Home>Finance>What Type Of Life Insurance Policy Generates Immediate Cash Value?

Finance

What Type Of Life Insurance Policy Generates Immediate Cash Value?

Published: October 14, 2023

Looking for a life insurance policy that provides immediate cash value? Explore finance-focused options to secure your financial future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Life insurance is an essential financial tool that provides protection and financial security to your loved ones in the event of your untimely death. It serves as a safety net, ensuring that your family’s financial needs are met even after you are no longer around to provide for them.

When it comes to life insurance policies, there are various types available in the market. Each type has its own unique features and benefits. One of the key differentiating factors between these policies is the generation of immediate cash value.

In this article, we will explore the different types of life insurance policies that generate immediate cash value. We will delve into each policy’s characteristics, benefits, and considerations, helping you make an informed decision based on your individual needs and financial goals.

Whether you are looking for a policy that builds cash value over time or one that provides immediate liquidity, understanding the different options available will empower you to make a choice that aligns with your financial objectives.

So, let’s dive into the various types of life insurance policies and discover which ones can generate immediate cash value.

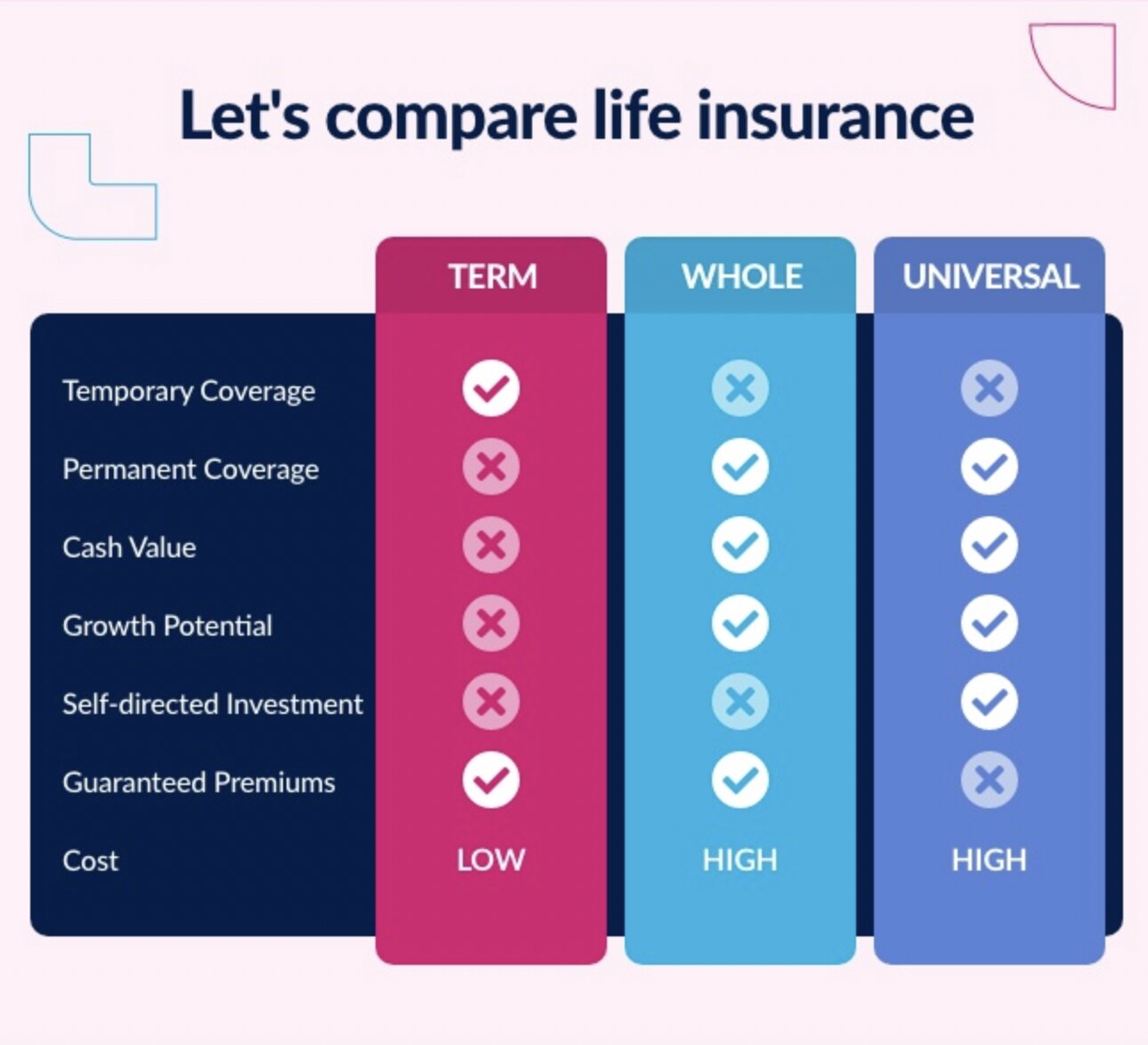

Term Life Insurance

Term life insurance is a type of life insurance policy that offers coverage for a specific period or term, usually ranging from 10 to 30 years. It provides a death benefit to your beneficiaries if you pass away within the term of the policy. Unlike other types of life insurance, term life insurance generally does not accumulate cash value.

This means that term life insurance policies typically do not generate immediate cash value. The premiums you pay go towards the cost of providing the death benefit coverage, without any component allocated to accumulating cash value.

Term life insurance is a popular choice for individuals who want affordable coverage for a specific period. It is often purchased to provide financial protection during the years when your loved ones may be most dependent on your income, such as when you have young children or outstanding debts.

While term life insurance does not build cash value over time, its main advantage lies in its affordability. Since it does not have the investment component that generates cash value, the premiums for term life insurance policies tend to be lower compared to other types of life insurance.

Term life insurance is a straightforward and transparent form of coverage. You pay a fixed premium for a predetermined period, and if you pass away during that period, your beneficiaries receive the death benefit. Once the term expires, the coverage ends, and there is no cash value or residual benefit.

It’s important to note that some term life insurance policies have a convertible option, which allows you to convert the policy to a permanent life insurance policy in the future. This can be beneficial if your needs change and you want to have a policy that has the potential to generate immediate cash value.

In summary, while term life insurance is an affordable and straightforward way to provide temporary protection for your loved ones, it typically does not generate immediate cash value. If you are looking for a policy that offers cash value accumulation, you may need to explore other types of life insurance, such as whole life, universal life, or variable life insurance.

Whole Life Insurance

Whole life insurance is a type of permanent life insurance that provides coverage for your entire lifetime, as long as you continue to pay the premiums. One of the key features of whole life insurance is that it has the potential to generate immediate cash value.

With whole life insurance, a portion of the premium you pay goes towards the cost of the death benefit coverage, while the remaining portion is allocated toward an investment component called the cash value. This cash value has the potential to grow over time, generating immediate cash value that you can access during your lifetime.

The cash value within a whole life insurance policy accumulates on a tax-deferred basis. It grows over time based on a guaranteed rate of return set by the insurance company, and in some cases, it may also have a participating feature that allows you to earn dividends.

There are several ways to access the cash value of a whole life insurance policy. You can take out a policy loan against the cash value, use it to pay premiums, or even surrender the policy and receive the accumulated cash value. However, it’s important to note that withdrawing or borrowing against the cash value can reduce the death benefit and may have tax implications.

One of the key advantages of whole life insurance is that it provides lifelong coverage with the potential for cash value growth. It offers a combination of protection and savings, making it a popular choice for individuals who want to build up assets over time and have a safety net for their loved ones.

Whole life insurance policies also typically offer level premiums, meaning that your premium remains constant throughout the life of the policy. This can provide peace of mind, knowing that your premium will not increase as you age or if your health deteriorates.

While whole life insurance offers the benefit of immediate cash value, it’s important to consider that it is generally more expensive than term life insurance. The premiums are higher because a portion of the premium goes towards building the cash value component.

In summary, whole life insurance is a type of permanent life insurance that has the potential to generate immediate cash value. It provides lifelong coverage and combines protection with cash value growth. If you are looking for a life insurance policy that offers immediate liquidity and long-term savings potential, whole life insurance may be the right choice for you.

Universal Life Insurance

Universal life insurance is another type of permanent life insurance that offers flexibility and the potential to generate immediate cash value. It combines a death benefit with a savings component, providing you with lifelong coverage and the opportunity to accumulate cash value over time.

With universal life insurance, a portion of the premium you pay goes towards the cost of the death benefit coverage, while the remaining portion is allocated to an investment account known as the cash value. The cash value grows based on the performance of the underlying investments, such as stocks, bonds, or money market funds. This means that the accumulation of cash value is dependent on the market performance of the chosen investments.

One of the key features of universal life insurance is its flexibility. You have the ability to adjust your premium payments and death benefit coverage amount, within certain limits, to meet your changing needs and financial goals. You can also use the accumulated cash value to cover premiums or take out loans against the cash value.

Unlike whole life insurance, which typically offers a guaranteed rate of return, the cash value growth in universal life insurance is linked to the market performance of the underlying investments. This means that there is potential for higher returns but also higher risk compared to whole life insurance.

Universal life insurance policies may offer different options for how the cash value is invested. These options can include fixed interest accounts, index accounts that track a specific market index, or variable accounts that allow you to choose from a selection of investment options. The choice of investment options will depend on your risk tolerance and investment preferences.

It’s important to monitor the performance of the cash value in a universal life insurance policy, as poor investment performance can impact the growth and sustainability of the policy. If the cash value does not perform well, it may require additional premium payments to maintain the desired level of coverage.

Universal life insurance offers the advantage of flexibility and the potential for cash value growth. It allows you to adjust your coverage and premium payments as your financial situation changes. However, it’s crucial to work closely with your insurance agent or financial advisor to ensure that the policy is properly managed and meets your long-term financial goals.

In summary, universal life insurance is a type of permanent life insurance that provides lifelong coverage and the opportunity to accumulate cash value through investments. It offers flexibility in premium payments and death benefit coverage, but the performance of the cash value is dependent on the market performance of the underlying investments. If you are comfortable with market fluctuations and want the potential for higher returns, universal life insurance may be a suitable option for you.

Variable Life Insurance

Variable life insurance is a type of permanent life insurance that offers both a death benefit and the potential for immediate cash value growth through investment options. It combines the protection of a life insurance policy with the opportunity to invest in a variety of investment vehicles, such as stocks, bonds, and mutual funds.

With variable life insurance, a portion of the premium you pay goes towards the cost of the death benefit coverage, while the remaining portion is allocated to the investment component, known as the cash value. Unlike other types of life insurance, variable life insurance policies allow you to choose from a selection of investment options within the policy.

The cash value within a variable life insurance policy fluctuates based on the performance of the underlying investments. As the investments grow, so does the cash value. However, it’s important to note that poor investment performance can also lead to a decrease in the cash value. This means that the accumulation of cash value is subject to market volatility and carries a higher level of risk compared to other types of life insurance.

Variable life insurance policies offer transparency and control over investment choices. You have the ability to allocate your premium payments to different investment options based on your risk tolerance and investment preferences. This flexibility allows you to take advantage of market opportunities and potentially earn higher returns.

It’s important to note that variable life insurance policies come with certain fees and expenses, such as administrative fees and investment management fees. These costs can impact the overall returns of the policy and should be carefully considered when evaluating the suitability of variable life insurance for your financial needs.

Variable life insurance policies also typically offer a death benefit that can be adjusted over time, providing flexibility to tailor the coverage to your changing needs. However, it’s important to ensure that the cash value is sufficient to sustain the policy, as poor investment performance or high fees can deplete the cash value and jeopardize the policy’s longevity.

Variable life insurance can be a suitable option for individuals who are comfortable with investment risk and want the potential for higher returns. It offers the combination of death benefit coverage and the opportunity to build cash value through investment options. However, it’s important to work closely with your insurance agent or financial advisor to ensure that the investment choices align with your risk tolerance and long-term financial goals.

In summary, variable life insurance is a type of permanent life insurance that offers a death benefit and the potential for immediate cash value growth through a selection of investment options. It provides flexibility and control over investment choices, but it carries a higher level of investment risk compared to other types of life insurance. If you are comfortable with market fluctuations and want the potential for higher returns, variable life insurance may be a suitable option for you.

Indexed Universal Life Insurance

Indexed universal life insurance (IUL) is a type of permanent life insurance policy that offers both a death benefit and the potential for immediate cash value growth tied to the performance of a stock market index, such as the S&P 500. It combines the financial protection of a life insurance policy with the potential for investment growth.

With indexed universal life insurance, a portion of your premium payments goes towards the cost of the death benefit coverage, while the remaining portion is allocated to an indexed account. The indexed account earns interest based on the performance of the chosen stock market index, with a minimum guaranteed interest rate set by the insurance company.

The cash value within an indexed universal life insurance policy grows based on the positive performance of the stock market index. This means that if the index experiences growth, your cash value will also increase. However, if the index performs poorly, your cash value will still be protected by the guaranteed minimum interest rate, ensuring that it doesn’t decrease.

IUL policies typically come with a cap or participation rate that limits the maximum amount of interest that can be credited to the cash value. This ensures a balance between potential growth and protection from market downturns. Additionally, IUL policies may also offer a floor or guaranteed minimum interest rate to safeguard against negative index performance.

One of the main advantages of indexed universal life insurance is its flexibility. You have the ability to adjust your premium payments and death benefit coverage amount, within certain limits, to suit your changing financial needs. This flexibility allows you to adapt the policy as your circumstances evolve over time.

Additionally, the cash value within an indexed universal life insurance policy can be accessed through policy loans or withdrawals, providing you with a source of funds for various expenses such as education, emergencies, or retirement. However, it’s important to consider the potential impact on the death benefit and the tax consequences of accessing the cash value.

Indexed universal life insurance can be suitable for individuals looking for a balance between potential investment growth and downside protection. It offers the potential for cash value growth tied to the performance of a stock market index, while also providing a level of guaranteed minimum interest. However, it’s important to carefully evaluate the policy’s terms, fees, and potential risks before making a decision.

In summary, indexed universal life insurance is a type of permanent life insurance that offers both a death benefit and the potential for immediate cash value growth tied to the performance of a stock market index. It provides flexibility, downside protection, and the opportunity to accumulate cash value over time. If you are comfortable with market fluctuations and want the potential for growth while maintaining a level of protection, indexed universal life insurance may be a suitable option for you.

Conclusion

When it comes to life insurance policies, it’s important to understand the different types available and their ability to generate immediate cash value. Term life insurance, although it provides essential coverage, typically does not generate immediate cash value. On the other hand, permanent life insurance policies such as whole life insurance, universal life insurance, variable life insurance, and indexed universal life insurance offer the potential for immediate cash value growth.

Whole life insurance provides lifelong coverage and the potential for cash value accumulation on a guaranteed basis. Universal life insurance offers flexibility in premium payments and the potential for cash value growth based on investments. Variable life insurance allows you to choose from a variety of investment options to potentially grow the cash value. Indexed universal life insurance ties the cash value growth to the performance of a stock market index.

Each type of permanent life insurance has its own unique features and considerations. Therefore, it’s essential to carefully evaluate your financial goals, risk tolerance, and long-term objectives when choosing a life insurance policy that generates immediate cash value.

Whether you are looking for a policy that provides lifelong coverage, the ability to adjust your premium payments, or potential growth through investments, there is a life insurance option available to suit your needs.

Remember to consult with a qualified insurance agent or financial advisor to assess your specific situation and find the best life insurance policy that aligns with your financial goals. They can provide personalized guidance and help you navigate the features, benefits, and risks associated with each type of life insurance.

Ultimately, life insurance is an important financial tool that provides security and peace of mind for you and your loved ones. By understanding the different types of life insurance policies that generate immediate cash value, you can make an informed decision and secure a brighter financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance