Finance

How To Use Whole Life Insurance As A Bank

Published: November 17, 2023

Learn how to leverage whole life insurance to grow your finances and use it as a reliable banking tool for long-term financial stability. Discover the benefits and strategies today.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- What is Whole Life Insurance?

- The Concept of Using Whole Life Insurance as a Bank

- Benefits of Using Whole Life Insurance as a Bank

- Process of Using Whole Life Insurance as a Bank

- Considerations Before Using Whole Life Insurance as a Bank

- Potential Risks of Using Whole Life Insurance as a Bank

- Conclusion

Introduction

When it comes to managing our finances, we are often on the lookout for innovative ways to make the most of our money. One such approach that has gained popularity in recent years is using whole life insurance as a bank.

Whole life insurance is a type of permanent life insurance that provides coverage for your entire life as long as the premiums are paid. It offers not only a death benefit to your beneficiaries but also an opportunity for cash value accumulation over time.

The concept of using whole life insurance as a bank is based on leveraging the cash value component of the policy. Instead of relying solely on traditional banks for loans, individuals can borrow against the cash value of their insurance policies.

This innovative strategy provides a wide range of benefits, including the potential for tax advantages, flexible loan terms, and the ability to earn dividends on the cash value. However, it is important to consider the potential risks and understand the process before utilizing whole life insurance as a bank.

In this article, we will delve deeper into the concept of using whole life insurance as a bank and explore its benefits, the process involved, and the considerations one should take into account before opting for this financial strategy. By understanding the intricacies of this approach, you can make an informed decision about whether or not it is a suitable option for you.

What is Whole Life Insurance?

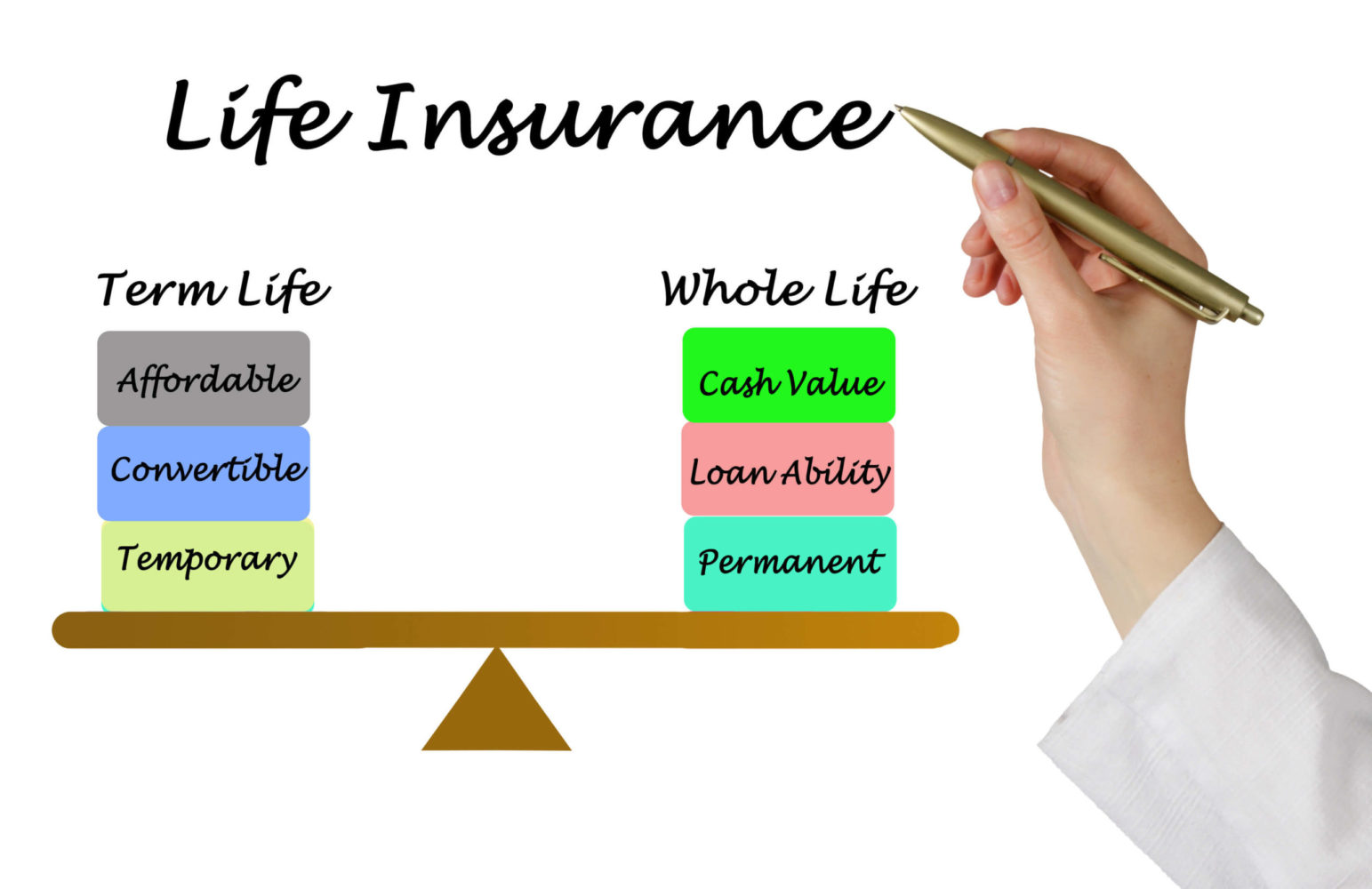

Whole life insurance is a form of permanent life insurance that provides coverage for the entire duration of your life, as long as you continue paying the premiums. Unlike term life insurance, which only provides coverage for a specific period, whole life insurance offers lifelong protection.

One of the key features of whole life insurance is the accumulation of cash value. A portion of the premium payments made towards the policy is allocated to a cash value account, which grows over time. This cash value can be accessed through policy loans or withdrawals.

With whole life insurance, the premiums are typically higher compared to term life insurance. However, this higher cost is offset by the benefits it offers. Apart from providing a death benefit to your beneficiaries, whole life insurance also serves as a long-term savings vehicle.

Unlike other types of investments, the cash value of a whole life insurance policy grows on a tax-deferred basis. This means that the growth is not subject to income taxes. Additionally, some whole life insurance policies may pay dividends, further increasing the cash value of the policy.

Whole life insurance offers financial security and peace of mind, as it ensures that your loved ones are taken care of in the event of your passing. It also provides you with the opportunity to accumulate wealth over time and access funds when needed.

It is important to note that whole life insurance is a long-term commitment. Canceling the policy prematurely or surrendering it can lead to financial consequences, so it is advisable to carefully review the terms and conditions of the policy before purchasing.

Now that we have a basic understanding of what whole life insurance is, let’s explore the concept of using it as a bank and how it can benefit you financially.

The Concept of Using Whole Life Insurance as a Bank

The concept of using whole life insurance as a bank revolves around leveraging the cash value component of the policy to meet financial needs. Instead of relying solely on traditional banks for loans, individuals can borrow against the cash value of their insurance policies.

When you pay premiums into a whole life insurance policy, a portion of those payments goes toward building the cash value. Over time, this cash value grows through the accumulation of interest and potential dividends. This accumulated cash value can serve as collateral when borrowing against the policy.

By using whole life insurance as a bank, individuals can enjoy several advantages. Firstly, the process of obtaining a loan against the cash value is typically more streamlined and straightforward compared to traditional bank loans. It can be a quicker and more convenient option for addressing financial needs.

Secondly, since the loan is secured by the cash value of the policy, the interest rates are often lower than those charged by banks for unsecured loans. This can result in significant savings on interest payments over the life of the loan.

Another benefit of using whole life insurance as a bank is the flexibility it offers. Borrowers have the freedom to determine the loan terms, including the repayment period, interest rate, and repayment schedule. This flexibility allows individuals to tailor the loan to their specific financial circumstances and goals.

In addition, borrowing against the cash value of a whole life insurance policy does not require a credit check or affect your credit score. This can be advantageous if you have less-than-perfect credit or want to preserve your credit rating.

It’s important to note that when borrowing against the cash value of a whole life insurance policy, the amount borrowed reduces the overall death benefit. However, if the loan is repaid, the death benefit is reinstated to its original amount.

Overall, the concept of using whole life insurance as a bank provides an alternative avenue for accessing funds when needed. It offers convenience, flexibility, and potentially lower interest rates compared to traditional financing options. However, it is crucial to understand the process and consider the associated risks and considerations before utilizing this strategy.

Benefits of Using Whole Life Insurance as a Bank

Using whole life insurance as a bank can provide several benefits for individuals seeking financial flexibility and access to funds. Let’s explore some of the key advantages of utilizing this unconventional strategy:

1. Convenient access to funds: Borrowing against the cash value of a whole life insurance policy allows for a straightforward and hassle-free process. Unlike traditional bank loans, which often involve extensive paperwork and approval procedures, accessing funds from your policy can be quick and convenient.

2. Lower interest rates: Loans against the cash value of a whole life insurance policy tend to have lower interest rates compared to other forms of borrowing. This is because the loan is secured by the cash value of the policy, reducing the risk for the lender. Lower interest rates can result in significant savings over the life of the loan.

3. Flexibility in loan terms: Borrowers have the freedom to customize their loan terms, including repayment period, interest rate, and repayment schedule. This flexibility allows individuals to tailor the loan to their specific financial needs and goals, providing greater control over their financial situation.

4. Preservation of credit rating: When borrowing against the cash value of a whole life insurance policy, there is no credit check required, and it does not impact your credit score. This can be advantageous for individuals with less-than-perfect credit or those who want to maintain their credit rating for other purposes.

5. Tax advantages: The cash value accumulation within a whole life insurance policy grows on a tax-deferred basis. This means that the growth is not subject to income tax. Additionally, policyholders may be eligible to receive tax-free withdrawals up to the amount of their premiums paid. These tax advantages can provide significant savings over the long term.

6. Death benefit preservation: While borrowing against the cash value of a whole life insurance policy reduces the death benefit, once the loan is repaid, the death benefit is reinstated to its original amount. This ensures that the financial protection provided to your beneficiaries remains intact.

7. Potential for policy dividends: Some whole life insurance policies may pay dividends based on the performance of the insurance company. These dividends can be used to enhance the cash value of the policy, further increasing the funds available for borrowing or potential growth.

Utilizing whole life insurance as a bank offers a unique set of benefits that can provide individuals with greater financial flexibility, lower borrowing costs, and potential tax advantages. However, it’s important to consider the process involved in borrowing against the cash value and the potential risks before making a decision.

Process of Using Whole Life Insurance as a Bank

The process of using whole life insurance as a bank involves borrowing against the cash value of the policy to meet financial needs. Here is a step-by-step guide to help you understand the process:

1. Determine your financial needs: Assess your financial situation and determine how much funding you require. Be clear about your financial goals and how the borrowed funds will be utilized. This will help you determine the amount you want to borrow from your whole life insurance policy.

2. Review your policy details: Carefully review your whole life insurance policy to understand the terms and conditions, including the cash value, surrender charges, policy loans provision, and any potential impact on the death benefit. It’s crucial to have a clear understanding of how borrowing against the policy will affect your coverage.

3. Contact your insurance company: Get in touch with your insurance company and inform them of your intention to borrow against the cash value of your policy. They will guide you through the process and provide you with all the necessary forms and paperwork required to initiate the loan request.

4. Complete the loan application: Fill out the loan application form provided by your insurance company. You may need to provide personal information, policy details, the loan amount requested, and any additional documentation required by the insurer.

5. Evaluate loan terms: Once your loan application is submitted, the insurance company will review your request and determine the loan terms. This includes the interest rate, repayment period, and any other applicable charges or fees. Review these terms carefully to ensure they align with your financial goals.

6. Loan approval and disbursement: If your loan application is approved, the insurance company will disburse the funds to you. The loan amount will typically be a percentage of the cash value of your policy, which can vary depending on the insurance company and the specifics of your policy.

7. Repayment of the loan: Develop a repayment plan to ensure you can repay the loan within the agreed-upon terms. Make regular payments on time to avoid any potential negative consequences, such as the accumulation of interest or the reduction of the death benefit.

8. Monitoring your policy: As you repay the loan, monitor the impact on your policy’s cash value and death benefit. Keep track of the loan balance and ensure that your policy remains active and in good standing.

It’s crucial to note that the process of using whole life insurance as a bank may vary slightly depending on the specific insurance company and the terms of your policy. Consulting with your insurance company and seeking professional financial advice can provide greater clarity and guidance throughout the process.

Considerations Before Using Whole Life Insurance as a Bank

While utilizing whole life insurance as a bank can offer various financial benefits, it is essential to carefully consider certain factors before pursuing this strategy. Here are some key considerations to keep in mind:

1. Impact on policy’s cash value and death benefit: Borrowing against the cash value of your whole life insurance policy will reduce the available cash value, and in turn, the death benefit. It’s important to assess the impact on your policy’s protection and evaluate if the borrowed funds outweigh the potential loss of coverage for your loved ones.

2. Loan repayment obligations: Before taking a loan against your policy, consider your ability to repay the loan within the agreed-upon terms. Failure to make loan payments can result in interest accumulation, potential policy lapses, or the need to surrender the policy, which could lead to financial consequences.

3. Surrender charges and fees: Some whole life insurance policies may have surrender charges or fees associated with borrowing against the cash value. Review your policy documents to understand any potential costs involved before proceeding.

4. Opportunity cost of cash value: The cash value of a whole life insurance policy has the potential to grow over time. By borrowing against the cash value, you may miss out on potential growth and dividend earnings. Evaluate the potential opportunity cost and compare it with alternative investment options available to you.

5. Alternative borrowing options: Consider other borrowing options available to you, such as traditional banks, credit unions, or personal loans. Compare the terms, interest rates, and repayment conditions to determine the most suitable option for your financial needs.

6. Tax implications: While the cash value of a whole life insurance policy grows tax-deferred, policy loans are not considered taxable income. However, there could be tax consequences if the policy lapses or is surrendered. Consult with a tax professional to fully understand the potential tax implications of borrowing against your policy.

7. Overall financial goals and priorities: Assess your broader financial goals and priorities before using whole life insurance as a bank. Consider whether borrowing against your policy aligns with your long-term financial plan and supports your overall financial objectives.

It is recommended to consult with a financial advisor or insurance professional who can provide personalized guidance tailored to your specific circumstances. They can help you navigate the intricacies of using whole life insurance as a bank and evaluate whether this strategy is suitable for your financial needs and goals.

Potential Risks of Using Whole Life Insurance as a Bank

While using whole life insurance as a bank can offer several benefits, it is crucial to understand and evaluate the potential risks associated with this financial strategy. Here are some key risks to consider:

1. Reduction in death benefit: Borrowing against the cash value of a whole life insurance policy will result in a reduction of the death benefit. This means that if you were to pass away while the loan is outstanding, the payout to your beneficiaries would be lower than it would have been without the loan.

2. Impact on policy performance: The cash value of a whole life insurance policy plays a vital role in providing potential growth and earning dividends. Borrowing against the cash value can impede the policy’s performance and limit the accumulation of funds over time.

3. Risk of policy lapsing: Failing to repay the loan within the agreed-upon terms can lead to policy lapses. A policy lapse means losing the coverage and potential cash value, and it may require additional payments or reinstatement fees to reinstate the policy later on.

4. Accumulation of interest: If loan repayments are not made promptly and in full, it can lead to the accumulation of interest on the outstanding loan balance. This can increase the total amount owed and put additional financial pressure on the policyholder.

5. Surrender charges and fees: Some whole life insurance policies may impose surrender charges or fees when borrowing against the cash value. These fees can diminish the amount of money available for borrowing and impact the overall financial benefits of using the policy as a bank.

6. Disruption of long-term financial plans: Using whole life insurance as a bank can disrupt long-term financial plans and goals. It is important to consider the potential impact on other financial objectives, such as retirement planning or education savings, before borrowing against the policy.

7. Tax implications: While policy loans themselves are not considered taxable income, there could be tax consequences if the policy lapses, is surrendered, or becomes a modified endowment contract (MEC). Consult with a tax professional to understand the potential tax implications specific to your situation.

Understanding these potential risks is crucial in making an informed decision about utilizing whole life insurance as a bank. It is advisable to consult with a financial advisor or insurance professional who can help assess your specific circumstances, evaluate the risks, and provide guidance on whether this strategy aligns with your long-term financial goals.

Conclusion

Using whole life insurance as a bank can be an attractive option for those seeking financial flexibility and access to funds. It allows individuals to leverage the cash value of their insurance policies to meet their financial needs, offering convenience, lower interest rates, and potential tax advantages.

However, before deciding to use whole life insurance as a bank, it is important to carefully consider the potential risks and implications. Borrowing against the cash value can result in a reduction in the death benefit, impact the policy’s performance, and carry the risk of policy lapses or the accumulation of interest.

It is crucial to thoroughly review your policy details, understand the terms and conditions, and assess how borrowing against the policy will align with your broader financial goals. Consulting with a financial advisor or insurance professional can provide personalized guidance and help you make an informed decision.

Remember that using whole life insurance as a bank is not suitable for everyone. It requires careful planning, commitment to loan repayment, and an understanding of the potential consequences. Assess your financial situation, alternative borrowing options, and consider the long-term impact on your policy and other financial objectives.

While utilizing whole life insurance as a bank can offer benefits such as convenient access to funds, lower interest rates, and potential tax advantages, it is essential to weigh these benefits against the potential risks and costs associated with this strategy.

By considering all these factors and seeking professional advice, you can make an informed decision about whether using whole life insurance as a bank is the right choice for your financial needs and goals.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance