Home>Finance>Whole Life Insurance Definition: How It Works, With Examples

Finance

Whole Life Insurance Definition: How It Works, With Examples

Published: February 18, 2024

Learn about whole life insurance and how it works in the world of finance, including examples and insights.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

What is Whole Life Insurance?

When it comes to securing your financial future, whole life insurance can play a crucial role. It is a type of life insurance policy that provides coverage for the entire lifetime of the insured person, as long as the premiums are paid on time. Unlike term life insurance, which only covers a specific period, whole life insurance offers lifelong protection and can provide a range of benefits to policyholders and their beneficiaries.

Key Takeaways:

- Whole life insurance is a type of policy that provides coverage for the entire lifetime of the insured.

- Premiums for whole life insurance are typically higher than term life insurance but offer additional benefits.

Now that we’ve defined what whole life insurance is, let’s take a closer look at how it works and the advantages it offers.

How Does Whole Life Insurance Work?

Whole life insurance works by combining a death benefit with a cash value component. Here are the main aspects of how this type of policy functions:

- Premium payments: To keep the policy active, you need to pay regular premiums for the duration of your life or a set period, depending on the policy’s terms.

- Death benefit: In the event of your death, the insurance company pays a lump sum, known as the death benefit, to your designated beneficiaries. This amount can help cover funeral expenses, outstanding debts, or provide financial support to your loved ones.

- Cash value accumulation: A portion of the premium you pay goes towards building cash value within the policy. This cash value grows over time, often on a tax-deferred basis. You can borrow against this accumulated cash value or even withdraw it, providing you with a flexible financial resource.

Whole life insurance policies also offer a range of additional benefits, including:

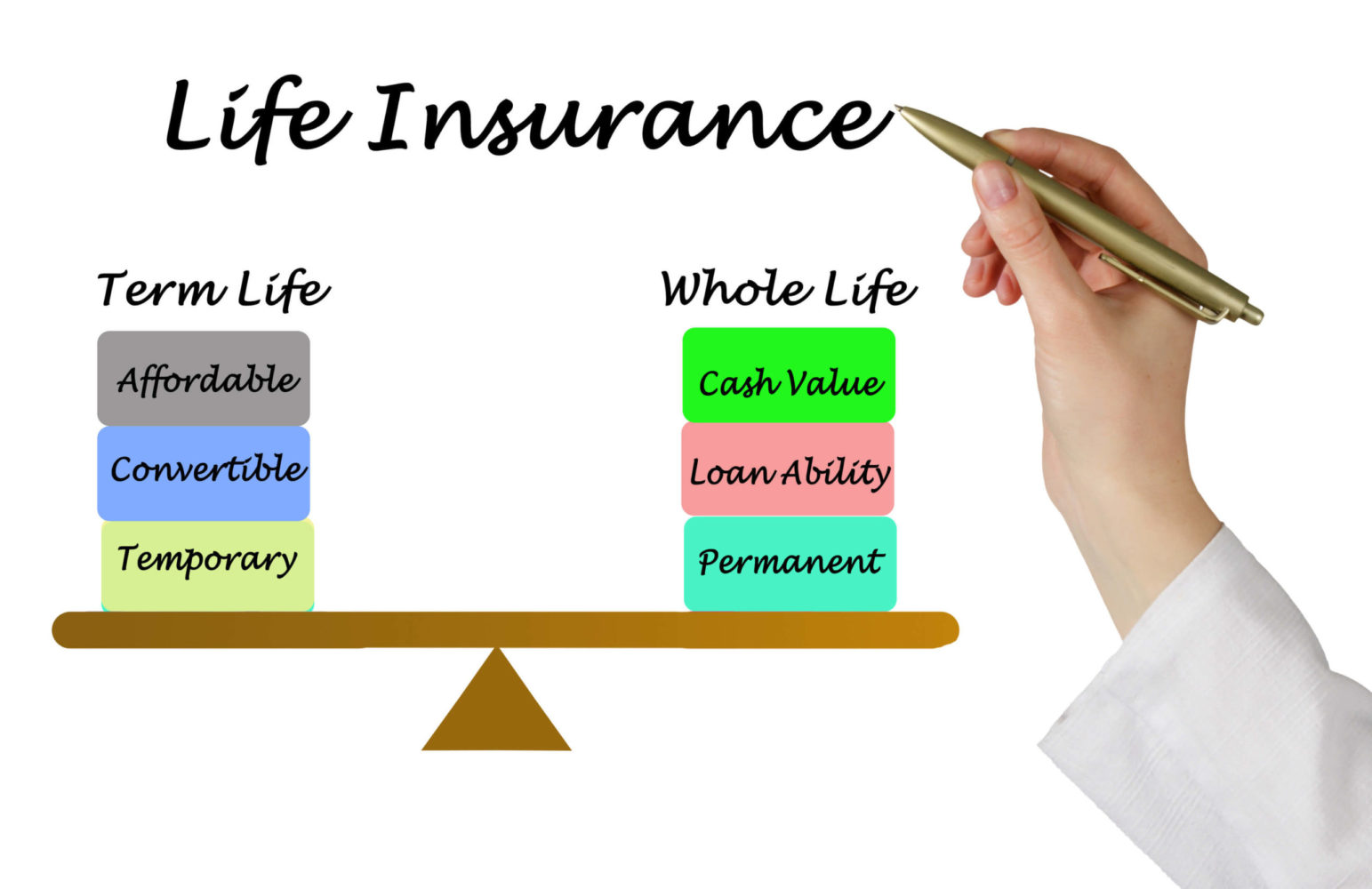

- Stable premiums: Unlike term life insurance, which typically increases in cost as you get older, whole life insurance premiums remain steady throughout your lifetime. This can provide stability and predictability when it comes to financial planning.

- Lifetime coverage: Whether you pass away at 40 or 90, your whole life insurance policy will pay out a death benefit to your beneficiaries, as long as you’ve paid the required premiums.

- Tax advantages: The cash value growth within a whole life insurance policy is tax-deferred, meaning you won’t pay taxes on the growth until you withdraw it. Additionally, the death benefit is typically tax-free to the beneficiary, providing a valuable source of tax-advantaged wealth transfer.

Examples of Whole Life Insurance

Let’s take a look at two hypothetical examples that illustrate how whole life insurance can work:

Example 1: Sarah, a 35-year-old mother of two, purchases a whole life insurance policy with a $500,000 death benefit. She pays premiums of $300 per month for the entire duration of her life. When Sarah passes away at age 75, her beneficiaries receive the $500,000 death benefit, which they can use to cover any outstanding debts, funeral costs, or provide financial security for the family.

Example 2: John, a 45-year-old individual, wants to ensure his family’s financial stability. He buys a whole life insurance policy for $250,000 and pays $500 per month until he turns 65. At that point, John can access the accumulated cash value, which has grown over the years, to supplement his retirement income or fund his grandchildren’s education.

In Conclusion

Whole life insurance is a comprehensive financial tool that combines lifelong coverage with a cash value component. Whether you’re looking to protect your loved ones in case of your untimely passing or build a financial resource to supplement your retirement, whole life insurance provides a range of benefits to suit various personal and financial goals. Take the time to assess your needs and consult with a financial advisor to determine if whole life insurance is right for you.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance