Finance

What To Say On A Late Credit Inquiry

Published: March 5, 2024

Learn how to handle a late credit inquiry in your finance journey. Discover what to say and how to navigate the situation effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Navigating the world of credit inquiries can be a daunting task, especially when faced with the prospect of addressing a late credit inquiry. Whether you're applying for a loan, a credit card, or a mortgage, a late credit inquiry can have a significant impact on your credit score and financial standing. Understanding how to respond to a late credit inquiry is crucial for mitigating its potential negative effects.

Late credit inquiries occur when a lender or creditor pulls your credit report after a specified deadline. This can happen if there was a delay in processing your application or if the lender made an error in the timing of the inquiry. Regardless of the reason, a late credit inquiry can raise concerns for lenders and may lead to questions about your financial responsibility.

In this article, we'll delve into the intricacies of late credit inquiries, providing valuable insights into what they entail and offering practical tips for effectively addressing them. Additionally, we'll provide sample responses that you can use as a reference when communicating with lenders or creditors about late credit inquiries. By the end of this article, you'll be equipped with the knowledge and confidence to navigate the complexities of late credit inquiries and to communicate effectively with relevant parties.

Understanding the nuances of late credit inquiries and knowing how to respond to them can empower you to take control of your financial narrative and minimize any potential negative impact on your credit profile. Let's embark on this insightful journey to unravel the intricacies of late credit inquiries and equip ourselves with the tools to address them adeptly.

Understanding Late Credit Inquiries

When you apply for credit, whether it’s a credit card, auto loan, mortgage, or any other type of financing, the potential lender will likely pull your credit report to assess your creditworthiness. This process involves a credit inquiry, which is recorded on your credit report. A late credit inquiry occurs when this inquiry is made after a predetermined deadline, often established by the lender or creditor.

It’s important to note that credit inquiries are categorized into two types: hard inquiries and soft inquiries. Hard inquiries, which typically occur when you apply for credit, can impact your credit score and are visible to other parties who view your credit report. On the other hand, soft inquiries, such as those made by companies for pre-approved offers or by yourself for monitoring purposes, do not affect your credit score and are visible only to you.

When a credit inquiry is labeled as late, it can raise concerns for potential lenders. They may question why the inquiry was made after the stipulated deadline and whether there were underlying reasons for the delay. This can potentially cast doubt on your reliability in managing credit and meeting financial obligations.

It’s essential to recognize that late credit inquiries can stem from various scenarios, including administrative delays, technical issues, or miscalculations in the timing of the inquiry. While some late credit inquiries may be legitimate, others could be the result of errors or oversight on the part of the lender or creditor.

Understanding the implications of late credit inquiries is pivotal in safeguarding your credit standing. These inquiries can impact your credit score and, consequently, your ability to secure favorable terms on future credit applications. By comprehending the nuances of late credit inquiries, you can proactively address any issues that arise and strive to mitigate their potential adverse effects on your credit profile.

Now that we’ve delved into the essence of late credit inquiries, let’s explore actionable tips for effectively responding to them, empowering you to navigate these situations with confidence and proficiency.

Tips for Responding to Late Credit Inquiries

Responding to a late credit inquiry necessitates a strategic and informed approach to effectively address the situation. Consider the following tips to navigate this process with confidence:

- Review Your Records: Before responding to a late credit inquiry, carefully review your records to ascertain the timeline of your credit application and any communications with the lender. Understanding the sequence of events can provide valuable insights into the circumstances surrounding the late inquiry.

- Communicate Promptly: Upon discovering a late credit inquiry, promptly reach out to the lender or creditor to initiate a dialogue. Clear and timely communication can demonstrate your proactive approach in addressing the issue and convey your commitment to resolving any discrepancies.

- Provide Documentation: If you possess documentation, such as application submission confirmations or correspondence with the lender, that supports the timeline of your credit application, be prepared to present these materials. Tangible evidence can substantiate your claims and bolster your position.

- Remain Courteous and Professional: When communicating with the lender or creditor, maintain a courteous and professional demeanor. Despite the urgency of rectifying the late inquiry, approaching the situation with professionalism can foster constructive dialogue and facilitate a mutually beneficial resolution.

- Seek Clarification: If the late credit inquiry resulted from an error or misunderstanding, seek clarification from the lender regarding the circumstances that led to the delay. Understanding the underlying reasons can enable you to address any misconceptions and work towards a resolution.

- Request Correction if Applicable: If the late credit inquiry was indeed an error on the part of the lender or creditor, respectfully request that they rectify the situation. Emphasize the importance of an accurate credit report and the potential impact of the late inquiry on your credit standing.

- Monitor Your Credit Report: Following the resolution of the late credit inquiry, diligently monitor your credit report to ensure that any inaccuracies are corrected. Regularly reviewing your credit report can help you promptly identify and address any discrepancies that may arise.

By adhering to these tips, you can approach the process of responding to late credit inquiries proactively and effectively. Navigating this situation with attentiveness and professionalism can contribute to safeguarding your credit integrity and fostering positive relationships with lenders and creditors.

Sample Responses for Late Credit Inquiries

When crafting a response to address a late credit inquiry, it’s essential to convey clarity, professionalism, and a proactive stance. Below are sample responses that can serve as templates for communicating with lenders or creditors regarding late credit inquiries:

- Sample Response 1:

- Sample Response 2:

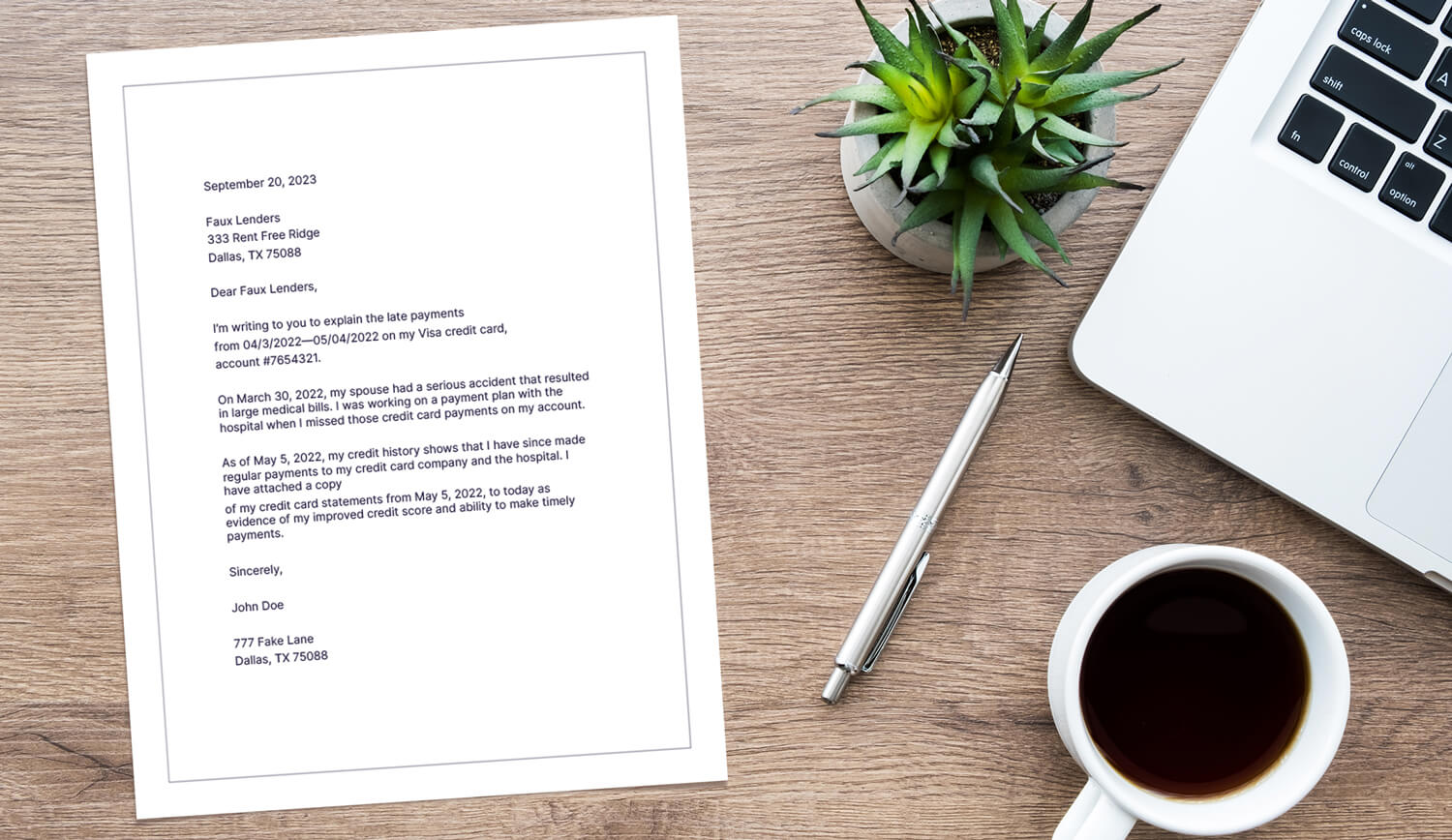

Dear [Lender/Creditor’s Name],

I recently became aware of a late credit inquiry associated with my credit application. Upon reviewing the timeline of my application process, I noticed that the inquiry was conducted after the specified deadline. I value transparency and accountability, and I am committed to addressing this matter promptly.

Enclosed with this correspondence are documents that outline the submission of my credit application and subsequent interactions with your institution. I believe that these materials will provide clarity regarding the sequence of events and the circumstances surrounding the late credit inquiry.

I am eager to engage in constructive dialogue to rectify this situation and ensure the accuracy of my credit report. Your prompt attention to this matter is greatly appreciated, and I am confident that we can work together to resolve this issue amicably.

Thank you for your attention to this important matter, and I look forward to your timely response.

Sincerely,

[Your Name]

Dear [Lender/Creditor’s Name],

I recently discovered a late credit inquiry associated with my credit application, and I am reaching out to address this matter proactively. I understand the significance of accurate credit reporting and am committed to ensuring the integrity of my credit profile.

Given the implications of a late credit inquiry, I have meticulously reviewed the timeline of my credit application process and have compiled supporting documentation that elucidates the sequence of events. I believe that this documentation will provide valuable context and assist in resolving any discrepancies pertaining to the timing of the credit inquiry.

I value the opportunity to collaborate with you in rectifying this situation and am open to providing any additional information that may facilitate a swift resolution. Your attention to this matter is crucial, and I am eager to work towards a mutually beneficial outcome.

Thank you for your prompt consideration, and I anticipate a constructive dialogue to address this issue effectively.

Warm regards,

[Your Name]

These sample responses exemplify a proactive and professional approach to addressing late credit inquiries. By customizing these templates to align with the specifics of your situation, you can effectively communicate with lenders or creditors and work towards a resolution that upholds the accuracy of your credit report.

Conclusion

Navigating the realm of late credit inquiries requires attentiveness, clear communication, and a proactive mindset. By understanding the implications of late credit inquiries and familiarizing yourself with effective response strategies, you can confidently address these situations and safeguard the integrity of your credit profile.

When confronted with a late credit inquiry, it’s crucial to approach the matter with diligence and professionalism. Reviewing your records, promptly initiating communication with the relevant parties, and providing supporting documentation are pivotal steps in addressing late credit inquiries. By seeking clarification, requesting corrections if applicable, and maintaining courteous dialogue, you can work towards resolving these issues and mitigating any potential impact on your credit standing.

Furthermore, the sample responses provided in this article serve as valuable templates for crafting your own communications with lenders or creditors regarding late credit inquiries. Customizing these responses to align with the specifics of your situation can help you convey transparency, accountability, and a proactive stance in addressing late credit inquiries effectively.

Ultimately, proactively addressing late credit inquiries contributes to upholding the accuracy of your credit report and fortifying your financial credibility. By adhering to the insights and strategies outlined in this article, you can navigate the complexities of late credit inquiries with confidence and advocate for the integrity of your credit profile.

Empowered with the knowledge and tools to respond adeptly to late credit inquiries, you are well-equipped to engage in constructive dialogue with lenders and creditors, thereby fostering positive relationships and maintaining a strong financial standing.

As you embark on your journey to address late credit inquiries, remember that attentiveness, professionalism, and proactive communication are instrumental in navigating these situations effectively. By leveraging the guidance provided in this article, you can navigate late credit inquiries with poise and advocate for the accuracy and integrity of your credit profile.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance