Home>Finance>What Is Another Name For Interest-Sensitive Whole Life Insurance?

Finance

What Is Another Name For Interest-Sensitive Whole Life Insurance?

Published: October 15, 2023

Discover the alternative term for interest-sensitive whole life insurance in the world of finance. Explore the benefits and features of this financial product.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of finance and insurance, where individuals and families seek protection and financial security. In this realm, life insurance plays a crucial role in safeguarding loved ones and providing peace of mind. One type of life insurance that stands out is interest-sensitive whole life insurance. But what exactly is interest-sensitive whole life insurance?

Interest-sensitive whole life insurance is a unique and flexible insurance product that combines the benefits of whole life insurance with the potential to earn interest on the policy’s cash value. Unlike other forms of life insurance, it offers policyholders the opportunity to adjust their premiums and death benefits as their needs change over time. This feature makes it an appealing option for those looking for flexibility and potential growth.

Interest-sensitive whole life insurance operates on the principle of linking the policy’s cash value to an underlying interest-bearing account. The interest earned on this account is typically tied to prevailing market rates and can be credited to the policy’s cash value periodically. This means that, similar to a savings account, the cash value of the policy has the potential to accumulate and grow over time.

However, it’s important to note that the interest rates on an interest-sensitive whole life insurance policy are not guaranteed and may vary depending on market conditions. Additionally, the insurance company may impose certain fees and charges, such as administrative fees and mortality charges, which can affect the policy’s returns.

Interest-sensitive whole life insurance is often referred to by various names, including adjustable life, indexed universal life, or variable universal life insurance. While these names may differ slightly based on specific variations of the policy, the underlying concept remains the same – the ability to adjust premiums and death benefits while potentially earning interest on the policy’s cash value.

Now that we have a basic understanding of interest-sensitive whole life insurance, let’s explore its features and benefits in more detail to see if it’s the right option for you.

Definition of Interest-Sensitive Whole Life Insurance

Interest-sensitive whole life insurance is a type of life insurance policy that combines the features of traditional whole life insurance with the potential to earn interest on the policy’s cash value. It offers policyholders the opportunity to adjust their premiums and death benefits as their needs change, providing flexibility and possible growth.

At its core, interest-sensitive whole life insurance works by linking the policy’s cash value to an underlying interest-bearing account. This account is often tied to the performance of a market index, such as the S&P 500. The interest credited to the policy’s cash value is typically determined by the performance of this index, subject to certain limitations and fees.

Unlike other forms of life insurance, interest-sensitive whole life insurance allows policyholders to choose between different premium payment options. They can opt for a level premium, where the premium remains fixed throughout the life of the policy, or a flexible premium, where they have the flexibility to adjust their premiums over time.

Furthermore, the death benefit of an interest-sensitive whole life insurance policy can also be adjusted to suit the policyholder’s needs. Policyholders have the option to increase or decrease the death benefit, subject to certain conditions and limitations set by the insurance company.

One key feature of interest-sensitive whole life insurance is the potential for cash value accumulation. As the policyholder pays premiums, a portion of these payments is allocated to the policy’s cash value. Over time, this cash value can grow based on interest credited to the policy’s underlying account.

It’s important to note that the interest rates on an interest-sensitive whole life insurance policy are not guaranteed and can fluctuate based on market conditions. Policyholders should carefully review the terms and conditions of their policy to understand the potential risks and rewards associated with this type of insurance.

Interest-sensitive whole life insurance is often preferred by individuals who seek a combination of protection and potential growth. The flexibility in premium payments and death benefit adjustments makes it an appealing option for those with evolving financial needs.

Now that we have a clear understanding of interest-sensitive whole life insurance, let’s explore the features and benefits it offers compared to other types of life insurance.

Features and Benefits of Interest-Sensitive Whole Life Insurance

Interest-sensitive whole life insurance offers a range of features and benefits that make it a versatile and attractive option for individuals seeking both protection and potential growth. Let’s delve into some of the key features and benefits of interest-sensitive whole life insurance:

- Flexibility: One of the standout features of interest-sensitive whole life insurance is its flexibility. Policyholders have the option to adjust their premiums and death benefits as their financial needs change over time. This flexibility allows for greater control and customization, ensuring that the policy aligns with the policyholder’s evolving circumstances.

- Potential for Cash Value Growth: With interest-sensitive whole life insurance, the policy’s cash value has the potential to grow over time. The interest credited to the policy’s underlying investment account, which is often linked to a market index, can contribute to the accumulation of cash value. This growth can serve as a source of funds for various purposes, such as supplemental retirement income or emergency expenses.

- Tax Advantages: Another benefit of interest-sensitive whole life insurance is its potential tax advantages. The growth of the policy’s cash value is tax-deferred, meaning that policyholders do not have to pay taxes on the interest earned until they withdraw the funds. Additionally, the death benefit received by the beneficiaries is typically tax-free, providing valuable financial protection without the burden of taxation.

- Protection for Loved Ones: Like other forms of life insurance, interest-sensitive whole life insurance provides a death benefit that can offer financial protection to loved ones in the event of the policyholder’s death. This benefit can help cover funeral expenses, outstanding debts, mortgage payments, and provide ongoing financial support for beneficiaries, ensuring their financial security and peace of mind.

- Legacy Planning: Interest-sensitive whole life insurance can be an effective tool for legacy planning. The death benefit received by the beneficiaries can be used to leave a lasting financial legacy, support charitable causes, or provide for future generations. This allows policyholders to create a lasting impact and ensure their financial legacy lives on.

- Protection against Market Volatility: While interest-sensitive whole life insurance offers potential for growth through the underlying investment account, it also provides a level of protection against market volatility. The policy guarantees a minimum interest rate, ensuring that the cash value of the policy does not decrease, even if the underlying index performs poorly.

It’s important to note that the specific features and benefits of interest-sensitive whole life insurance may vary depending on the insurance company and policy terms. Policyholders should carefully review the policy documents and consult with a financial advisor to fully understand the details and make an informed decision.

Now that we have explored the features and benefits of interest-sensitive whole life insurance, let’s compare it with other types of life insurance to understand its unique advantages.

Comparison with Other Types of Life Insurance

When considering life insurance options, it’s essential to understand how interest-sensitive whole life insurance compares to other types of life insurance. Let’s compare interest-sensitive whole life insurance with two common types: term life insurance and traditional whole life insurance.

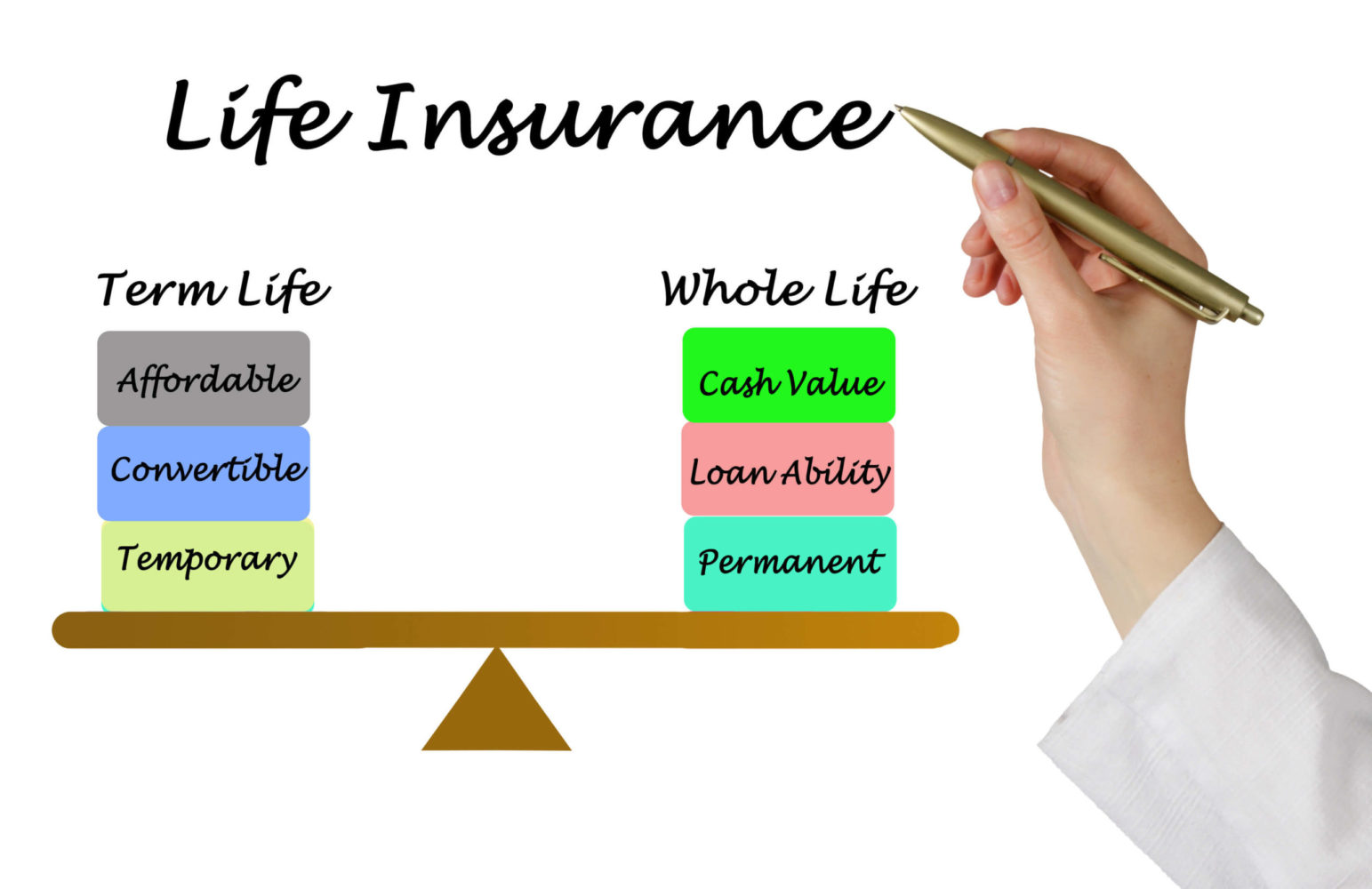

Term Life Insurance: Term life insurance provides coverage for a specific period, typically 10, 20, or 30 years. It offers a fixed death benefit and does not accumulate cash value. Unlike interest-sensitive whole life insurance, term life insurance does not provide potential growth or the flexibility to adjust premiums or death benefits. However, term life insurance premiums are generally lower, making it an affordable option for individuals seeking pure protection over a specific timeframe.

Traditional Whole Life Insurance: Traditional whole life insurance is a permanent life insurance policy that provides coverage for the policyholder’s entire life. It offers a fixed death benefit and builds cash value over time. Unlike interest-sensitive whole life insurance, traditional whole life insurance does not offer the same flexibility in adjusting premiums and death benefits. However, it guarantees a minimum cash value growth rate and may offer dividends, which can be used to increase the policy’s cash value or offset premiums.

Compared to both term life insurance and traditional whole life insurance, interest-sensitive whole life insurance offers a unique combination of features. It provides the potential for cash value growth, flexibility in premium payments and death benefit adjustments, and protection against market volatility. This makes it an appealing option for individuals who want both protection and potential long-term growth.

While interest-sensitive whole life insurance may have higher premiums compared to term life insurance, it offers the advantage of accumulating cash value over time. This cash value can be used for various purposes, such as supplementing retirement income or accessing funds during times of financial need.

Moreover, interest-sensitive whole life insurance provides policyholders with the ability to adjust their premiums and death benefits as their financial circumstances change. This flexibility ensures that the insurance coverage remains aligned with their evolving needs and goals.

It’s important to note that the right type of life insurance for an individual depends on their specific financial situation, goals, and risk tolerance. Consulting with a financial advisor can help determine the most suitable option.

Now that we have compared interest-sensitive whole life insurance with other types of life insurance, let’s explore the factors to consider when choosing interest-sensitive whole life insurance.

Factors to Consider when Choosing Interest-Sensitive Whole Life Insurance

Choosing the right interest-sensitive whole life insurance policy requires careful consideration of various factors. Here are some key factors to keep in mind when making a decision:

- Financial Goals: Determine your financial goals and objectives. Are you primarily seeking protection for your loved ones or are you also interested in potential cash value growth? Understanding your financial goals will help you select a policy that aligns with your needs.

- Risk Tolerance: Consider your risk tolerance. Interest-sensitive whole life insurance policies are linked to the performance of underlying investment accounts. These accounts may be subject to market volatility, which can impact the cash value growth. Assess your comfort level with market fluctuations and consider the guaranteed minimum interest rate provided by the policy.

- Flexibility Options: Evaluate the flexibility options offered by the policy. Interest-sensitive whole life insurance policies allow policyholders to adjust premiums and death benefits. Consider if these options align with your changing financial circumstances and long-term objectives.

- Insurance Company Reputation: Research the reputation and financial stability of the insurance company. Choose an established and reputable insurance provider with a strong track record in the industry. This ensures that your policy is backed by a financially secure company that can fulfill its obligations in the future.

- Policy Costs: Understand the costs associated with the policy. Evaluate the premiums, fees, and charges related to the interest-sensitive whole life insurance policy. Compare these costs with similar policies from different insurance companies to ensure you are getting a competitive and fair deal.

- Policy Illustrations: Request policy illustrations from multiple insurance companies. These illustrations provide projections of the policy’s performance based on various assumptions. Review the illustrations carefully, paying attention to growth potential, fees, and potential risks.

- Expert Advice: Seek guidance from a qualified financial advisor or insurance professional. They can help you navigate through the complexities of interest-sensitive whole life insurance and make an informed decision based on your specific financial situation and goals.

By considering these factors, you can make a well-informed decision when choosing an interest-sensitive whole life insurance policy that aligns with your needs and financial objectives.

Now that we have explored the factors to consider, it’s time to summarize our findings.

Conclusion

Interest-sensitive whole life insurance offers a unique blend of protection and potential growth, making it an appealing option for individuals seeking flexibility and long-term financial security. By linking the policy’s cash value to an underlying interest-bearing account, policyholders have the opportunity to accumulate wealth over time, while also having the flexibility to adjust premiums and death benefits as their needs change.

When comparing interest-sensitive whole life insurance to other types of life insurance, it stands out for its potential cash value growth and protection against market volatility. However, it’s essential to consider factors such as financial goals, risk tolerance, flexibility options, insurance company reputation, policy costs, policy illustrations, and seeking expert advice when making a decision.

Interest-sensitive whole life insurance can provide valuable benefits such as tax advantages, legacy planning, and protection for loved ones. However, it may come with higher premiums compared to term life insurance and limited flexibility compared to traditional whole life insurance.

Ultimately, the choice of interest-sensitive whole life insurance depends on your individual financial situation, goals, and risk tolerance. Taking the time to carefully evaluate your needs and consult with a financial advisor will help you make an informed decision.

Remember, interest-sensitive whole life insurance can offer both protection and growth potential, providing financial security for you and your loved ones. So, take the necessary steps to understand the policy’s features, compare different options, and choose the right interest-sensitive whole life insurance policy that suits your unique needs.

Now that you have a deeper understanding of interest-sensitive whole life insurance, you can confidently explore this option and make a well-informed decision to secure your financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance