Finance

What Is A Credit Card Authorization

Published: October 24, 2023

Learn all about credit card authorization and how it works in the realm of finance. Gain valuable insights and tips to ensure seamless transactions and security.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Credit Card Authorization

- Purpose of Credit Card Authorization

- How Credit Card Authorization Works

- Importance of Credit Card Authorization

- Common Methods of Credit Card Authorization

- Factors Affecting Credit Card Authorization

- Benefits and Risks of Credit Card Authorization

- Authorization Holds and Release

- Authorization vs. Settlement

- Conclusion

Introduction

In today’s digital age, credit cards have become an essential tool for financial transactions. Whether you’re making online purchases, booking travel accommodations, or simply grabbing a quick cup of coffee, credit cards offer convenience and security. However, behind the scenes of every credit card transaction lies a crucial process called credit card authorization.

Credit card authorization is the verification process that takes place between the merchant, the card issuer, and the payment processor to ensure that a credit card transaction is legitimate and approved. It plays a vital role in protecting both consumers and businesses from fraudulent activities, ensuring the seamless flow of funds, and maintaining the overall integrity of the financial system.

This article will provide a comprehensive understanding of credit card authorization, exploring its definition, purpose, working process, importance, methods, factors affecting it, and the benefits and risks associated with it. We’ll also delve into the concept of authorization holds and releases, as well as the distinction between authorization and settlement. By the end, you’ll have a clear grasp of how credit card authorization plays a significant role in our everyday financial transactions.

Definition of Credit Card Authorization

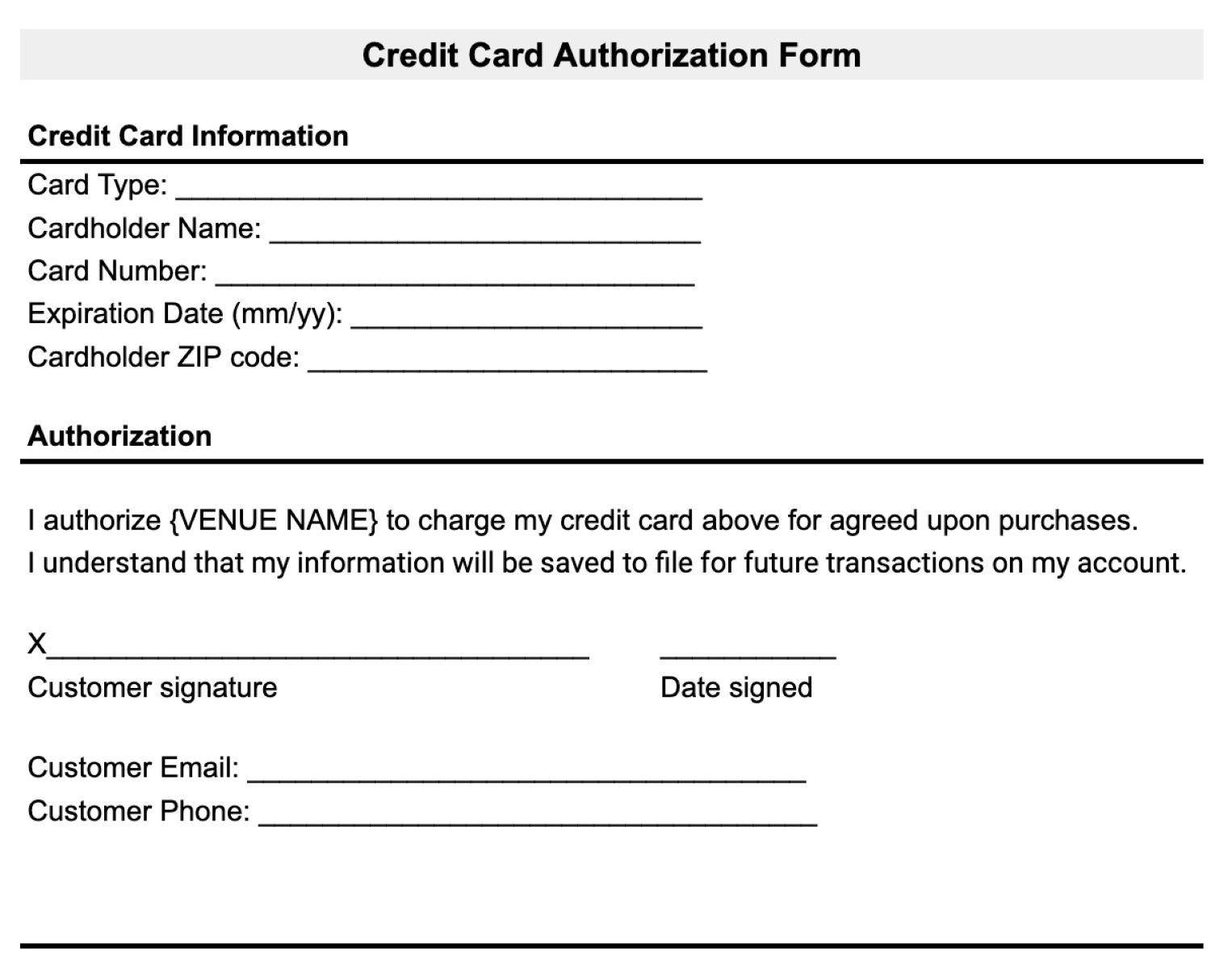

Credit card authorization refers to the process of validating a credit card’s legitimacy and available credit limit before approving a transaction. It ensures that the cardholder has the necessary funds or credit line to cover the purchase and protects merchants from potential losses due to fraudulent transactions. Essentially, it acts as a security measure to verify and authenticate credit card transactions.

During the credit card authorization process, the merchant’s payment terminal or online payment gateway sends a request to the card issuer or the issuing bank to confirm the validity and availability of funds for a particular transaction. The card issuer then evaluates the request, checking factors such as the card’s validity, the cardholder’s credit limit, and any potential fraud alerts.

If the information provided by the merchant matches the cardholder’s details and there are sufficient funds available, the card issuer approves the authorization request. The funds are then reserved, or put on hold, to ensure they will be available for the transaction to be finalized later during settlement. If the authorization is declined, the transaction is not processed, and the cardholder is notified of the rejection.

It is important to note that credit card authorization is not the same as the final payment or settlement. It is merely an approval to proceed with the transaction, reserving the necessary funds. The actual payment takes place during the settlement process, where the reserved funds are transferred from the cardholder’s account to the merchant’s account.

Overall, credit card authorization serves as a vital step in ensuring the security, validity, and efficiency of credit card transactions. It protects both consumers and businesses from fraudulent activities, reduces the risk of chargebacks, and helps maintain the smooth functioning of the financial ecosystem.

Purpose of Credit Card Authorization

The primary purpose of credit card authorization is to validate and verify the legitimacy of a credit card transaction. By authorizing a transaction, the card issuer confirms that the cardholder has sufficient funds or credit available and reduces the risk of fraud and chargebacks. Let’s delve into the key purposes of credit card authorization.

- Preventing Fraud: Credit card authorization serves as a vital defense against unauthorized transactions and fraudulent activities. By verifying the cardholder’s information and available credit, the authorization process helps identify and prevent fraudulent use of stolen or counterfeit cards. This protection benefits both consumers and businesses, ensuring that only legitimate transactions are processed.

- Protecting Merchants: Authorization protects merchants from financial losses due to chargebacks or disputed transactions. When a transaction is authorized, the funds are reserved or held to guarantee that they will be available for settlement. This reduces the risk of a merchant providing goods or services without receiving payment or facing penalties for disputes.

- Ensuring Sufficient Funds: Before completing a transaction, credit card authorization confirms that the cardholder has enough funds or an available credit limit to cover the purchase. This helps prevent any declined transactions or inconvenience for the cardholder due to insufficient funds.

- Mitigating Risk: By following established authorization protocols, credit card issuers and merchants can mitigate the risk of accepting fraudulent transactions. These protocols typically involve checking the card’s security features, verifying the cardholder’s identity, and assessing any potential risk factors associated with the transaction.

- Building Trust: Credit card authorization enhances the overall trust and confidence in the payment system. Consumers can feel secure knowing that their credit card transactions are being validated and protected against unauthorized use. This trust encourages more consumers to use credit cards for their purchases, contributing to the growth of e-commerce and other digital payment methods.

In summary, credit card authorization serves multiple purposes, including preventing fraud, protecting merchants, ensuring sufficient funds, mitigating risk, and building trust. It plays a crucial role in maintaining the security and integrity of credit card transactions, benefiting both consumers and businesses in the process.

How Credit Card Authorization Works

Credit card authorization involves a series of steps and interactions between the merchant, the cardholder, the card issuer, and the payment processor. Let’s explore the process of how credit card authorization works:

- Customer Initiates a Transaction: The credit card authorization process begins when a customer initiates a transaction, either in-person at a physical store or online through a website or mobile app.

- Merchant Sends Authorization Request: The merchant’s payment terminal or online payment gateway sends an authorization request to the card issuer or the issuing bank. The request typically includes information such as the card number, expiration date, and transaction amount.

- Authorization Request Sent to Card Issuer: The card issuer receives the authorization request and verifies the cardholder’s information and available credit. This involves checking the validity of the card, verifying the cardholder’s identity through security measures like CVV codes or biometric authentication, and assessing any risk factors associated with the transaction.

- Card Issuer Approves or Declines Authorization: Based on the evaluation, the card issuer approves or declines the authorization request. If approved, the issuer sets aside the necessary funds or places a hold on the cardholder’s available credit. If declined, the transaction is not processed, and the cardholder is notified of the rejection.

- Payment Processor Relays Response: The authorization response from the card issuer is then relayed back to the merchant’s payment terminal or online payment gateway. The response indicates whether the transaction is approved or declined.

- Customer Completes Transaction: If the authorization is approved, the customer can proceed to complete the transaction. In an in-person transaction, the customer typically signs a receipt or enters their PIN to authorize the payment. In an online transaction, the customer may need to provide additional security measures, such as a one-time password or biometric authentication.

- Settlement and Transfer of Funds: Once the transaction is completed, the authorized funds are transferred from the cardholder’s account to the merchant’s account during the settlement process. This typically occurs within a few days, depending on the settlement terms and the merchant’s payment processing timeline.

It’s important to note that the speed and efficiency of the credit card authorization process can vary depending on various factors, such as the card issuer’s response time, the availability of funds or credit, and any additional security checks implemented by the merchant or payment processor. However, the overall goal of credit card authorization is to ensure the validity and security of transactions while maintaining a smooth flow of funds between the cardholder and the merchant.

Importance of Credit Card Authorization

Credit card authorization plays a vital role in the modern financial ecosystem, benefiting both consumers and businesses. Let’s explore the importance of credit card authorization in more detail:

- Protection against Fraud: Credit card authorization serves as a crucial safeguard against fraudulent transactions. By verifying the cardholder’s information and available credit, the authorization process helps detect and prevent instances of unauthorized use, stolen cards, or counterfeit cards. This protection reduces the financial burden on both consumers and merchants, promoting trust in the payment system.

- Reduced Chargebacks: Authorization helps reduce the risk of chargebacks for merchants. When a transaction is authorized, the funds are held or reserved, ensuring that the necessary funds are available for settlement. This reduces the likelihood of a customer disputing a transaction or initiating a chargeback, ultimately reducing potential losses and administrative hassle for merchants.

- Enhanced Security: Credit card authorization contributes to the overall security of financial transactions. It incorporates various security measures, such as CVV codes, address verification, and risk assessment, to authenticate the cardholder and validate the transaction. This helps protect sensitive cardholder data and prevents unauthorized access or use of credit cards.

- Efficient Funds Management: By authorizing transactions, credit card issuers can effectively manage the available credit or funds for cardholders. This enables efficient budgeting and spending control, providing cardholders with a clear understanding of their credit limits and preventing overspending or exceeding credit limits.

- Seamless Payment Experience: Credit card authorization ensures a seamless and hassle-free payment experience for consumers. It allows for quick and efficient approval of transactions, eliminating the need for manual verification or lengthy authorization processes. This convenience encourages consumers to use credit cards more frequently for their purchases, driving economic growth and enhancing customer satisfaction.

- Protection for Cardholders: Credit card authorization protects cardholders from unauthorized transactions, minimizing their financial liability in case of fraudulent activity. In most cases, cardholders are only responsible for reporting any suspicious transactions promptly. This provides peace of mind and confidence in using credit cards, as cardholders know they have recourse in case of fraudulent or unauthorized use.

In summary, credit card authorization plays a critical role in protecting consumers and businesses, ensuring the security of transactions, reducing the risk of fraud and chargebacks, and providing a seamless payment experience. It instills confidence in the financial system, promoting the use of credit cards as a trusted and secure method of payment.

Common Methods of Credit Card Authorization

Credit card authorization involves various methods and technologies to verify and authenticate transactions. These methods are designed to ensure the security and integrity of the payment process. Let’s explore some of the common methods of credit card authorization:

- Magnetic Stripe Cards: Magnetic stripe cards were one of the earliest methods of credit card authorization. The card’s magnetic stripe contains encoded information, including the cardholder’s account number and other relevant data. When swiped through a card reader, the information is read and verified by the card issuer, authorizing the transaction.

- Chip-and-PIN: Chip-and-PIN, also known as EMV (Europay, Mastercard, and Visa), is a widely adopted method of credit card authorization. It involves the use of a microchip embedded in the card, which contains encrypted data. During a transaction, the cardholder inserts the card into a compatible reader and enters a unique PIN. The chip generates a unique transaction code, which is validated by the card issuer for authorization.

- Contactless Payments: Contactless payments utilize Near Field Communication (NFC) technology to authorize transactions. The credit card or mobile device is brought close to a contactless-enabled terminal, and the necessary information is transmitted wirelessly for authorization. These payments typically have a maximum transaction limit and do not require a signature or PIN for smaller amounts.

- Tokenization: Tokenization is a method that replaces the actual credit card number with a unique token during the authorization process. The token is a randomly generated string of characters that is used instead of the card details for transaction authorization. This enhances security by minimizing the risk of sensitive cardholder data being intercepted or compromised during the transaction process.

- 3D Secure: 3D Secure is an additional security layer for online credit card transactions. It requires the cardholder to enter a one-time password or personal information that only the cardholder would know, in addition to entering the card details. This method helps validate the transaction and reduce the risk of fraudulent activities.

- Address Verification System (AVS): AVS is a method that compares the address provided by the cardholder during the transaction to the billing address on file with the card issuer. By matching the address information, AVS helps confirm the validity of the transaction and reduces the risk of fraudulent activities.

These are just a few of the common methods of credit card authorization. The specific method used may vary depending on the card issuer, merchant, and the technology available. The constant evolution of payment technologies and the increased focus on security continue to drive innovation in credit card authorization methods.

Factors Affecting Credit Card Authorization

Credit card authorization is influenced by several factors that impact the decision to approve or decline a transaction. These factors are taken into consideration to ensure the security and validity of the transaction. Let’s explore some of the key factors that can affect credit card authorization:

- Available Credit Limit: One of the primary factors impacting credit card authorization is the available credit limit on the card. The credit card issuer will check if the transaction amount exceeds the cardholder’s available credit. If the transaction amount exceeds the credit limit, the authorization may be declined.

- Cardholder Verification: Authorization may also depend on the cardholder’s identity verification. This can include entering a PIN, providing a signature, or verifying personal information associated with the card. Card issuers use these verification methods to ensure that the person using the card is the legitimate cardholder.

- Merchant Category Code (MCC): Some card issuers may have restrictions or specific rules based on the merchant category code (MCC) associated with the merchant. Certain types of businesses may be considered higher risk or may be subject to additional scrutiny during the authorization process. For example, transactions made at casinos or adult entertainment establishments may undergo more stringent authorization checks.

- Transaction Amount: The amount of the transaction also plays a role in credit card authorization. Large or unusual transactions may raise flags for further verification to ensure that the transaction is legitimate and authorized by the cardholder.

- Card Usage Patterns: Card issuers may monitor the cardholder’s usage patterns and purchase history to detect any irregularities or suspicious activities. Unusual spending patterns, such as a sudden increase in transaction amounts or purchases in unfamiliar locations, may trigger additional authorization checks before approving a transaction.

- Fraud Detection Measures: Card issuers employ various fraud detection measures to identify and prevent unauthorized transactions. These measures can include real-time fraud monitoring systems that analyze transaction patterns, use of artificial intelligence algorithms to detect anomalies, and blacklists of known fraudulent card numbers or merchants.

It’s important to note that the specific factors considered in the credit card authorization process can vary between card issuers and may depend on their risk assessment policies. By carefully evaluating these factors, credit card issuers can protect the cardholder from fraudulent activities while ensuring a smooth and secure payment experience.

Benefits and Risks of Credit Card Authorization

Credit card authorization offers several benefits for both consumers and businesses, but it is not without its risks. Understanding these benefits and risks is important in order to make informed decisions regarding credit card transactions. Let’s explore the benefits and risks of credit card authorization:

- Benefits:

- Security: Credit card authorization provides security by verifying the legitimacy of transactions, protecting cardholders from unauthorized use and merchants from potential losses due to fraud.

- Convenience: The authorization process is typically quick and seamless, providing a convenient payment experience for consumers. It allows for instant approval, reducing the need for manual verification and paperwork.

- Reduced Chargebacks: Authorization reduces the risk of chargebacks for merchants. Approved transactions are more likely to be valid, decreasing the likelihood of disputes or customer-initiated chargebacks.

- Funds Availability: Authorization ensures that funds or credit limits are available to cover the transaction, minimizing the chances of declined transactions due to insufficient funds or credit.

- Built-in Fraud Protection: Credit card authorization incorporates various security measures, such as CVV codes, address verification, and risk assessment, to protect against fraudulent activities, safeguarding both consumers and businesses.

- Risks:

- Authorization Holds: One potential risk is the occurrence of authorization holds. When a transaction is authorized, the funds may be put on hold or reserved, temporarily reducing the available credit or funds for the cardholder until the final settlement.

- Transaction Declines: In some cases, valid transactions may be declined during the authorization process due to factors like temporary issues with the card issuer’s system or a miscommunication between the merchant and the card issuer.

- Data Breaches: Credit card authorization involves the sharing of sensitive personal and financial information, which can be a target for hackers and data breaches. Card issuers and merchants must maintain stringent security measures to protect cardholder data.

- False Sense of Security: While credit card authorization provides protection against fraudulent transactions, it may give cardholders a false sense of security. Cardholders should remain vigilant and monitor their transactions to identify any unauthorized or suspicious activity.

- Potential for Fraud: Although credit card authorization helps in minimizing fraudulent activities, there is always a risk of sophisticated fraud techniques bypassing the authorization process. Cardholders and merchants should remain aware of potential fraud risks and implement additional security measures as necessary.

It is crucial for both cardholders and merchants to understand and balance the benefits and risks associated with credit card authorization. By staying informed and implementing security best practices, the advantages can be maximized, while any potential risks can be mitigated to ensure a secure and efficient payment experience.

Authorization Holds and Release

Authorization holds, also known as pending transactions or preauthorizations, are a common practice in credit card authorization. They occur when a merchant requests an authorization for a specific amount, which temporarily sets aside those funds or puts a hold on the cardholder’s available credit limit. Let’s take a closer look at authorization holds and the process of their release:

When a credit card transaction is authorized, the issuing bank or card issuer reserves the necessary funds to ensure they are available for the final settlement. This serves as a guarantee for the merchant that the funds will be available when the transaction is settled. Authorization holds are commonly seen in scenarios such as hotel bookings, car rentals, or other services where the final amount may vary or additional charges may be incurred.

Here is an overview of how authorization holds and releases work:

- Authorization Hold: When a merchant initiates a transaction, they contact the card issuer to obtain authorization for a specific amount. The issuing bank verifies the cardholder’s information, available credit, and other factors to approve the authorization request. The approved amount is then set aside, and the cardholder’s available credit or funds are temporarily reduced by that amount.

- Hold Period: The duration of the authorization hold can vary and is determined by the merchant’s policies, industry practices, and the card issuer’s terms. Holds can typically last anywhere from a few hours to several days, but in some cases, it can take up to a week or more for the hold to be released.

- Release of Hold: Once the transaction is settled, the merchant sends a request for the final amount to the card issuer for payment. At this point, the authorization hold is released, and the funds or credit limit that were previously held become available again to the cardholder. The final transaction amount replaces the hold amount, and the cardholder’s account reflects the updated available credit or funds.

- Partial Authorization: In some cases, a merchant may request authorization for an amount that is higher than the actual transaction total, such as when a tip or additional charges are added later. This can result in a partial authorization, where the initial hold amount is released, and a new hold is placed for the adjusted total. The initial hold will be replaced by the final hold amount once the transaction is settled.

It’s important to note that while the held funds or credit limit are not available for other transactions during the hold period, they are not debited from the cardholder’s account. It is crucial for cardholders to keep track of their transactions and ensure that any authorization holds are released after the settlement to avoid any discrepancies or confusion.

Authorization holds are a necessary part of credit card authorization, providing both merchants and card issuers with a level of security. While they can temporarily impact the cardholder’s available credit or funds, understanding the hold period and being aware of any pending transactions can help cardholders manage their finances effectively.

Authorization vs. Settlement

Authorization and settlement are two distinct stages in the process of a credit card transaction. Understanding the difference between the two is crucial for both merchants and cardholders. Let’s explore the key differences between authorization and settlement:

Authorization:

Authorization is the initial stage of a credit card transaction, where the cardholder’s available funds or credit limit is verified before a transaction is approved. During this stage, the merchant sends a request to the card issuer to confirm the legitimacy of the transaction and ensure that the cardholder has sufficient funds or credit available to cover the purchase.

The authorization process involves checking various factors, such as the validity of the card, the cardholder’s identity, and the available credit, to determine if the transaction should be approved. If the authorization is successful, the card issuer places a hold on the necessary funds or temporarily reduces the available credit limit by the transaction amount. However, no actual funds are transferred at this stage.

Settlement:

Settlement is the phase where the authorized transaction is finalized, and the actual transfer of funds takes place. It occurs after the goods or services have been provided by the merchant and typically happens within a few days of the initial authorization.

During the settlement process, the merchant sends a request for payment to the card issuer. The card issuer then transfers the authorized funds from the cardholder’s account to the merchant’s account, completing the transaction. The settlement amount may differ from the initially authorized amount due to additional charges, tips, or adjustments made by the merchant.

It is important to note that the settlement process may include other parties involved, such as the payment processor or acquiring bank, who facilitate the transfer of funds between the cardholder’s issuer and the merchant’s account.

Key Differences:

The main differences between authorization and settlement can be summarized as follows:

- Timing: Authorization takes place at the beginning of a transaction, ensuring the availability of funds or credit, while settlement occurs after the goods or services have been provided, finalizing the transfer of funds.

- Funds Transfer: Authorization does not involve the actual transfer of funds, but rather places a hold on the necessary amount. In contrast, settlement involves the transfer of the authorized funds from the cardholder’s account to the merchant’s account.

- Transaction Amount: The settlement amount may differ from the initially authorized amount due to additional charges or adjustments made by the merchant.

- Bank Involvement: Authorization primarily involves the cardholder’s issuing bank and the merchant, whereas settlement may involve additional parties such as payment processors or acquiring banks.

Understanding the distinction between authorization and settlement helps ensure transparency and clarity in credit card transactions. It allows cardholders to manage their available credit or funds effectively and enables merchants to receive timely payments for the goods or services provided.

Conclusion

Credit card authorization is a vital process that plays a crucial role in ensuring the security and integrity of financial transactions. It protects both consumers and businesses from fraudulent activities, reduces the risk of chargebacks, and provides a seamless payment experience. By verifying the legitimacy of credit card transactions and ensuring the availability of funds or credit, authorization enables the smooth and efficient flow of funds between the cardholder and the merchant.

Throughout this article, we have explored the definition, purpose, and working process of credit card authorization. We have discussed the importance of authorization in preventing fraud, protecting merchants, and building trust in the payment system. We have also examined common methods of credit card authorization, factors affecting the authorization decision, and the benefits and risks associated with the process.

Credit card authorization provides several benefits, including enhanced security, reduced chargebacks, efficient funds management, and a seamless payment experience. However, there are also risks to consider, such as authorization holds, transaction declines, and the potential for fraud or data breaches.

Understanding the distinction between authorization and settlement is essential, as they represent different stages in the credit card transaction process. While authorization confirms the availability of funds or credit, settlement involves the actual transfer of the authorized funds to the merchant’s account.

In conclusion, credit card authorization is a critical aspect of modern financial transactions, enabling safe and reliable payments. By staying informed about the process, consumers can use credit cards with confidence, while businesses can protect themselves against fraud and maintain a high level of service. As technology evolves, credit card authorization will continue to adapt and improve, ensuring secure and convenient transactions well into the future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance