Home>Finance>When A Financial Institusion Buys Futures Contracts

Finance

When A Financial Institusion Buys Futures Contracts

Modified: February 21, 2024

Learn how financial institutions utilize futures contracts in their investment strategies and manage risk in the finance industry

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Futures Contracts

- Purpose of Financial Institutions Buying Futures Contracts

- Potential Benefits of Buying Futures Contracts

- Risks Involved in Buying Futures Contracts

- Factors Considered by Financial Institutions When Buying Futures Contracts

- Examples of Financial Institutions Buying Futures Contracts

- Conclusion

Introduction

In the ever-evolving world of finance, financial institutions play a pivotal role in managing and leveraging various investment instruments to achieve their goals. One such instrument that these institutions often utilize is futures contracts. Buying futures contracts allows financial institutions to take advantage of the price movements of commodities, currencies, or financial instruments in the future.

In simple terms, a futures contract is an agreement between two parties to buy or sell an asset at a predetermined price on a specified future date. These contracts are traded on futures exchanges, providing a standardized platform for investors to engage in buying and selling.

Financial institutions, including banks, investment firms, and hedge funds, are actively involved in buying futures contracts to hedge their risks, speculate on price movements, or create additional investment opportunities for their clients. By participating in futures markets, these institutions demonstrate their expertise in managing risks and capitalizing on potential gains.

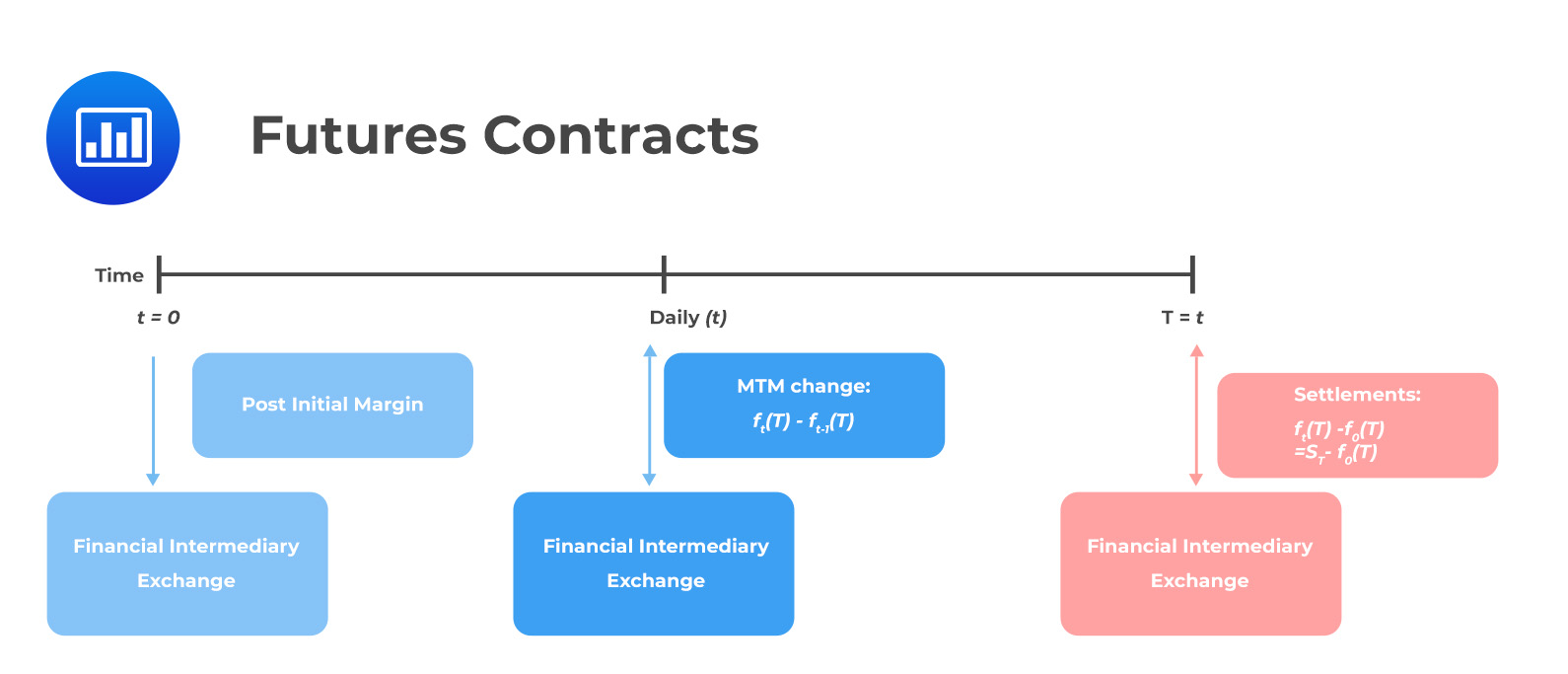

When financial institutions buy futures contracts, they enter into a binding agreement to either buy or sell the underlying asset at a predetermined price, known as the futures price, on the contract’s maturity date. This transaction is facilitated through a clearinghouse, ensuring the smooth settlement of trades and minimizing counterparty risk.

The primary reason for financial institutions to buy futures contracts is to mitigate risk exposure. By locking in prices today, they can protect themselves against the potential adverse movements in prices that may occur in the future. This is particularly crucial for institutions dealing with price-sensitive commodities or currencies.

In addition to risk management, financial institutions also seek potential benefits from buying futures contracts. Through speculation, institutions take positions based on their market analysis and forecast future price movements. If their predictions are correct, they can profit from the price differentials and generate substantial returns for their investment portfolios.

However, it’s essential to note that buying futures contracts is not without its risks. The volatility of futures markets can expose financial institutions to significant losses if prices move against their positions. Therefore, thorough analysis, research, and risk management strategies are crucial to mitigate potential downsides.

As financial institutions evaluate and decide to buy futures contracts, they consider various factors, such as market conditions, regulations, liquidity, and the objectives of their clients. By understanding these factors, institutions can formulate effective strategies and make informed decisions on which futures contract to buy.

Let’s explore in more detail the potential benefits, risks, and factors that financial institutions consider when buying futures contracts, using real-world examples to illustrate their application in practice.

Definition of Futures Contracts

Before delving into the intricacies of financial institutions buying futures contracts, it is essential to understand the fundamental concept of futures contracts.

A futures contract is a standardized agreement between two parties to buy or sell a specific asset at a predetermined price (referred to as the “futures price”) on a specified future date. The assets underlying futures contracts can vary widely, including commodities like crude oil, gold, or agricultural products, currencies, interest rates, or stock market indices.

Unlike options contracts, which give the buyer the right but not the obligation to buy or sell the asset, futures contracts create a binding obligation for both parties involved. This means that the buyer must buy, and the seller must sell, the underlying asset at the agreed-upon price and date.

Futures contracts are primarily traded on organized exchanges, such as the Chicago Mercantile Exchange (CME) or the Intercontinental Exchange (ICE), where standardized contract specifications are established. These specifications include the size of the contract, the unit of measurement, the delivery months, and the minimum price fluctuations.

Financial institutions rely on these standardized contracts as they provide liquidity and a transparent marketplace for buying and selling futures contracts. This facilitates efficient price discovery and ensures the smooth settlement of trades through the exchange’s clearinghouse.

Furthermore, futures contracts have a finite duration, typically with standardized expiration dates. At the expiry of the contract, the agreed-upon transaction takes place between the buyer and the seller, either through physical delivery of the underlying asset (in the case of commodity futures) or through a cash settlement based on the price difference (in the case of financial futures).

The concept of futures contracts stems from the need to manage and hedge risk in various industries. For example, commodity producers, such as farmers or oil companies, can use futures contracts to secure a fixed price for their products, protecting them from price fluctuations. On the other hand, speculators or investors can take positions in futures contracts to capitalize on anticipated price movements and generate profits.

It is important to note that futures contracts are highly leveraged instruments. This means that traders can control a large position with a fraction of the total contract value, known as the margin requirement. This leverage amplifies both potential profits and losses, making futures trading a high-risk endeavor.

Financial institutions play a significant role in the futures markets. Their participation brings liquidity, stability, and expert analysis to the marketplace. By understanding the fundamental nature of futures contracts, financial institutions can effectively utilize these instruments to achieve their investment objectives.

Purpose of Financial Institutions Buying Futures Contracts

Financial institutions engage in buying futures contracts for a variety of purposes, often driven by their investment strategies, risk management, and client requirements. Let’s explore the main purposes behind financial institutions’ decision to buy futures contracts.

1. Risk Management: One of the primary reasons financial institutions buy futures contracts is to manage and hedge their exposure to price volatility. By entering into a futures contract, institutions can lock in prices today, mitigating the risk of adverse price movements in the future. For example, airlines may buy futures contracts to hedge against rising jet fuel prices, ensuring predictable costs for their operations. Similarly, agricultural companies might purchase futures contracts to hedge against potential fluctuations in crop prices.

2. Speculation: Financial institutions with expertise in market analysis and forecasting may utilize futures contracts for speculative purposes. By taking positions based on their predictions of future price movements, institutions aim to profit from the price differentials. Speculation in futures contracts can provide opportunities for significant returns if the market moves in the expected direction.

3. Arbitrage: Arbitrage is the practice of taking advantage of price discrepancies between different markets. Financial institutions may engage in buying futures contracts to capitalize on arbitrage opportunities. For example, if a particular asset is trading at a lower price in the futures market compared to the spot market, institutions can buy futures contracts and simultaneously sell the underlying asset to lock in a risk-free profit.

4. Portfolio Diversification: Financial institutions aim to diversify their investment portfolios to reduce overall risk. By including futures contracts in their portfolios, institutions can achieve exposure to varied asset classes and sectors. This diversification allows them to spread risk and potentially enhance long-term returns.

5. Liquidity Management: Financial institutions often face the challenge of managing their liquidity and optimizing the utilization of available funds. By buying futures contracts, they can allocate funds to investment opportunities that provide potential returns, while maintaining liquidity for other operational and strategic needs. Futures contracts offer the flexibility to adjust positions and exit trades relatively quickly compared to other long-term investments.

6. Client Requirements: Financial institutions serve diverse clients with specific investment objectives and risk profiles. Buying futures contracts allows institutions to meet the investment needs of their clients by providing exposure to specific asset classes or sectors. For example, a pension fund may require exposure to commodities as part of their investment strategy, and a financial institution can fulfill this requirement by purchasing futures contracts on behalf of the fund.

Overall, the purpose of financial institutions buying futures contracts extends beyond mere speculation. They utilize these instruments strategically to manage risk, capitalize on opportunities, diversify portfolios, and meet client requirements. By employing futures contracts, financial institutions demonstrate their ability to navigate the complexities of financial markets and drive optimal outcomes for their stakeholders.

Potential Benefits of Buying Futures Contracts

Financial institutions derive several potential benefits from buying futures contracts as part of their investment strategies. These benefits include risk management, potential profit opportunities, cost efficiency, and increased market access. Let’s explore these benefits in more detail:

1. Risk Management: Buying futures contracts enables financial institutions to effectively manage and hedge their exposure to price fluctuations. By locking in prices today, institutions can protect themselves against potential adverse moves in the future. This risk management tool is particularly valuable for institutions dealing with price-sensitive assets like commodities or currencies.

2. Speculative Opportunities: Financial institutions with in-depth market analysis and forecasting capabilities can capitalize on futures contracts as a speculative investment. By taking positions based on their predictions of future price movements, institutions can potentially generate significant profits. Successful speculation in futures contracts relies on accurate market analysis and timing.

3. Cost Efficiency: Futures contracts offer a cost-efficient way for financial institutions to gain exposure to various asset classes. Compared to buying physical assets or other investment instruments, futures contracts require a lower upfront investment. This allows institutions to allocate their capital more efficiently and diversify their portfolios at a lower cost.

4. Leveraged Positioning: Futures contracts are highly leveraged instruments, meaning that traders can control a larger position with a relatively small amount of initial margin. This leverage amplifies potential returns, allowing financial institutions to potentially achieve higher profits compared to the initial investment. However, it’s important to note that leverage also magnifies potential losses, and prudent risk management is crucial.

5. Enhanced Market Access: Buying futures contracts provides financial institutions with access to a wide range of markets and asset classes. Rather than physically owning the underlying assets, institutions can gain exposure to commodities, currencies, interest rates, or stock market indices through futures contracts. This increased market access allows for greater diversification and the ability to capitalize on opportunities in different sectors.

6. Margin Efficiency: Futures contracts operate on a margin system, meaning that traders only need to deposit a fraction of the contract’s total value as initial margin. This margin efficiency provides financial institutions the opportunity to allocate their capital more efficiently and potentially increase their exposure to a broader range of assets.

7. Liquidity: Futures markets are highly liquid, with active trading volume throughout the trading day. Financial institutions benefit from this liquidity, as it allows for easy entry and exit of positions and facilitates swift execution of trades. This liquidity reduces the risk of slippage and ensures that financial institutions can efficiently manage their positions.

While buying futures contracts provides potential benefits, it’s important to note that these benefits come with associated risks. The overall success of financial institutions in buying futures contracts depends on their ability to effectively manage risk, conduct thorough market analysis, and execute prudent trading strategies.

By carefully considering the potential benefits and risks, financial institutions can strategically incorporate futures contracts into their investment portfolios, thereby enhancing risk-adjusted returns and expanding their market opportunities.

Risks Involved in Buying Futures Contracts

While buying futures contracts offers potential benefits, it’s crucial for financial institutions to be aware of the inherent risks associated with these derivative instruments. Understanding and effectively managing these risks is crucial to mitigate potential losses. Let’s explore the main risks involved in buying futures contracts:

1. Price Volatility: Futures markets are known for their volatility, with prices fluctuating rapidly and unpredictably. Financial institutions buying futures contracts are exposed to the risk of adverse price movements. If the market moves against their positions, institutions may experience significant losses. It’s essential to conduct thorough market analysis and risk assessment before entering into futures contracts.

2. Leverage and Margin Calls: Futures contracts are highly leveraged instruments, allowing traders to control larger positions with a fraction of the total contract value. While leverage can amplify profits, it also magnifies losses. If market movements result in significant losses, financial institutions may receive margin calls, requiring them to provide additional funds to cover the potential losses. Failure to meet margin requirements may lead to forced liquidation of positions.

3. Counterparty Risk: When financial institutions buy futures contracts, they enter into a contractual agreement with a counterparty. There is always a risk that the counterparty may default on their obligation, potentially resulting in financial losses for the institution. To mitigate this risk, futures contracts are typically traded on regulated exchanges, with a clearinghouse acting as an intermediary to guarantee the performance of the contract.

4. Market Liquidity: While futures markets are generally highly liquid, there can be instances of reduced liquidity or illiquidity, especially in times of extreme market stress or during periods of low trading activity. If financial institutions need to exit their positions quickly, they may encounter difficulties in finding counterparties or executing trades at desired prices, potentially leading to losses or increased transaction costs.

5. Operational and Systemic Risks: Buying futures contracts involves various operational and systemic risks. These risks include errors in trade execution, technological failures, disruptions in the exchange’s infrastructure, or trading platform glitches. Financial institutions need to implement robust risk management systems and controls to mitigate operational risks and ensure smooth trading operations.

6. Regulatory and Legal Risks: Financial institutions operating in futures markets must comply with relevant regulations and legal frameworks. Failure to adhere to these regulations, such as reporting requirements or position limits, can result in regulatory penalties or legal consequences. It is crucial for institutions to have a comprehensive understanding of the regulatory environment and stay updated on any changes in rules or requirements.

Financial institutions must conduct comprehensive risk assessments, implement robust risk management strategies, and continuously monitor market conditions to effectively navigate the risks associated with buying futures contracts. Adequate capital allocation, prudent position sizing, risk diversification, and regular monitoring of market developments are essential aspects of risk management in futures trading.

By understanding and addressing the risks involved, financial institutions can make informed decisions, implement effective risk mitigation strategies, and enhance the overall management of their investment portfolios.

Factors Considered by Financial Institutions When Buying Futures Contracts

When financial institutions make the decision to buy futures contracts, they carefully evaluate various factors to ensure they align with their investment strategies, risk appetite, and client objectives. These factors play a crucial role in determining the suitability and potential success of the futures contracts being considered. Let’s explore the key factors considered by financial institutions:

1. Market Analysis and Research: Financial institutions extensively analyze the underlying market associated with the futures contract. They assess factors such as supply and demand dynamics, macroeconomic indicators, geopolitical news, and technical analysis. Robust market research helps financial institutions develop informed opinions about future price movements and understand the risk-reward characteristics of the contracts they are considering.

2. Risk Management Strategy: Financial institutions have specific risk management frameworks in place to determine the level of risk they are willing to take. Factors such as the institution’s risk tolerance, risk appetite, and the impact of potential losses on their overall portfolio are considered when buying futures contracts. Institutions develop risk management strategies that align with their investment objectives, ensuring that the potential risks associated with the futures contracts are effectively mitigated.

3. Liquidity: Financial institutions assess the liquidity of the particular futures contracts they are considering. Liquidity refers to the ease with which an asset can be bought or sold without causing significant impact on its price. Institutions prefer contracts with high liquidity to ensure there are sufficient trading opportunities and minimal price slippage when entering or exiting positions. Contracts with low liquidity may have wider bid-ask spreads and limited trading volume, making it more challenging to execute trades efficiently.

4. Contract Specifications: Financial institutions carefully review the contract specifications, including the contract size, delivery months, trading hours, and settlement terms. They ensure that the specifications of the futures contracts align with their trading requirements and investment strategies. Institutions also consider any special conditions or unique features associated with the contracts, such as the option for physical delivery or the inclusion of specific delivery locations.

5. Regulatory Environment: Financial institutions consider the regulatory framework governing the futures contracts they are buying. They ensure compliance with regulatory requirements, such as position limits, reporting obligations, and margin requirements. Institutions assess the regulatory landscape to understand any potential changes or developments that may impact their trading activities or affect the viability of the futures contracts they wish to purchase.

6. Client Objectives: Financial institutions often consider the investment objectives and preferences of their clients when buying futures contracts. They evaluate whether the contracts align with their clients’ risk profiles, desired asset allocation, and specific investment goals. Institutions strive to select contracts that meet the unique requirements of their clients, ensuring that the purchased futures contracts contribute to the overall diversification and performance of client portfolios.

7. Historical Performance and Volatility: Financial institutions review historical price patterns, volatility, and correlations to assess the potential risk and return characteristics of the futures contracts. They analyze historical data to gain insights into the asset’s price behavior, identify market trends, and make more informed decisions. Institutions consider factors such as average daily price ranges, historical price movements, and previous market reactions to external events.

By carefully considering these factors, financial institutions can make informed decisions when buying futures contracts. Thorough analysis and evaluation of market conditions, risk appetite, liquidity, client requirements, and regulatory considerations are paramount to successful futures trading strategies.

Examples of Financial Institutions Buying Futures Contracts

Financial institutions, spanning from large banks to hedge funds, actively participate in buying futures contracts to strategically manage their investments and generate profits. Here are a few real-world examples of how financial institutions utilize futures contracts:

1. Investment Banks: Investment banks often engage in proprietary trading using futures contracts. For instance, a bank might buy crude oil futures contracts as they anticipate an increase in oil prices due to global demand trends. If their analysis proves correct, the bank can profit from the price appreciation. Investment banks also purchase futures contracts on behalf of clients, providing exposure to various asset classes, such as equity index futures or foreign currency futures.

2. Hedge Funds: Hedge funds actively trade futures contracts to execute their investment strategies. For example, a macro-focused hedge fund may buy and sell bond futures contracts based on their interest rate outlook. By taking positions in futures contracts tied to interest rates, the hedge fund can profit from anticipated rate movements. Hedge funds also utilize futures to hedge their portfolios, mitigating risks and protecting against adverse market conditions.

3. Pension Funds and Endowments: Pension funds and endowments may use futures contracts to manage their portfolios by hedging against specific risks or gaining exposure to desired asset classes. For instance, pension funds may purchase equity index futures contracts to mimic the performance of a particular stock index and achieve diversification. By investing in futures contracts, pension funds can efficiently allocate their capital and achieve their long-term investment objectives.

4. Commodity Trading Firms: Commodity trading firms, such as those involved in energy, agriculture, or metals, actively participate in buying futures contracts. These firms utilize futures contracts to hedge against commodity price risk. For example, an energy trading company may buy natural gas futures contracts to lock in prices for future delivery, ensuring a consistent cost for their energy production or trading operations.

5. Asset Management Companies: Asset management companies can utilize futures contracts to implement investment strategies across different asset classes. They may buy futures contracts to gain exposure to commodities, currencies, interest rates, or even alternative assets like volatility indices. By incorporating futures contracts into their portfolios, asset management companies can efficiently manage risk, diversify their holdings, and potentially enhance returns for their clients.

6. Commercial Banks: Commercial banks engage in buying futures contracts to manage risk associated with their core business operations. For example, banks may utilize interest rate futures contracts to hedge against changes in interest rates that can impact their loan portfolios. By taking positions in these futures contracts, banks can neutralize the potential adverse impacts of interest rate fluctuations and maintain stability in their lending operations.

7. Proprietary Trading Firms: Proprietary trading firms specialize in executing trades using their own capital to profit from short-term market fluctuations. These firms buy and sell futures contracts across various asset classes including equities, currencies, and commodities. Their trading strategies, such as trend-following or statistical arbitrage, rely on analyses of price patterns and market dynamics to identify profitable opportunities.

These examples highlight the diverse range of financial institutions that actively engage in buying futures contracts. Each institution utilizes futures for different purposes, including risk management, speculation, portfolio diversification, and profit generation. The application of futures contracts varies based on the unique strategies and investment objectives of the respective institutions.

Conclusion

Financial institutions play a crucial role in the buying of futures contracts to manage risk, pursue investment opportunities, diversify portfolios, and meet client requirements. These institutions navigate the dynamic and volatile landscape of futures markets by carefully analyzing market conditions, assessing risk, and implementing effective strategies.

Futures contracts provide financial institutions with a range of benefits, including risk management, speculative opportunities, cost efficiency, enhanced market access, leveraged positioning, and liquidity. By buying futures contracts, institutions can hedge against unfavorable price movements, capitalize on market predictions, gain exposure to various asset classes, and efficiently manage their capital.

However, financial institutions must carefully consider and manage the risks associated with buying futures contracts. Price volatility, leverage, margin calls, counterparty risk, market liquidity, operational risks, and regulatory compliance are important factors that institutions must monitor and mitigate to protect their investments and maintain stability.

When making decisions to buy futures contracts, financial institutions evaluate factors such as market analysis, risk management strategies, liquidity, contract specifications, regulatory environment, and client objectives. Through thorough analysis and consideration of these factors, institutions can ensure that the futures contracts align with their investment goals and risk tolerance.

Real-world examples demonstrate how financial institutions across various sectors and investment strategies actively participate in buying futures contracts. Investment banks, hedge funds, pension funds, commodity trading firms, asset management companies, commercial banks, and proprietary trading firms all utilize futures contracts to achieve different objectives in their investment activities.

In conclusion, buying futures contracts provides financial institutions with valuable tools to effectively manage risk, speculate on price movements, diversify portfolios, and meet client needs. By understanding the potential benefits and risks associated with futures contracts, financial institutions can make informed decisions and implement strategies that drive optimal outcomes.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance