Finance

What Is FICO Score 8

Published: March 6, 2024

Learn about FICO Score 8 and its impact on your finances. Understand how this credit scoring model affects your financial opportunities.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the realm of personal finance, one's credit score holds substantial significance. It is a numerical representation of an individual's creditworthiness and is utilized by lenders to assess the risk associated with extending credit. Among the various credit scoring models, the FICO Score 8 stands out as a widely utilized and influential metric in the lending industry.

Understanding the intricacies of the FICO Score 8 is essential for anyone seeking to comprehend the factors that shape their credit profile and the potential impact on their financial opportunities. This comprehensive guide aims to demystify the FICO Score 8, shedding light on its calculation, significance, influencing factors, and practical implications.

A deep dive into the FICO Score 8 will not only equip individuals with the knowledge to manage and improve their credit standing but also empower them to make informed decisions when navigating the complex landscape of personal finance. Whether you are contemplating a major loan application or striving to enhance your financial health, grasping the nuances of the FICO Score 8 is a pivotal step toward achieving your goals.

What is FICO Score 8?

The FICO Score 8 is a credit scoring model developed by the Fair Isaac Corporation (FICO), a leading analytics company in the financial services industry. This scoring model serves as a tool for evaluating an individual’s credit risk and is widely used by lenders to make informed decisions regarding loan approvals, interest rates, and credit limits.

Unlike earlier versions of the FICO Score, the FICO Score 8 incorporates several refinements that aim to provide a more accurate and holistic assessment of a consumer’s creditworthiness. One notable feature of the FICO Score 8 is its emphasis on the impact of credit utilization, making it crucial for individuals to maintain low credit card balances relative to their credit limits.

Furthermore, the FICO Score 8 takes into account the overall credit history, payment behavior, credit mix, and new credit inquiries of an individual. This comprehensive evaluation enables lenders to gauge the likelihood of a borrower repaying debts responsibly, thereby influencing their lending decisions.

It is important to note that the FICO Score 8 is utilized by a wide array of lenders, including mortgage providers, credit card issuers, and auto loan financiers. As such, the score holds substantial sway over an individual’s financial prospects, impacting their access to credit and the terms associated with borrowing.

Given its widespread adoption and influence, understanding the nuances of the FICO Score 8 is pivotal for individuals aiming to comprehend their credit standing and take proactive steps to manage and improve it.

How is FICO Score 8 Calculated?

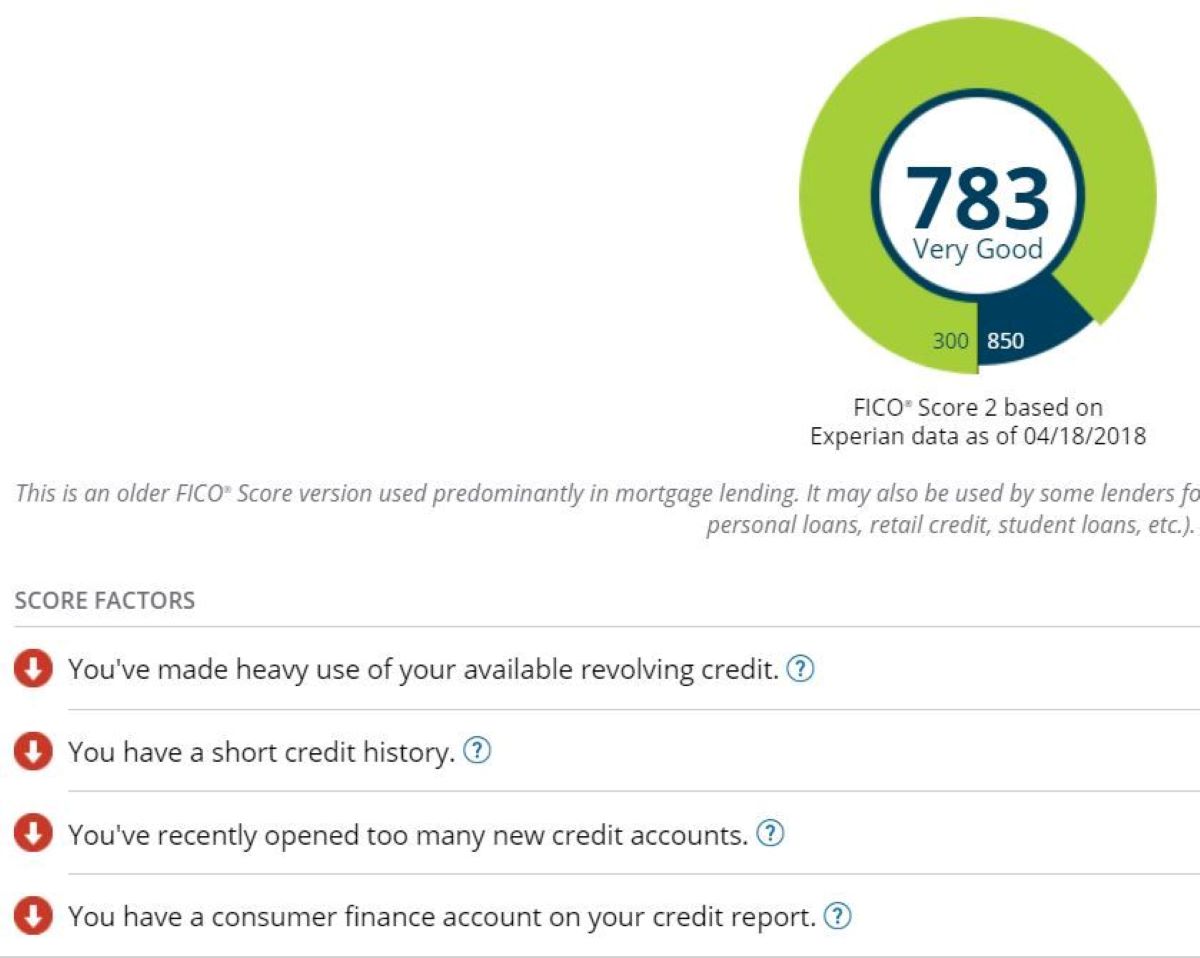

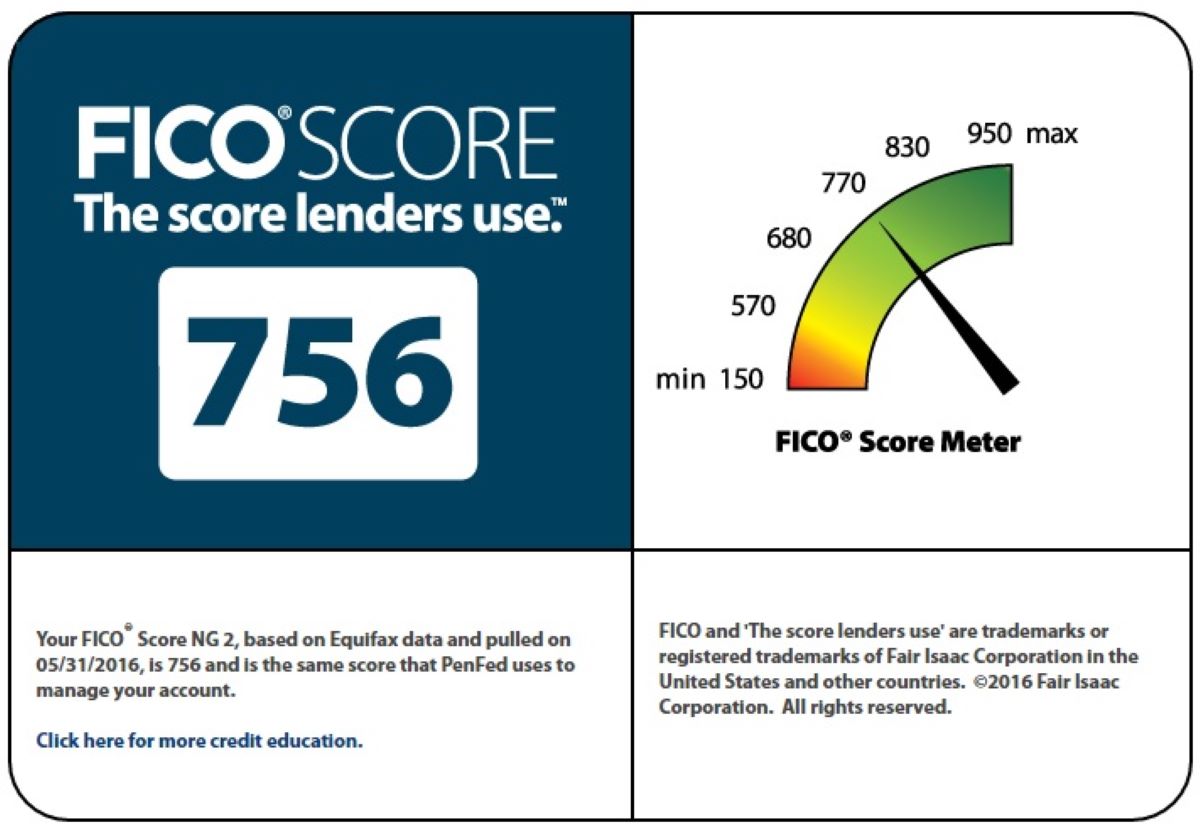

The calculation of the FICO Score 8 involves a sophisticated algorithm that analyzes various components of an individual’s credit history to generate a three-digit score ranging from 300 to 850. This score serves as a pivotal indicator of the individual’s creditworthiness and is utilized by lenders to assess the risk associated with extending credit.

The key factors considered in the calculation of the FICO Score 8 include:

- Payment History: This component holds significant weight in the calculation and reflects an individual’s track record of making on-time payments for credit accounts, including loans and credit cards.

- Credit Utilization: The ratio of credit card balances to credit limits is a crucial factor, with lower utilization indicative of responsible credit management.

- Length of Credit History: The duration for which credit accounts have been open and the time since the most recent account activity are taken into account, providing insights into the individual’s credit management over time.

- New Credit Inquiries: The number of recent credit inquiries and newly opened accounts can impact the score, as multiple inquiries within a short period may signal higher risk.

- Credit Mix: A diverse mix of credit accounts, such as credit cards, mortgages, and installment loans, can positively influence the score, reflecting responsible credit usage across various financial products.

It is important to note that the weight assigned to each factor may vary based on the individual’s unique credit profile. The FICO Score 8 algorithm leverages these components to generate a comprehensive assessment of the individual’s credit risk, culminating in the assignment of a numerical score that holds substantial sway over their financial opportunities.

By comprehending the intricacies of the FICO Score 8 calculation, individuals can gain insights into the specific areas of their credit history that impact their score and take proactive measures to strengthen their credit profile, thereby enhancing their financial prospects.

Importance of FICO Score 8

The FICO Score 8 holds immense importance in the realm of personal finance, exerting a profound impact on an individual’s financial opportunities and the terms associated with credit products. Understanding the significance of this credit scoring model is crucial for individuals aiming to navigate the lending landscape and harness their financial potential.

Key facets underscoring the importance of the FICO Score 8 include:

- Lending Decisions: Lenders across diverse financial sectors, including mortgage providers, credit card issuers, and auto loan financiers, rely on the FICO Score 8 to assess the creditworthiness of applicants. The score plays a pivotal role in determining the approval of loan applications, interest rates, and credit limits, thereby influencing an individual’s access to credit.

- Interest Rates: The FICO Score 8 often serves as a determining factor in setting the interest rates for approved credit products. Individuals with higher scores are typically offered more favorable interest rates, translating to reduced borrowing costs over the life of the loan.

- Access to Credit: A robust FICO Score 8 can expand an individual’s access to credit, enabling them to secure favorable terms on loans and credit lines. Conversely, a lower score may limit access to credit or result in higher costs associated with borrowing.

- Financial Opportunities: The FICO Score 8 directly impacts an individual’s ability to seize financial opportunities, such as obtaining a mortgage for a home purchase, securing a competitive credit card with enticing rewards, or accessing affordable auto financing.

Furthermore, the FICO Score 8 serves as a barometer of an individual’s financial responsibility and credit management prowess. It reflects their track record of repaying debts, managing credit accounts, and navigating the financial landscape, thereby influencing the trust placed in them by potential lenders.

By recognizing the pivotal role of the FICO Score 8, individuals can proactively manage their credit profiles, cultivate healthy financial habits, and strive to elevate their scores, thereby unlocking enhanced financial opportunities and paving the way toward a more secure and prosperous financial future.

Factors Affecting FICO Score 8

The FICO Score 8 is influenced by a range of factors that collectively shape an individual’s credit profile and ultimately determine their creditworthiness. Understanding these factors is essential for individuals seeking to comprehend the dynamics of their credit scores and take proactive steps to manage and improve them.

Key factors that impact the FICO Score 8 include:

- Payment History: Timely payment of credit obligations is a critical factor influencing the FICO Score 8. Consistent on-time payments contribute positively to the score, while late payments, defaults, and accounts in collections can have adverse effects.

- Credit Utilization: The ratio of credit card balances to credit limits plays a pivotal role in the FICO Score 8 calculation. Maintaining low utilization, ideally below 30% of available credit, is advisable to positively impact the score.

- Length of Credit History: The duration for which credit accounts have been established and the average age of accounts contribute to the FICO Score 8. A longer credit history, coupled with responsible credit management over time, can bolster the score.

- New Credit Inquiries: Recent credit inquiries and the opening of new credit accounts can influence the FICO Score 8. Multiple inquiries within a short period may signal higher risk to potential lenders.

- Credit Mix: A diverse mix of credit accounts, including credit cards, mortgages, and installment loans, can positively impact the FICO Score 8 by showcasing responsible management of various credit products.

It is important to recognize that these factors are interwoven and collectively contribute to the overall assessment of an individual’s creditworthiness. Moreover, the weight assigned to each factor may vary based on the unique characteristics of an individual’s credit profile, thereby influencing the impact of these factors on their FICO Score 8.

By comprehending the nuanced interplay of these factors, individuals can strategically manage their credit behaviors, cultivate healthy financial habits, and make informed decisions to positively influence their FICO Score 8. Proactive credit management, responsible borrowing, and prudent financial choices can collectively contribute to enhancing the factors that underpin the FICO Score 8, thereby fortifying an individual’s credit standing and expanding their financial opportunities.

Benefits of FICO Score 8

The FICO Score 8 offers a multitude of benefits that extend beyond its role as a numerical representation of an individual’s creditworthiness. Understanding these advantages is crucial for individuals aiming to leverage the FICO Score 8 to their advantage and harness its potential to unlock enhanced financial opportunities.

Key benefits of the FICO Score 8 include:

- Standardized Evaluation: The FICO Score 8 provides a standardized and widely recognized metric for assessing an individual’s credit risk, enabling lenders to make consistent and informed lending decisions across various credit products.

- Transparent Assessment: Individuals can gain insights into the key factors influencing their credit scores, as the FICO Score 8 algorithm considers specific components of their credit history, empowering them to comprehend their credit standing and take proactive measures to improve it.

- Impact on Interest Rates: A robust FICO Score 8 can translate to lower interest rates on approved credit products, potentially resulting in significant cost savings over the life of loans and credit lines.

- Enhanced Access to Credit: Individuals with favorable FICO Score 8 ratings are more likely to qualify for a diverse range of credit products, including mortgages, auto loans, and credit cards, with favorable terms and higher credit limits.

- Financial Empowerment: A strong FICO Score 8 can empower individuals to seize financial opportunities, such as securing competitive mortgage rates, accessing premium credit card offerings, and obtaining favorable terms on personal loans, thereby enhancing their financial well-being.

Moreover, the FICO Score 8 serves as a tool for fostering financial accountability and incentivizing responsible credit management. By recognizing the benefits of a robust credit score, individuals are encouraged to cultivate healthy financial habits, maintain disciplined credit behaviors, and make informed decisions to bolster their credit profiles.

Ultimately, the FICO Score 8 not only serves as a barometer of creditworthiness but also as a catalyst for financial empowerment, enabling individuals to navigate the lending landscape with confidence, access credit on favorable terms, and embark on a path toward greater financial resilience and prosperity.

Limitations of FICO Score 8

While the FICO Score 8 is a widely utilized and influential credit scoring model, it is important to acknowledge its limitations, as these aspects can impact individuals’ credit experiences and lending opportunities.

Key limitations of the FICO Score 8 include:

- Scoring Model Variations: Lenders may use different versions of the FICO Score or alternative credit scoring models, leading to variations in the scores provided to consumers. This can result in discrepancies in credit assessments across different lenders and credit bureaus.

- Limited Scope: The FICO Score 8 may not fully capture an individual’s creditworthiness, particularly for those with limited credit histories or unique financial circumstances. This can pose challenges for individuals seeking to establish credit or demonstrate their creditworthiness through non-traditional financial behaviors.

- Influence of Negative Events: Adverse credit events, such as delinquencies, defaults, or bankruptcies, can significantly impact the FICO Score 8, potentially overshadowing an individual’s positive credit behaviors and hindering their access to credit.

- Dynamic Credit Factors: The FICO Score 8 algorithm may not instantaneously reflect changes in an individual’s credit behaviors or financial circumstances, leading to delays in score adjustments that align with their current credit management practices.

- Impact of Economic Conditions: External economic factors, such as recessions or financial crises, can influence credit behaviors and, subsequently, the FICO Score 8. Individuals may experience score fluctuations due to broader economic trends beyond their control.

It is crucial for individuals to recognize these limitations and take proactive measures to mitigate their impact on their credit experiences. This includes maintaining open communication with lenders, regularly monitoring credit reports, and seeking opportunities to build robust credit profiles beyond the scope of traditional credit scoring models.

Furthermore, understanding the limitations of the FICO Score 8 can prompt individuals to explore alternative credit-building strategies, such as responsible use of secured credit cards, credit builder loans, and alternative data sources, to showcase their creditworthiness and enhance their financial prospects.

By acknowledging these limitations and adopting a proactive approach to credit management, individuals can navigate the complexities of credit scoring with resilience, embracing opportunities to fortify their credit profiles and pursue their financial goals with confidence.

Conclusion

The FICO Score 8 stands as a cornerstone of the modern credit landscape, wielding significant influence over individuals’ access to credit and the terms associated with borrowing. Understanding the intricacies of this credit scoring model is pivotal for anyone seeking to navigate the realm of personal finance with confidence and foresight.

By delving into the nuances of the FICO Score 8, individuals can gain insights into the factors that shape their credit profiles, the impact of their credit behaviors, and the avenues for cultivating healthy financial habits. Armed with this knowledge, they can proactively manage their credit standing, pursue opportunities to strengthen their creditworthiness, and make informed decisions that resonate with their long-term financial aspirations.

Moreover, recognizing the benefits and limitations of the FICO Score 8 empowers individuals to approach credit management with resilience and adaptability. It encourages them to explore diverse credit-building strategies, engage in open dialogue with lenders, and embrace holistic approaches to financial well-being that extend beyond traditional credit scoring models.

Ultimately, the FICO Score 8 serves as more than a numerical assessment of credit risk; it embodies a pathway toward financial empowerment, resilience, and informed decision-making. By leveraging the insights gleaned from this comprehensive guide, individuals can embark on a journey toward a more secure and prosperous financial future, underpinned by a deep understanding of their credit standing and the mechanisms that drive their financial opportunities.

As individuals harness the knowledge encapsulated within the realm of the FICO Score 8, they are poised to navigate the complexities of credit with confidence, seize opportunities for credit enhancement, and chart a course toward enduring financial well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance