining your goals will help you determine how much you need to save and the strategies you should employ. Here are some steps to help you determine your retirement goals:

- Visualize Your Ideal Retirement: Take some time to imagine your ideal retirement lifestyle. Consider where you want to live, the activities you want to pursue, and the kind of financial security you desire. This will give you a clearer picture of what you are working towards.

- Estimate Your Retirement Expenses: Calculate your anticipated expenses during retirement. Consider all aspects, including housing, healthcare, daily living expenses, travel, and any other activities or goals you wish to pursue. Don’t forget to factor in inflation and potential healthcare costs.

- Consider Your Retirement Age: Determine at what age you plan to retire. This will impact the number of years you have to save and the income you will need to sustain yourself throughout retirement.

- Evaluate Your Risk Tolerance: Assess your risk tolerance and determine how comfortable you are with investing in potentially higher-yield, but riskier assets. Your risk tolerance will influence your asset allocation strategy and the investments you choose.

- Consult a Financial Advisor: If you’re unsure about estimating your retirement goals or need professional guidance, consider consulting a financial advisor. They can help you navigate the complexities of retirement planning and provide personalized advice.

Once you have a clear idea of your retirement goals, you can create a financial plan to achieve them. It’s important to regularly review and reassess your goals as your circumstances, priorities, and market conditions change.

Remember, retirement is a personal journey, and everyone’s goals and circumstances are unique. Don’t compare yourself to others or feel pressured to meet certain standards. Instead, focus on what matters most to you and create a retirement plan that aligns with your dreams and values.

Having well-defined retirement goals will provide a sense of purpose and direction to your financial planning efforts. It will also motivate you to stay disciplined and make the necessary sacrifices to ensure a secure and fulfilling retirement.

Assess your current financial situation

Before you can effectively plan for your retirement, it’s important to assess your current financial situation. This step will give you a clear understanding of where you stand financially and provide a baseline for developing your retirement plan. Here are some key factors to consider when assessing your financial situation:

- Evaluate Your Income: Determine your current income from all sources, including salaries, bonuses, freelance work, and investments. This will help you gauge your earning potential and the amount of money you can allocate towards retirement savings.

- Track Your Expenses: Review your expenses and identify areas where you can potentially cut back and save more. Look for any unnecessary spending habits and consider adjusting your lifestyle to free up additional funds for retirement savings.

- Analyze Your Debt: Assess your current debt, including student loans, credit card debt, and mortgages. Paying down high-interest debt should be a priority, as it can negatively impact your ability to save for retirement.

- Calculate Your Net Worth: Determine your net worth by subtracting your liabilities (debts) from your assets (savings, investments, property, etc.). This will give you an overall snapshot of your financial health and help you understand your current financial standing.

- Review Existing Retirement Accounts: If you already have retirement accounts, such as a 401(k) or an IRA, review their performance and contribution rates. Consider whether you need to adjust your contributions or explore other investment options to maximize growth.

Once you have a clear understanding of your current financial situation, you can make informed decisions about your retirement savings strategy. Keep in mind that properly assessing your finances may require time and effort, but the insights gained will be invaluable in setting realistic goals and crafting a plan tailored to your needs.

If you find that your financial situation is not ideal or that you are struggling to save for retirement, don’t despair. Use this assessment as a starting point to identify areas for improvement and take proactive steps towards financial stability. This may involve seeking additional sources of income, reducing expenses, or seeking professional financial advice.

Remember, assessing your current financial situation is a crucial step in creating a roadmap for your retirement journey. By understanding where you currently stand, you can develop a more effective and targeted plan to achieve your desired retirement goals.

Create a budget

Creating a budget is a fundamental step in any financial planning process, including retirement planning. A budget helps you gain control over your spending, prioritize your savings goals, and ensure you are on track to meet your retirement objectives. Here’s a step-by-step guide on creating a budget:

- Track Your Income: Start by identifying your sources of income. This includes your salary, side hustles, investment income, and any other money coming in each month. Calculate your total monthly income.

- List Your Expenses: Make a comprehensive list of all your expenses. This includes fixed expenses such as rent/mortgage, utilities, insurance, and loan repayments, as well as variable expenses like groceries, entertainment, dining out, and transportation.

- Categorize Your Expenses: Organize your expenses into categories to help you understand where your money is going. Examples of categories include housing, transportation, food, healthcare, debt payments, and entertainment.

- Analyze Your Spending: Review your expenses to identify areas where you can cut back or make adjustments. Look for any unnecessary or excessive spending habits that can be reduced to save more for retirement.

- Create Saving Categories: Allocate a portion of your income specifically for retirement savings. Aim to save a percentage of your income each month, and make it a priority to contribute consistently.

- Set Realistic Goals: Determine how much you aim to save for retirement each month and set realistic milestones. Use these goals as benchmarks to track your progress and make adjustments as needed.

- Monitor and Adjust: Regularly review your budget and track your expenses to ensure you are staying on track. Make necessary adjustments if you find that you are overspending or have extra funds available for retirement savings.

Creating a budget is not a one-time task; it requires ongoing monitoring and adjustment as your financial situation evolves. It’s important to be disciplined and stick to your budget, but also allow for flexibility when needed.

Remember, budgeting is not about restricting yourself or feeling deprived. It’s about understanding your spending patterns, making intentional choices, and aligning your money with your goals and priorities. By creating a budget and allocating funds towards retirement savings consistently, you’ll be better equipped to achieve financial security and enjoy a comfortable retirement.

Explore retirement account options

When it comes to saving for retirement, there are several retirement account options available to help you maximize your savings and take advantage of tax benefits. Here are some popular retirement account options to consider:

- 401(k) Plans: 401(k) plans are employer-sponsored retirement accounts. Contributions are made pre-tax, meaning they are deducted from your paycheck before taxes are taken out. Some employers also offer a matching contribution, which is essentially free money. Take advantage of the maximum employer match if available.

- Traditional IRAs: Individual Retirement Accounts (IRAs) allow you to contribute pre-tax dollars, which can be deducted from your taxes in the year of contribution. The money grows tax-deferred until you withdraw it during retirement.

- Roth IRAs: Roth IRAs are funded with after-tax dollars, meaning you don’t get a tax deduction upfront. However, qualified withdrawals during retirement are tax-free. Roth IRAs are advantageous if you anticipate being in a higher tax bracket in retirement.

- SIMPLE IRAs: SIMPLE (Savings Incentive Match Plan for Employees) IRAs are geared towards small businesses and self-employed individuals. They offer either an employer match or a mandatory employer contribution, making it an attractive retirement savings option for small business owners.

- Solo 401(k) Plans: If you’re self-employed, a solo 401(k) plan allows you to save for retirement as both the employer and employee. This means you can contribute more compared to traditional IRAs or SEP IRAs.

- Health Savings Accounts (HSAs): While primarily used for healthcare expenses, HSAs can also serve as retirement savings vehicles. Contributions are tax-deductible, growth is tax-free, and qualified withdrawals for healthcare expenses are tax-free.

Each retirement account option has its own contribution limits, withdrawal rules, and tax implications. It’s important to research and understand the specifics of each account type to determine which ones align with your financial goals and tax situation.

Additionally, consider diversifying your retirement savings by utilizing a combination of these accounts. This allows you to benefit from different tax advantages and provides more flexibility in managing your retirement income in the future.

When exploring retirement account options, it’s also essential to consider factors such as your age, income level, and eligibility requirements. Consulting with a financial advisor can help you assess your needs and choose the most suitable retirement accounts that will help you meet your savings goals.

Remember to regularly monitor and review your retirement accounts, ensuring that you optimize your contributions and take advantage of any investment opportunities that may arise. A well-rounded retirement account portfolio can go a long way towards building a secure and comfortable retirement.

Maximize employer contributions

One of the most valuable perks of many retirement plans is the employer contribution. It’s essential to understand and maximize this benefit as it can significantly boost your retirement savings. Here’s why maximizing employer contributions is crucial:

- Free Money: Employer contributions to retirement accounts are essentially free money. Taking advantage of these contributions allows you to increase your retirement savings without any additional cost to you.

- Higher Savings Rate: By maximizing employer contributions, you can reach your savings goals faster. It accelerates the growth of your retirement nest egg and increases the overall value of your account over time.

- Tax Advantage: Employer contributions are typically made with pre-tax dollars, reducing your taxable income and potentially lowering your tax liability for the year.

- Long-Term Impact: The compounding effect of employer contributions can be substantial over time. By starting early and consistently maximizing employer contributions, you can significantly increase your retirement savings and reach your financial goals.

To maximize your employer contributions, consider the following strategies:

- Contribute at Least the Minimum: Ensure that you are contributing at least the minimum amount required to receive the maximum employer match. Failing to do so means you’re leaving free money on the table.

- Increase Your Contributions Over Time: Whenever possible, incrementally increase your contributions to maximize the employer match. This allows you to take advantage of compounding growth and increase your retirement savings.

- Take Advantage of Vesting Periods: Some employer contributions may be subject to a vesting period. It’s crucial to understand the vesting schedule, as it determines your ownership of the employer contributions. Stay with the company long enough to fully vest and maximize the benefits.

- Automate Contributions: Set up automatic contributions from your paycheck to ensure consistent savings and make the most of your employer match. This eliminates the risk of forgetting or being tempted to spend the money elsewhere.

- Understand Plan Rules and Limits: Familiarize yourself with the rules and limits of your employer-sponsored retirement plan. This includes understanding any restrictions on contributions or eligibility criteria for employer matches.

It’s important to remember that employer contributions are a valuable component of your retirement savings strategy. To fully maximize this benefit, stay informed about your plan’s details and take proactive steps to contribute enough to receive the maximum employer match. By doing so, you can significantly enhance your retirement savings while minimizing the impact on your current income.

Consider additional retirement savings options

While employer-sponsored retirement plans and individual retirement accounts (IRAs) are popular and effective ways to save for retirement, there are additional options available that can further enhance your savings. Consider these additional retirement savings options to diversify your portfolio and increase your retirement nest egg:

- Health Savings Accounts (HSAs): If you have a high-deductible health insurance plan, consider contributing to an HSA. HSAs offer triple tax advantages: contributions are tax-deductible, growth is tax-free, and qualified withdrawals for healthcare expenses are also tax-free. Unused funds can be rolled over and saved for future healthcare expenses in retirement.

- Taxable Investment Accounts: Taxable brokerage accounts provide flexibility and accessibility to your retirement savings. While contributions are made with after-tax dollars, you have the freedom to invest in a variety of assets. This could include stocks, bonds, mutual funds, or real estate investment trusts (REITs).

- Annuities: Annuities are insurance products that provide a steady income stream during retirement. They can be purchased with a lump sum or through regular contributions. Annuities offer various options, such as immediate or deferred annuities, fixed or variable rates, and lifetime income options.

- Real Estate Investments: Investing in rental properties or real estate investment trusts (REITs) can provide a consistent income stream in retirement. Real estate can be an attractive long-term investment option that can also offer potential tax advantages and hedge against inflation.

- Life Insurance Policies: Certain life insurance policies, such as whole or universal life insurance, can accumulate cash value over time. These policies allow you to borrow against the cash value or withdraw funds in retirement to supplement your income.

- Side Hustles and Passive Income: Consider generating additional income streams through side hustles or passive income sources. This could include freelancing, starting a small business, or investing in dividend-paying stocks. The extra income can be allocated towards retirement savings.

When considering additional retirement savings options, it’s important to weigh the risks, benefits, and tax implications associated with each option. Additionally, consult with a financial advisor to determine which strategies align with your financial goals and risk tolerance.

Remember, diversifying your retirement savings across different investment vehicles can help spread risk and potentially increase returns. However, it’s crucial to review and monitor your investments regularly to ensure they align with your retirement goals and adjust as needed over time.

Keep in mind that while additional retirement savings options can be beneficial, it’s important to prioritize contributions to tax-advantaged retirement accounts like IRAs and employer-sponsored plans, as they typically offer significant tax advantages and potential employer match opportunities.

Invest wisely

Investing wisely is a crucial aspect of retirement planning as it can significantly impact the growth and sustainability of your retirement savings. While investing always carries some level of risk, taking a strategic and informed approach can help you maximize returns while minimizing potential pitfalls. Here are some key principles to consider when investing for retirement:

- Asset Allocation: Determine the appropriate mix of asset classes, such as stocks, bonds, and cash, based on your risk tolerance, time horizon, and financial goals. A well-diversified portfolio can help mitigate risk and potentially enhance returns over the long term.

- Time in the Market: Take advantage of the power of compounding by staying invested for the long term. Trying to time the market or making frequent changes to your investments can lead to missed opportunities and lower overall returns.

- Understand Risk vs. Reward: Higher return potential typically comes with higher risk. It’s important to strike a balance between risk and reward that aligns with your investment goals and risk tolerance. Consider seeking professional advice to analyze and manage risk effectively.

- Invest in Low-Cost Index Funds or ETFs: Consider investing in low-cost, passively managed index funds or exchange-traded funds (ETFs). These investment vehicles offer broad market exposure and have historically outperformed actively managed funds after accounting for fees.

- Rebalance Regularly: Regularly review and rebalance your portfolio to maintain your desired asset allocation. This ensures that your investments align with your risk tolerance and long-term goals, especially as market conditions and asset values fluctuate.

- Take Advantage of Tax Efficiency: Be mindful of the tax implications of your investments. Consider utilizing tax-efficient investment strategies such as tax-efficient funds, tax-efficient asset location, or tax-loss harvesting to minimize the impact of taxes on your returns.

- Don’t Put All Your Eggs in One Basket: Diversify your investments across different sectors, industries, and geographic regions to spread risk and reduce the impact of any single investment. Avoid concentrating too much of your portfolio in one specific investment or asset class.

- Stay Informed: Continuously educate yourself about investing and stay updated on market trends, economic indicators, and changes in regulations. This empowers you to make informed investment decisions that align with your retirement objectives.

It’s important to note that investing carries inherent risks, and past performance is not indicative of future results. To make well-informed investment decisions, consider consulting with a financial advisor who can provide personalized guidance and ensure your investments align with your retirement goals.

Remember, investing wisely requires patience, discipline, and a long-term perspective. By following sound investment principles, you can increase the potential growth of your retirement savings and work towards achieving your desired financial security in retirement.

Review and adjust your retirement plan regularly

Creating a retirement plan is not a one-time task. To ensure that your plan remains effective and aligned with your goals, it’s crucial to regularly review and adjust it as needed. Life circumstances, market conditions, and personal priorities can change over time, requiring you to adapt your retirement strategy. Here are some important steps to follow:

- Monitor your progress: Regularly review your retirement savings to track your progress towards your goals. Compare your actual savings to your projected savings and make adjustments if necessary. Tools like retirement calculators or financial software can help you assess your financial trajectory.

- Assess your risk tolerance: As you progress closer to retirement, reassess your risk tolerance. Adjust your asset allocation to strike a balance between preserving your capital and generating enough returns to sustain your lifestyle throughout retirement.

- Revisit your retirement goals: Life circumstances and priorities can change over time. Review your retirement goals periodically. Are you still on track to meet them? Do you need to adjust your goals or timelines based on changes in your life or financial situation?

- Consider inflation: Account for inflation when assessing your retirement savings. Inflation erodes the purchasing power of your money over time. Ensure that your retirement plan factors in this cost-of-living increase and adjust your savings and investment strategies accordingly.

- Consult with professionals: Seek advice from financial advisors or retirement specialists. They can provide valuable insights, help you navigate complex financial decisions, and ensure that your plan aligns with your changing circumstances.

- Prepare for healthcare costs: Consider the potential impact of healthcare costs in retirement. Evaluate your health insurance coverage and explore options such as long-term care insurance or health savings accounts (HSAs) to mitigate the financial burden of medical expenses.

- Adjust contributions and savings: Regularly assess your cash flow and financial situation to determine if you can increase your contributions to retirement accounts. Allocating additional funds towards retirement savings, whenever possible, can help you catch up if you’ve fallen behind on your savings goals.

Life is dynamic, and your retirement plan should reflect that. By reviewing and adjusting your plan regularly, you can ensure that it remains relevant, responsive, and effective. Remember, it’s essential to be proactive when it comes to your retirement planning, as small adjustments along the way can have a significant impact on your overall financial well-being in retirement.

Conclusion

Retirement planning may seem like a distant and overwhelming task for young adults, but taking action early can pave the way for a financially secure and comfortable future. By implementing the strategies outlined in this article, you can set yourself up for a successful retirement journey:

- Start saving early to harness the power of compounding.

- Determine your retirement goals and create a plan to achieve them.

- Assess your current financial situation to understand where you stand.

- Create a budget to prioritize saving for retirement.

- Explore retirement account options and maximize your employer contributions.

- Consider additional retirement savings options to diversify your portfolio.

- Invest wisely by taking a long-term approach and understanding risk.

- Regularly review and adjust your retirement plan to stay on track.

Remember, retirement planning is not a one-time task but an ongoing process. As life evolves, make sure to revisit your retirement plan, update your goals, and adapt your strategies to align with your changing circumstances. Seek professional guidance when needed and stay informed about the latest trends and best practices in retirement planning.

By starting early, staying disciplined, and making informed decisions, you can build a solid financial foundation and achieve the retirement lifestyle you desire. So take charge of your financial future today and embark on the journey towards a rewarding and worry-free retirement!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance