Finance

How To Get Student Loans Off My Credit Report

Published: January 19, 2024

Learn how to remove student loans from your credit report and improve your finance with our step-by-step guide. Take control of your financial future today!

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding the Impact of Student Loans on Credit Reports

- Steps to Remove Student Loans from Your Credit Report

- Step 1: Review Your Credit Reports

- Step 2: Check for Errors and Inaccuracies

- Step 3: Dispute Inaccurate Information with Credit Bureaus

- Step 4: Provide Documentation to Support Your Dispute

- Step 5: Follow Up with Credit Bureaus and Loan Servicers

- Step 6: Utilize Good Credit Practices

- Conclusion

Introduction

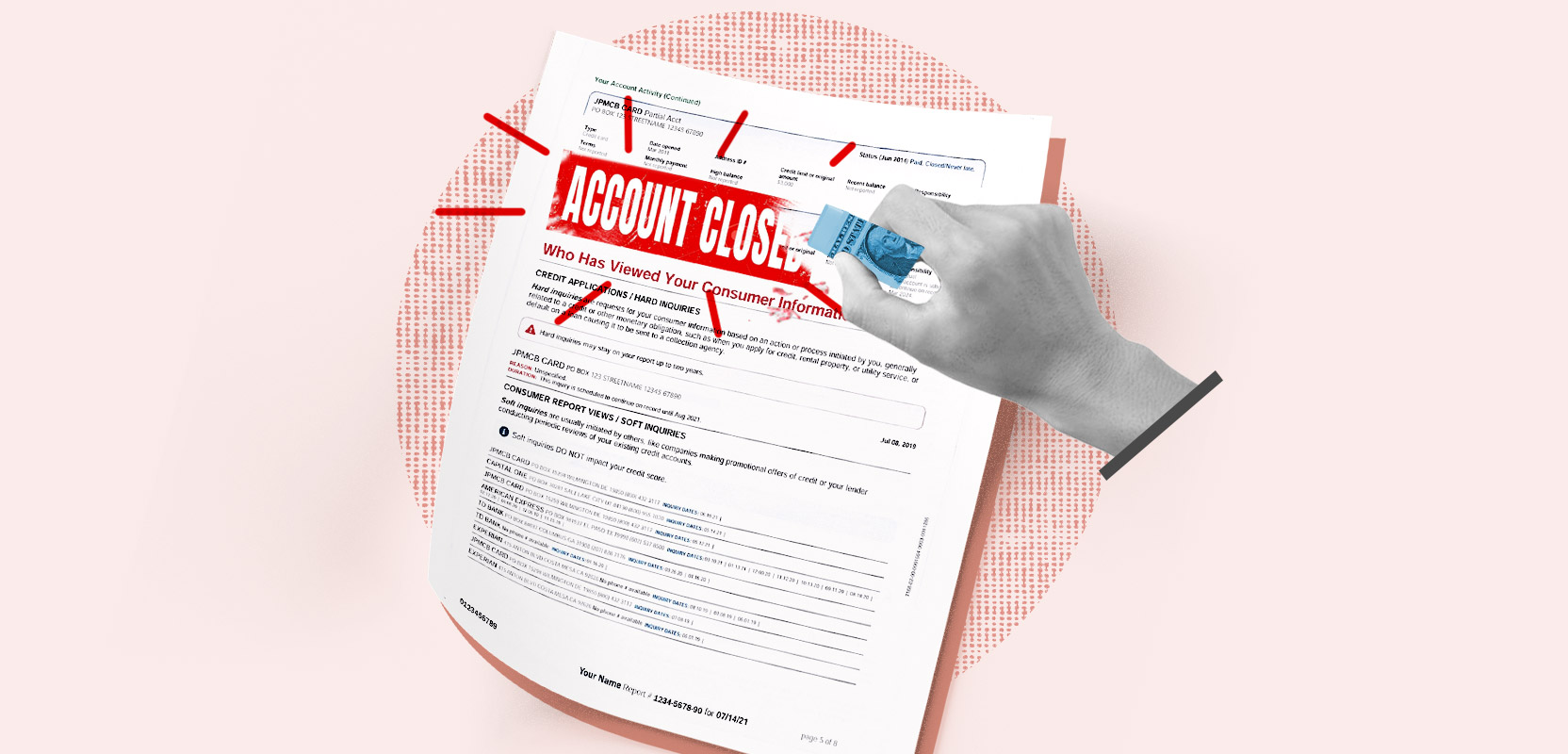

Student loans can have a significant impact on your credit report and overall financial health. As a borrower, it is essential to understand how these loans can affect your credit and what steps you can take to potentially remove them from your credit report.

When you take out a student loan, it becomes part of your credit history. This means that the loan details, including payment history, outstanding balances, and any delinquencies or defaults, are reported to credit bureaus. This information is used to calculate your credit score, which is a numerical representation of your creditworthiness.

Having student loans on your credit report can have both positive and negative effects. On one hand, consistently making on-time payments can demonstrate responsible financial behavior and help build a positive credit history. On the other hand, missed or late payments can lower your credit score and make it more challenging to qualify for future credit.

It is important to remember that removing student loans from your credit report is not a guaranteed or instantaneous process. However, with careful attention to your credit reports and proactive steps, you may be able to improve your credit standing over time.

In this article, we will discuss the steps you can take to potentially remove student loans from your credit report. By following these steps and maintaining good credit practices, you can work towards improving your credit score and financial well-being.

Understanding the Impact of Student Loans on Credit Reports

Student loans play a crucial role in shaping your credit report and, subsequently, your overall creditworthiness. Here are some key points to help you understand the impact of student loans on credit reports:

1. Loan History: Your student loan payment history is a significant factor in determining your credit score. Making timely payments reflects positively on your credit report, showing lenders that you are responsible and can manage your debt. On the other hand, missed or late payments can have a detrimental effect on your credit score and make it more challenging to obtain credit in the future.

2. Loan Balances: The outstanding balance of your student loans also affects your credit report. Large balances relative to your income or overall credit limit can negatively impact your credit utilization ratio, which is the percentage of available credit you have used. High credit utilization can be seen as a red flag by lenders and can lower your credit score.

3. Length of Credit History: Student loans often have longer repayment terms, which means they can contribute positively to the length of your credit history. The longer you have a loan in good standing, the more it can enhance your credit report. However, it is important to note that a longer credit history only benefits your credit score if you have made consistent and timely payments.

4. Types of Credit: Your credit mix also plays a role in your credit report. Having different types of credit, such as student loans, credit cards, and auto loans, can show lenders that you can handle various forms of credit responsibly. This diversity can positively impact your credit score.

It is crucial to understand that once your student loans are reported to the credit bureaus, they will remain on your credit report for a significant period, even after they are paid off. However, the impact on your credit score can lessen over time as you demonstrate responsible financial behavior and build a positive credit history.

By understanding how student loans impact your credit report, you can make informed decisions and take steps to improve your creditworthiness. In the following sections, we will discuss the specific steps you can take to potentially remove student loans from your credit report.

Steps to Remove Student Loans from Your Credit Report

If you’re looking to remove student loans from your credit report, it’s important to understand that the process may require persistence and patience. However, by following these steps, you can increase your chances of success:

1. Review Your Credit Reports: Start by obtaining copies of your credit reports from the three major credit bureaus – Equifax, Experian, and TransUnion. Carefully review each report to identify any student loan accounts that are inaccurately reported or contain errors.

2. Check for Errors and Inaccuracies: Look for discrepancies in loan balances, payment history, or even accounts that don’t belong to you. Pay attention to misspellings or incorrect personal information. These errors can negatively impact your credit score and need to be addressed.

3. Dispute Inaccurate Information with Credit Bureaus: Use the credit dispute process to contest any inaccurate information on your credit reports. Write a formal letter to each credit bureau, clearly stating the errors and providing supporting documentation to back up your claim.

4. Provide Documentation to Support Your Dispute: Gather relevant paperwork such as loan statements, payment receipts, and any correspondence with lenders or loan servicers. Include copies of this documentation when submitting your dispute to the credit bureaus. This evidence can strengthen your case and increase the likelihood of a successful dispute.

5. Follow Up with Credit Bureaus and Loan Servicers: Keep track of your dispute progress and follow up with the credit bureaus if you haven’t received a response within the designated time frame, typically 30 days. Similarly, if your dispute is resolved in your favor, ensure that the corrected information is reflected in your credit reports. Additionally, communicate with your loan servicers to rectify any errors on their end.

6. Utilize Good Credit Practices: While the above steps focus on disputing and removing inaccurate information, it’s equally important to build a positive credit history. Make your loan payments on time, reduce your overall debt, and avoid applying for excessive credit in a short period. These good credit practices can help improve your credit score and offset any negative impact from the student loans.

Removing student loans from your credit report may not happen overnight, but by staying vigilant and taking the necessary steps, you can make significant progress. Remember, a better credit report can lead to improved financial opportunities and make it easier to achieve your goals.

Step 1: Review Your Credit Reports

The first step in the process of potentially removing student loans from your credit report is to review your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. By obtaining these reports, you can gain a clear understanding of how your student loans are currently being reported and identify any potential errors or inaccuracies.

Here are some key points to consider when reviewing your credit reports:

1. Obtain Copies of Your Credit Reports: You can request a free copy of your credit report from each of the three credit bureaus once a year by visiting AnnualCreditReport.com. Alternatively, you can also access your reports through various credit monitoring services or directly from each credit bureau’s website.

2. Thoroughly Examine Each Credit Report: Take the time to carefully go through each section of your credit reports. Look for any student loan accounts that are inaccurately reported, such as incorrect balances or missed payments. Check for any accounts that don’t belong to you, as they may be fraudulent and should be disputed.

3. Verify Personal Information: Ensure that all personal information, such as your name, address, and social security number, is accurate. Any errors in this information could potentially lead to the misreporting of your student loans. Contact the credit bureau to correct any inaccurate personal details.

4. Pay Attention to Loan Details: Note the specific details of each student loan account, including the loan holder, loan balance, payment history, and current status. Ensure that all the information aligns with your records and that there are no discrepancies. If you find any discrepancies, mark them for further investigation and potential dispute.

5. Take Notes and Document Findings: As you review your credit reports, make notes of any errors, discrepancies, or inaccuracies you come across. Document the account names, loan numbers, and specific details that need to be addressed. This will help you take organized and focused action in the next steps of the process.

By thoroughly reviewing your credit reports, you can pinpoint any issues related to the reporting of your student loans. Identifying errors or inaccuracies is crucial in taking the necessary steps to potentially remove or correct them. Once you have a clear picture of the reporting status of your student loans, you can proceed to the next step of addressing any discrepancies through the credit dispute process.

Step 2: Check for Errors and Inaccuracies

After obtaining your credit reports and reviewing them thoroughly, the next step in the process of potentially removing student loans from your credit report is to check for errors and inaccuracies. It’s crucial to identify any discrepancies relating to your student loans, as they can have a substantial impact on your credit score and overall creditworthiness.

Here are some key areas to focus on when checking for errors and inaccuracies:

1. Loan Balances: Compare the outstanding balances reported on your credit reports with your own loan statements. If you notice any discrepancies, such as inflated balances or inaccurate loan amounts, take note of them. These errors can significantly impact your credit utilization ratio, which measures the amount of credit you’re using compared to your total available credit.

2. Payment History: Review the payment history for each student loan account on your credit reports. Ensure that the reported payment dates and amounts align with your own records. Look out for any missed or late payments that may have been erroneously reported. Timely payment history is crucial for maintaining a good credit score.

3. Account Status: Check the current status of your student loan accounts. Verify that each account is accurately reported as open, closed, paid off, or in deferment/forbearance status. If you have paid off a loan but it is still showing as outstanding, this is an error that should be addressed.

4. Duplicate Accounts: Look out for any duplicate accounts on your credit reports. Sometimes, a student loan may be mistakenly listed multiple times, which can inflate your overall debt and negatively impact your credit score. Make note of any duplicate accounts and plan to dispute them with the credit bureaus.

5. Personal Information: Pay close attention to your personal information, such as your name, address, and Social Security number. Incorrect personal information can lead to incorrect reporting of your student loans. If you identify any errors, contact the credit bureau to correct them.

It’s important to be thorough and vigilant when checking for errors and inaccuracies on your credit reports. Make note of any discrepancies you come across, as they will be crucial in the next steps of disputing and potentially removing these inaccuracies from your credit report. By addressing these errors, you can work towards improving the accuracy of your credit history and increasing your chances of having student loans removed from your report.

Step 3: Dispute Inaccurate Information with Credit Bureaus

After identifying errors and inaccuracies related to your student loans on your credit reports, the next step is to formally dispute this information with the credit bureaus. Disputing inaccurate information is an important process to rectify any errors and potentially remove these inaccuracies from your credit report.

Here are the key steps to follow when disputing inaccurate information with the credit bureaus:

1. Gather Documentation: Compile all relevant documentation that supports your claim of inaccuracies. This can include loan statements, payment receipts, correspondence with lenders or loan servicers, and any other documentation that validates your position. Having strong evidence will help strengthen your case during the dispute process.

2. Write a Formal Dispute Letter: Draft a formal dispute letter to the credit bureaus. In the letter, be clear and concise in explaining the errors or inaccuracies you have identified on your credit reports. Include the account name, account number, and precise details of the information you are disputing. Back up your claims with the supporting documentation you gathered.

3. Submit the Dispute Letter: Send the dispute letter to each of the credit bureaus by certified mail with a return receipt requested. This way, you have proof that the credit bureaus received your dispute. Ensure you keep a copy of the letter and all supporting documents for your records.

4. Credit Bureau Investigation: The credit bureaus are required by law to investigate the disputed information within 30 days of receiving your dispute. They will contact the creditor or loan servicer associated with the disputed account and request verification of the information. During this process, the credit bureaus will review the evidence provided and make a determination.

5. Review the Investigation Results: After conducting their investigation, the credit bureaus will provide you with the results in writing. They will update your credit report accordingly if any errors or inaccuracies are found. If your dispute is successful, the inaccurate information will be removed or corrected, potentially leading to an improvement in your credit score.

6. Follow Up Regularly: If the investigation does not result in the removal or correction of the inaccurate information, it’s important to follow up with the credit bureaus and provide any additional evidence or information that supports your dispute. Persistence is key in ensuring that the inaccuracies are corrected as necessary.

Note that the credit bureaus are legally obligated to investigate your dispute, but the final decision ultimately rests with them. If you are unsatisfied with the outcome, you may consider seeking legal advice or contacting a credit counseling agency for further assistance.

By formally disputing inaccurate information with the credit bureaus, you can take proactive steps to address the errors and potentially remove them from your credit report. This process is a crucial part of improving the accuracy of your credit history and enhancing your overall creditworthiness.

Step 4: Provide Documentation to Support Your Dispute

When disputing inaccurate information with the credit bureaus, it is essential to provide supporting documentation to strengthen your case. By submitting relevant documents that validate your claims, you increase the chances of a successful dispute and the potential removal of inaccurate information from your credit report.

Here are the key steps to follow when providing documentation to support your dispute:

1. Gather Relevant Documentation: Collect all pertinent documentation related to the disputed account. This may include loan statements, payment receipts, cancellation or deferment letters, and any other paperwork that supports your position. Ensure that the documents clearly reflect the correct information and contradict the inaccuracies on your credit report.

2. Organize and Make Copies: Arrange your supporting documents in a clear and organized manner. Make copies of each document to include with your dispute letter. It is important to keep the original copies for your records, as they may be required in case of any future inquiries or disputes.

3. Highlight Relevant Information: As you review your supporting documents, highlight or underline the sections that directly relate to the inaccurate information being disputed. This makes it easier for the credit bureaus to quickly identify the discrepancies and understand the evidence you are presenting.

4. Include a Cover Letter: Draft a cover letter to accompany your dispute and supporting documents. In the letter, explain the purpose of the documentation you are providing and how it supports your claim. Be concise and clear, ensuring that your points are easy to understand.

5. Number and Reference Documents: Number or label each document and refer to them in your cover letter as you explain their significance. This helps the credit bureaus navigate through the supporting evidence and understand how each document relates to the specific inaccuracies being disputed.

6. Send Certified Mail: When submitting your dispute and documentation to the credit bureaus, send the package via certified mail with a return receipt requested. This method ensures that you have proof of mailing and allows you to track the delivery status.

7. Keep Copies for Your Records: Retain copies of the dispute package, including the cover letter and all supporting documents, for your records. This way, you have a complete record of the information you provided, which can be useful for future reference or if any further action is required.

By providing thorough and well-organized documentation, you demonstrate the validity of your dispute and increase the likelihood of a successful resolution. Your supporting evidence serves as a compelling argument for the removal or correction of inaccurate information on your credit report.

Remember to keep copies of all documents and correspondence related to your dispute, as you may need them in case of any future inquiries or follow-ups. With solid supporting documentation, you are positioning yourself for a stronger dispute resolution and potential improvement in your credit report.

Step 5: Follow Up with Credit Bureaus and Loan Servicers

After submitting your dispute and supporting documentation to the credit bureaus, it’s important to follow up with them to ensure your dispute is being properly addressed. Additionally, it may be necessary to reach out to your loan servicers to rectify any errors on their end. Here are the key steps to follow when following up with the credit bureaus and loan servicers:

1. Maintain Documentation: Keep copies of all correspondence, including the dispute letter, supporting documents, and any responses received from the credit bureaus or loan servicers. This documentation will serve as evidence of your efforts and can be helpful if you need to escalate the dispute process.

2. Track the Progress: Keep track of the timeline for the credit bureaus to investigate your dispute. They are required by law to complete their investigation within 30 days. Monitor the progress and ensure that they are actively working on your case.

3. Follow Up in Writing: If you haven’t received a response from the credit bureaus within 30 days, or if the response does not adequately address your dispute, follow up in writing. Send a letter requesting an update on the investigation and provide any additional information or evidence that may support your case. Send the letter via certified mail to have a record of its delivery.

4. Communicate with Loan Servicers: If the inaccuracies on your credit report are due to errors made by your loan servicers, contact them directly to address the issue. Provide them with the necessary information and documentation to support your claim. Request that they correct the information they reported to the credit bureaus and confirm that the changes will be reflected on your credit report.

5. Be Persistent: If your initial attempts to resolve the dispute are unsuccessful, don’t give up. Persistence is key in ensuring that inaccuracies are corrected. Continue to follow up with the credit bureaus and loan servicers until the issue is resolved to your satisfaction.

6. Consider Seeking Legal Assistance: If all attempts to resolve the dispute have failed, and the inaccurate information remains on your credit report, you may want to consult with a consumer rights attorney or credit counseling agency. They can provide guidance and assistance in resolving the issue and protecting your rights as a consumer.

Following up with the credit bureaus and loan servicers is crucial in ensuring that your dispute is being thoroughly investigated and resolved. By maintaining clear documentation and persistently pursuing a resolution, you increase the chances of having the inaccurate information removed or corrected from your credit report, ultimately improving your credit standing.

Step 6: Utilize Good Credit Practices

While you work on resolving any inaccuracies related to your student loans on your credit report, it’s important to utilize good credit practices to improve your overall creditworthiness. Establishing strong credit habits can not only mitigate the impact of negative information but also help build a positive credit history. Here are some key practices to consider:

1. Make Timely Payments: Pay all your bills, including your student loan payments, on time. Late or missed payments can negatively impact your credit score and make it harder to remove inaccuracies from your credit report. Set up automatic payments or calendar reminders to ensure timely payments.

2. Reduce Debt: Work on reducing your overall debt, including credit card balances and other outstanding loans. High debt levels can affect your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. Aim to keep your credit utilization below 30% to improve your credit score.

3. Maintain Low Credit Card Balances: Keep your credit card balances as low as possible. This demonstrates responsible credit management and can positively impact your credit score. Avoid maxing out your credit cards and consider paying off the balances in full each month, if possible.

4. Limit New Credit Applications: Be cautious when applying for new credit. Each credit application results in a hard inquiry on your credit report, which can temporarily lower your credit score. Only apply for credit when necessary and only after careful consideration of the terms and conditions.

5. Diversify Your Credit Mix: A healthy credit mix can positively impact your credit score. Consider having a variety of credit accounts, such as student loans, credit cards, and auto loans, to demonstrate your ability to manage different types of credit responsibly.

6. Regularly Monitor Your Credit: Stay informed about your credit status by regularly monitoring your credit reports and credit scores. Keep an eye out for any new inaccuracies or errors that may arise. Monitoring your credit allows you to address issues promptly and take necessary action.

By implementing these good credit practices, you can strengthen your overall credit profile and mitigate the impact of inaccurate information on your credit report. Over time, as you demonstrate responsible financial behavior, the positive aspects of your credit history will overshadow any negative information, leading to an improvement in your creditworthiness.

Remember, managing your credit responsibly and consistently implementing these practices are long-term habits that can yield positive results and help you achieve your financial goals.

Conclusion

Dealing with student loans on your credit report can feel overwhelming, but by taking proactive steps, you can potentially remove inaccuracies and improve your credit standing. While it may require time and effort, the benefits of having a more accurate credit report can have a significant impact on your financial well-being.

Through the steps outlined in this article, you can navigate the process of potentially removing student loans from your credit report:

1. Review your credit reports to identify any errors or inaccuracies.

2. Check for discrepancies in loan balances, payment history, and personal information.

3. Formalize the dispute process by submitting a dispute letter to the credit bureaus.

4. Provide supporting documentation to strengthen your dispute.

5. Follow up with the credit bureaus and loan servicers to ensure your dispute is being investigated.

6. Utilize good credit practices to improve your overall creditworthiness.

Remember, the road to removing inaccuracies from your credit report may not be an overnight process. It requires persistence, organization, and attention to detail. However, by addressing these issues head-on, you can improve your creditworthiness and open up opportunities for better financial prospects in the future.

Alongside disputing inaccurate information, it is crucial to establish and maintain good credit practices. Making timely payments, reducing debt, and regularly monitoring your credit are key factors in building a positive credit history.

Lastly, if you face challenges or need guidance throughout the process, consider seeking advice from a consumer rights attorney or a credit counseling agency. These professionals can provide expertise and support to help you navigate through any complications that may arise.

By taking control of your credit report and actively working towards removing inaccuracies, you can pave the way for a healthier credit profile and improve your financial prospects moving forward. Stay informed, persistent, and proactive, and you’ll be on your way to a better credit future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance