Finance

Why Cant I Get A Debt Consolidation Loan

Published: March 6, 2024

Learn why you're struggling to secure a debt consolidation loan and get expert advice on improving your financial situation. Explore finance options today.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

**

Introduction

**

Debt consolidation loans are often seen as a beacon of hope for individuals struggling to manage multiple debts. The concept is simple yet powerful: take out a new loan to pay off existing debts, leaving you with a single, more manageable monthly payment. However, the process of obtaining a debt consolidation loan can be challenging, and many individuals find themselves asking, “Why can’t I get a debt consolidation loan?”

Understanding the nuances of debt consolidation loans and the factors that affect approval is crucial for anyone considering this financial solution. From credit scores and income levels to the types of debt being consolidated, various elements come into play when lenders assess an individual’s eligibility for a debt consolidation loan. This article aims to shed light on the complexities of this process and provide valuable insights into improving one’s chances of securing a debt consolidation loan.

By delving into the intricacies of debt consolidation loans and exploring alternative options, readers will gain a comprehensive understanding of how to navigate their financial challenges effectively. Whether you’re currently grappling with overwhelming debt or simply seeking to expand your financial knowledge, this article will equip you with the information needed to make informed decisions regarding debt consolidation and its alternatives.

Understanding Debt Consolidation Loans

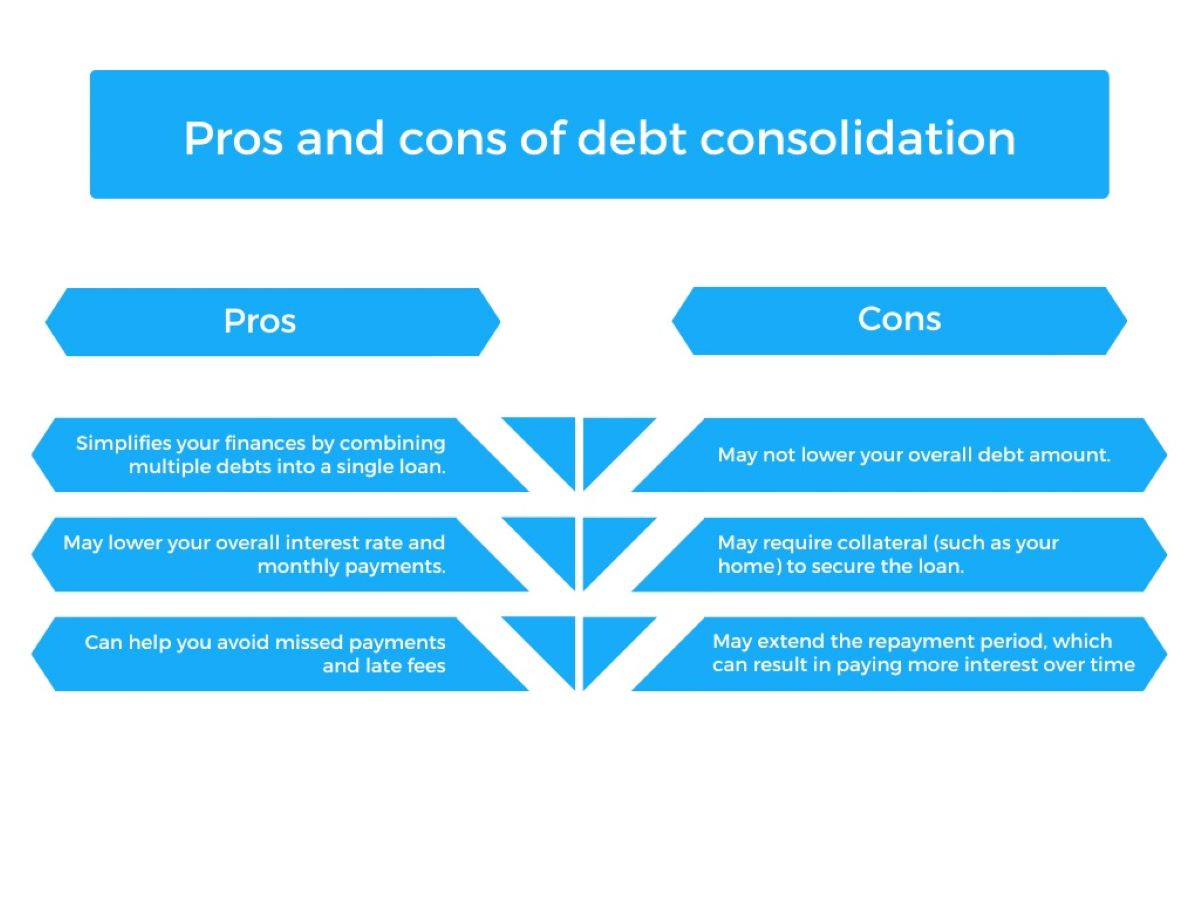

Debt consolidation loans serve as a powerful tool for simplifying debt management by combining multiple debts into a single loan with a fixed interest rate and a structured repayment plan. By doing so, borrowers can streamline their finances, potentially reduce their overall interest payments, and gain a clearer perspective on their debt obligations.

These loans are commonly used to consolidate credit card balances, medical bills, personal loans, and other unsecured debts. By opting for a debt consolidation loan, individuals can replace high-interest debts with a more manageable, single monthly payment. This not only eases the burden of tracking multiple payment due dates but also provides the opportunity to save on interest charges over time.

It’s important to note that debt consolidation loans do not eliminate debt; rather, they restructure it in a more organized and manageable manner. By understanding the mechanics of debt consolidation loans, individuals can make informed decisions about whether this option aligns with their financial goals and circumstances.

Furthermore, comprehending the potential benefits and drawbacks of debt consolidation loans is essential for individuals seeking to improve their financial well-being. While these loans can simplify repayment and potentially lower interest costs, they may not be suitable for everyone. Factors such as credit score, income stability, and the total amount of debt being consolidated play pivotal roles in determining eligibility and the terms of the loan.

By gaining a deeper understanding of how debt consolidation loans work and the impact they can have on one’s financial situation, individuals can make informed decisions about pursuing this option or exploring alternative paths to debt relief.

Factors That Affect Approval

When applying for a debt consolidation loan, numerous factors come into play, influencing the likelihood of approval and the terms offered by lenders. Understanding these key determinants is essential for individuals seeking to improve their eligibility and secure favorable loan terms.

- Credit Score: One of the most significant factors impacting loan approval is the applicant’s credit score. Lenders use this metric to assess an individual’s creditworthiness and likelihood of repaying the loan. A higher credit score typically increases the chances of approval and may result in more favorable interest rates.

- Income and Employment Stability: Lenders evaluate an applicant’s income level and employment history to gauge their ability to repay the loan. A stable income and steady employment demonstrate financial reliability, potentially bolstering the likelihood of loan approval.

- Total Debt and Debt-to-Income Ratio: The total amount of existing debt and the ratio of debt to income are critical considerations for lenders. Individuals with high levels of existing debt or a high debt-to-income ratio may encounter challenges in securing a debt consolidation loan.

- Collateral: Some debt consolidation loans are secured by collateral, such as a home or vehicle. The presence of collateral can impact approval, as it provides lenders with a form of security in the event of default.

- Payment History: A history of timely payments on existing debts reflects positively on an applicant’s financial responsibility. Conversely, late payments or delinquencies may raise concerns for lenders.

By recognizing the significance of these factors, individuals can take proactive steps to strengthen their financial position and improve their chances of obtaining a debt consolidation loan. This may involve addressing credit issues, enhancing income stability, or exploring alternative forms of collateral to support the loan application.

Moreover, individuals should be mindful of the impact of loan inquiries on their credit score. Multiple loan applications within a short timeframe can lower a credit score, potentially diminishing the chances of approval. Therefore, it’s advisable to research and target lenders whose eligibility criteria align with one’s financial profile before submitting loan applications.

By proactively addressing the factors that influence loan approval, individuals can enhance their eligibility and position themselves for more favorable debt consolidation loan terms.

Steps to Improve Your Eligibility

Improving eligibility for a debt consolidation loan involves a strategic approach to address the key factors that influence lender decisions. By taking proactive steps to enhance one’s financial standing, individuals can bolster their chances of securing a favorable loan and achieving effective debt consolidation.

- Enhance Credit Score: Prioritize efforts to improve and maintain a healthy credit score. This includes making timely payments, reducing outstanding balances, and addressing any errors on credit reports. By demonstrating responsible credit management, individuals can enhance their creditworthiness and increase the likelihood of loan approval.

- Stabilize Income: Lenders value stable income sources, as they provide assurance of an applicant’s ability to meet repayment obligations. Individuals can work towards enhancing their income stability by seeking additional sources of income, pursuing career advancement opportunities, or securing long-term employment.

- Reduce Debt Load: Taking proactive measures to reduce existing debt can positively impact one’s debt-to-income ratio and overall financial health. Implementing a focused debt repayment strategy, prioritizing high-interest debts, and exploring budget optimization techniques can contribute to a more favorable debt profile.

- Explore Collateral Options: For individuals considering secured debt consolidation loans, evaluating available collateral options is crucial. This may involve assessing the equity in real estate, vehicles, or other valuable assets that can be leveraged to strengthen the loan application.

- Research Lenders: Conduct thorough research to identify lenders whose eligibility criteria align with your financial profile. By targeting lenders that specialize in catering to individuals with specific credit scores or financial circumstances, you can increase the likelihood of finding a suitable loan offer.

Additionally, seeking financial counseling or guidance from reputable credit counseling agencies can provide valuable insights and personalized strategies for improving eligibility for a debt consolidation loan. These professionals can offer tailored advice on debt management, credit improvement, and the most effective paths to achieving debt relief.

By diligently addressing these steps and focusing on enhancing key eligibility factors, individuals can position themselves for a successful debt consolidation loan application, paving the way for improved financial stability and more manageable debt repayment.

Alternatives to Debt Consolidation Loans

While debt consolidation loans offer a structured approach to managing multiple debts, several alternative strategies can provide relief for individuals facing financial challenges. Exploring these alternatives allows individuals to consider a diverse range of options tailored to their specific circumstances and preferences.

- Debt Management Plans: Enrolling in a debt management plan through a reputable credit counseling agency can provide a structured pathway to debt repayment. These plans often involve negotiating reduced interest rates and monthly payments with creditors, enabling individuals to consolidate their debts without taking out a new loan.

- Balance Transfer Credit Cards: For individuals grappling with high-interest credit card debt, transferring balances to a credit card with a lower promotional interest rate can offer temporary relief. While this approach consolidates debts onto a single card, it’s crucial to assess the long-term implications and potential fees associated with balance transfers.

- Home Equity Loans or Lines of Credit: Homeowners may explore the option of leveraging their home equity to consolidate debts through a loan or line of credit. By using their home as collateral, individuals can access funds at potentially lower interest rates. However, this approach carries the risk of placing the home at stake if repayment obligations are not met.

- Debt Settlement: Individuals facing significant financial hardship may consider debt settlement, wherein creditors agree to accept less than the full amount owed to satisfy the debt. While debt settlement can lead to reduced overall debt balances, it may have adverse effects on credit scores and require careful consideration of potential tax implications.

- Personal Budgeting and Negotiation: Implementing a comprehensive personal budget and directly negotiating with creditors to establish modified repayment terms can be effective in managing debts without external consolidation. This approach requires discipline and proactive communication with creditors to reach mutually beneficial arrangements.

Each alternative presents unique considerations and potential implications, underscoring the importance of thorough research and careful assessment of individual financial circumstances. Furthermore, seeking guidance from financial professionals, such as credit counselors and financial advisors, can provide invaluable insights into the most suitable approach for achieving debt relief.

By evaluating these alternatives alongside debt consolidation loans, individuals can make informed decisions aligned with their financial goals and preferences, ultimately paving the way for effective debt management and long-term financial stability.

Conclusion

Navigating the complexities of debt consolidation loans and exploring alternative paths to debt relief is a pivotal journey for individuals seeking to regain control of their financial well-being. Understanding the factors that influence loan approval, along with the steps to enhance eligibility, empowers individuals to make informed decisions tailored to their unique circumstances.

While debt consolidation loans offer a structured approach to streamlining debt repayment, individuals should carefully assess alternative strategies such as debt management plans, balance transfer credit cards, home equity options, debt settlement, and personalized budgeting and negotiation. Each alternative presents distinct advantages and considerations, highlighting the significance of comprehensive research and personalized financial guidance.

By embracing proactive measures to improve credit scores, stabilize income, and reduce debt burdens, individuals can strengthen their eligibility for debt consolidation loans and alternative debt relief avenues. Moreover, seeking guidance from reputable financial professionals can provide tailored strategies and insights to navigate the path toward financial stability.

Ultimately, the journey toward effective debt management and long-term financial well-being requires a holistic approach that considers individual goals, financial circumstances, and risk tolerance. By leveraging a combination of informed decision-making, proactive financial management, and strategic debt relief strategies, individuals can pave the way for a brighter financial future and enhanced peace of mind.

Whether pursuing a debt consolidation loan or exploring alternative avenues, individuals are encouraged to approach their financial challenges with diligence, resilience, and a commitment to achieving sustainable debt relief. By doing so, they can embark on a transformative journey toward financial empowerment and a renewed sense of control over their economic destiny.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance