Home>Finance>Why Can’t You Hold Onto Credit Default Swaps Forever

Finance

Why Can’t You Hold Onto Credit Default Swaps Forever

Published: March 4, 2024

Learn why holding onto credit default swaps forever may not be a wise financial decision. Explore the risks and implications in the finance industry.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding the Risks of Holding Credit Default Swaps

Credit default swaps (CDS) have been a prominent feature of the financial landscape since their inception in the 1990s. These derivative instruments, initially designed to provide investors with a means of hedging against the risk of default on bonds and loans, have evolved to become a double-edged sword in the realm of finance. While they offer the potential for substantial profits, the risks associated with holding credit default swaps can be significant and are often underestimated.

As an investor, it's crucial to comprehend the intricacies of credit default swaps and the potential ramifications of holding onto them. This article delves into the nature of credit default swaps, the inherent risks they pose, the costs associated with holding them, and alternative strategies for managing risk in a more prudent manner.

By gaining a deeper understanding of these financial instruments, investors can make informed decisions and mitigate the potential downsides of holding credit default swaps. Let's navigate through the complexities of credit default swaps and explore the reasons why holding onto them indefinitely may not be a prudent course of action.

What are Credit Default Swaps?

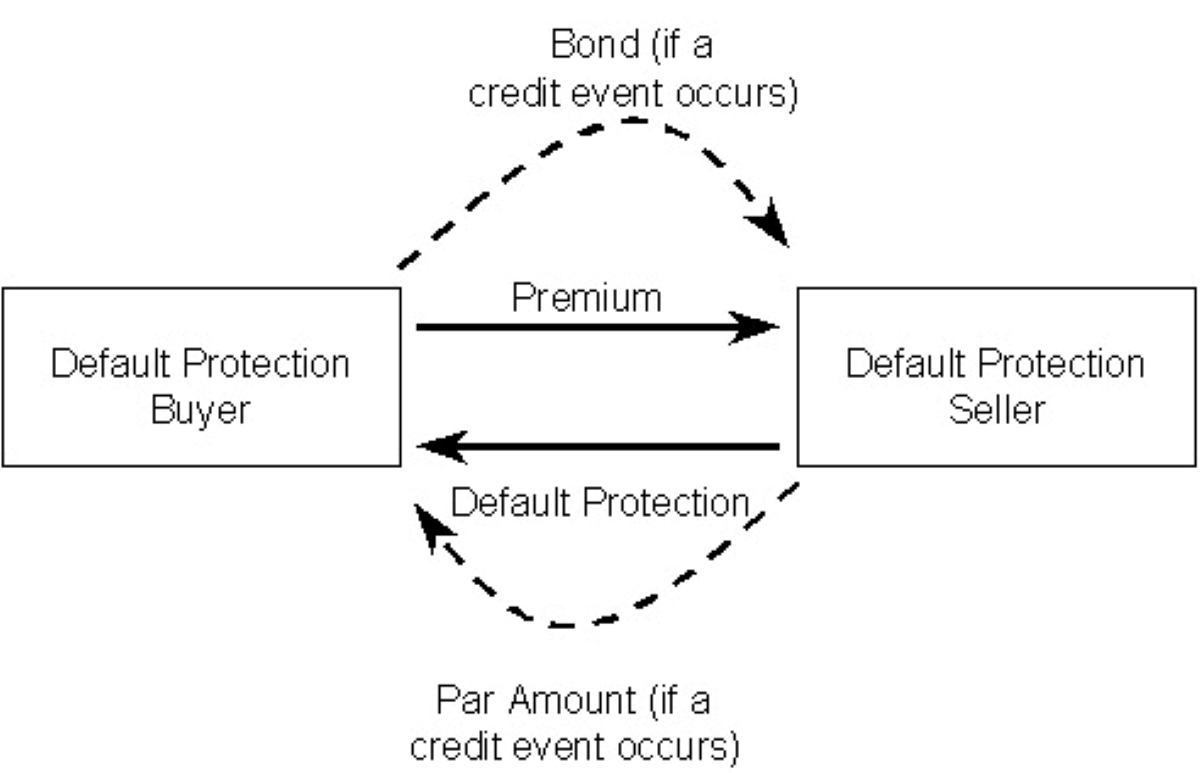

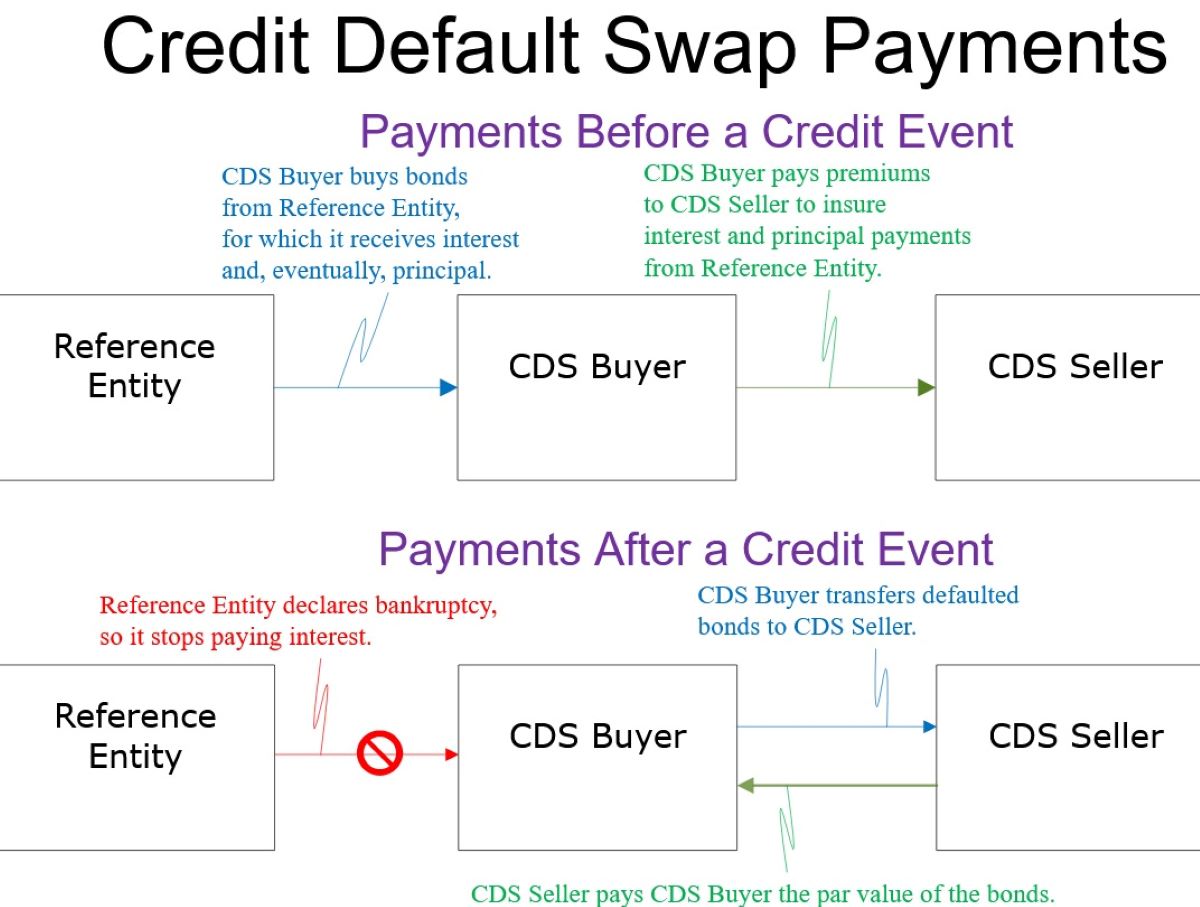

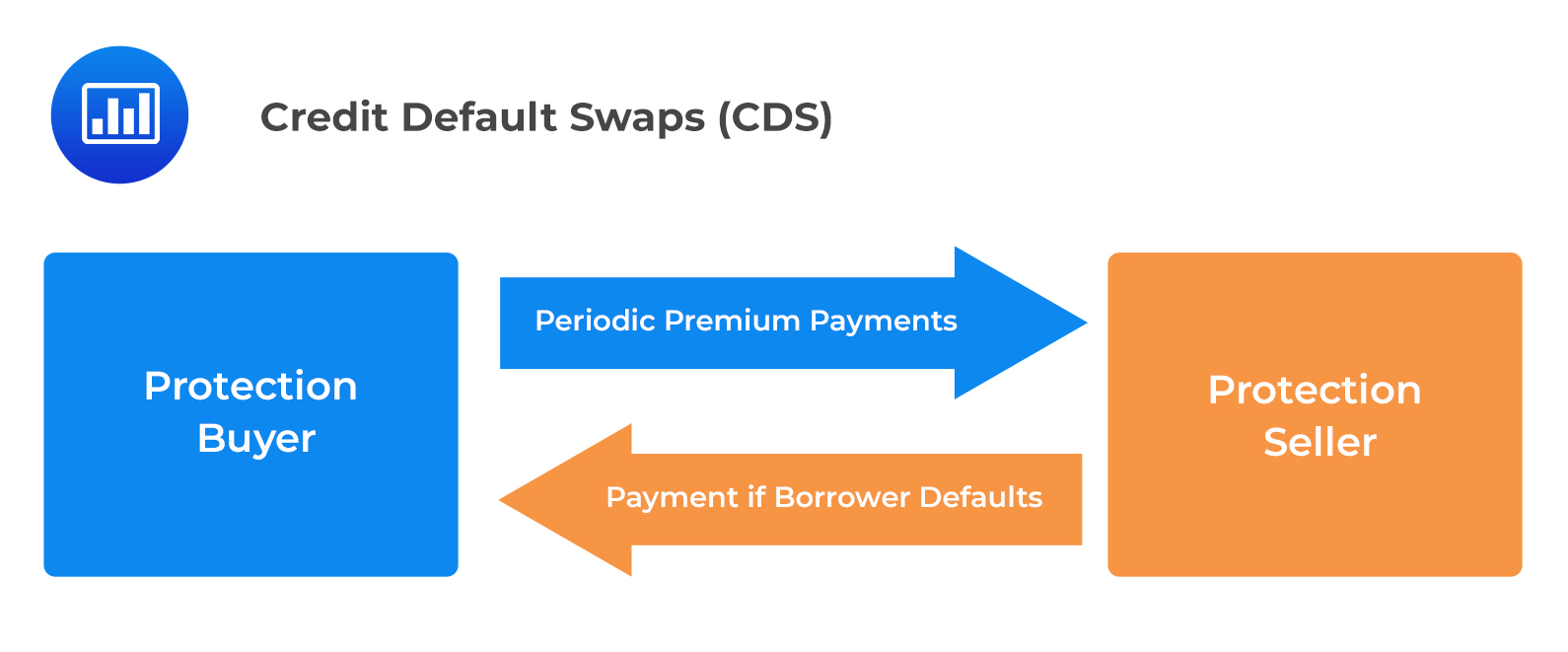

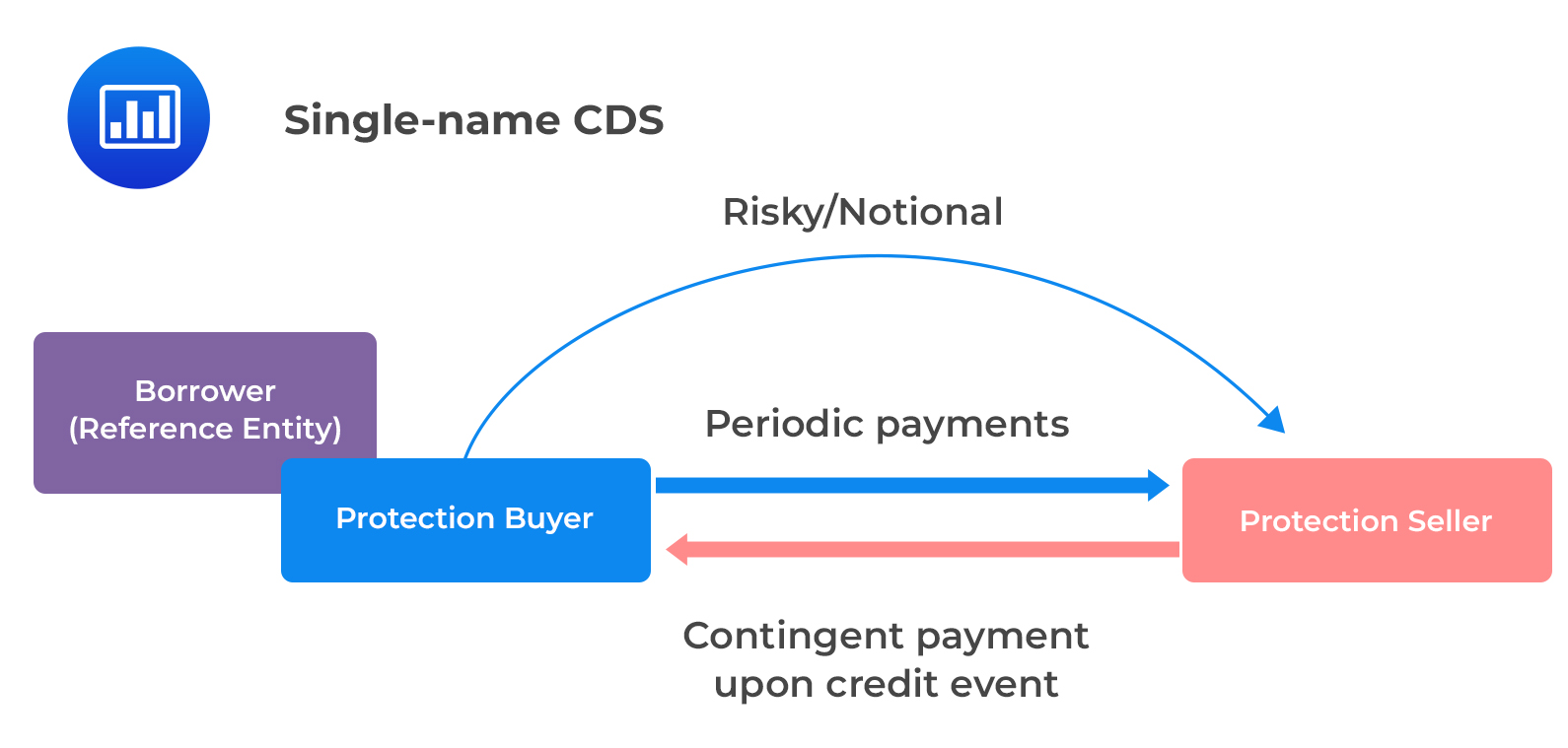

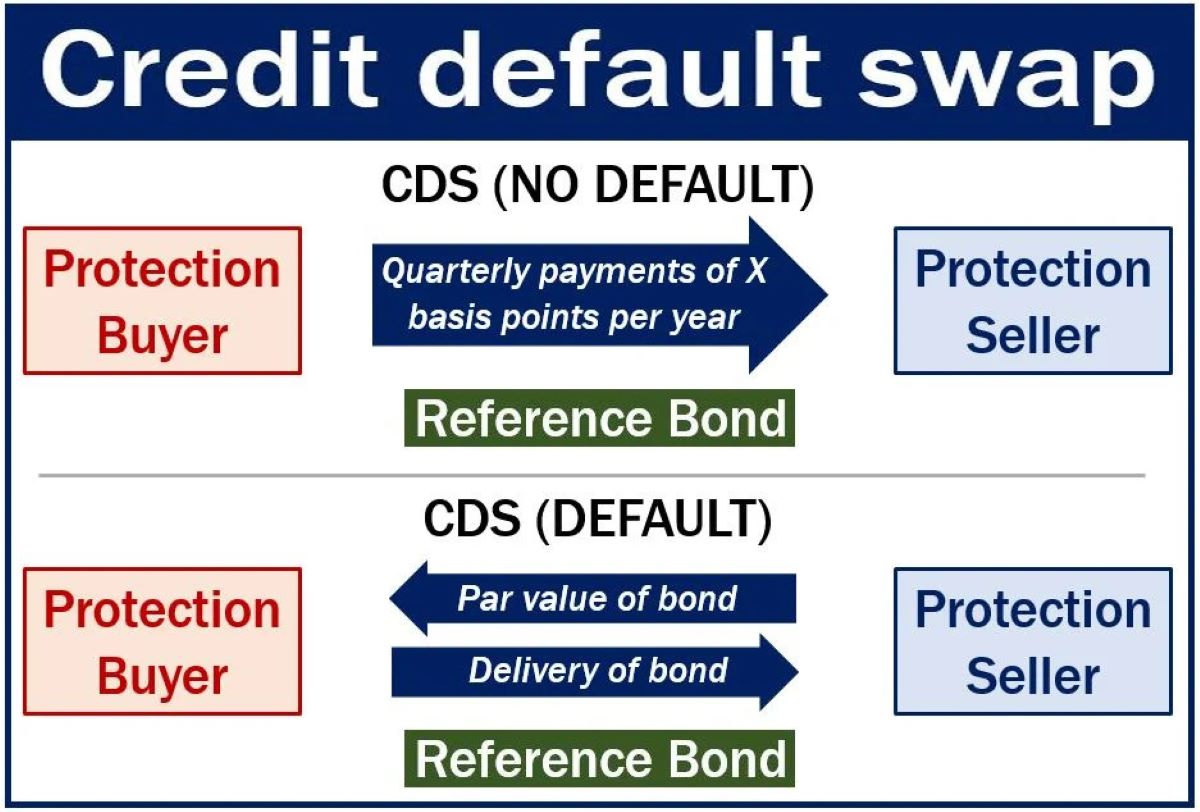

Credit default swaps (CDS) are financial derivatives that enable investors to hedge against the risk of default on bonds and loans or to speculate on the creditworthiness of a particular entity. In essence, a credit default swap functions as a form of insurance against the non-payment of debt. The buyer of a CDS makes periodic payments to the seller in exchange for protection in the event of a credit event, such as a bond issuer defaulting on its obligations.

One of the defining characteristics of credit default swaps is their flexibility. Unlike traditional insurance contracts, CDS can be bought and sold multiple times, allowing investors to adjust their exposure to credit risk dynamically. This feature has contributed to the widespread use of credit default swaps in managing and trading credit risk across various sectors of the financial markets.

Moreover, credit default swaps are not limited to individual bonds or loans. They can be based on a portfolio of assets, known as a synthetic CDO (collateralized debt obligation), which further amplifies their complexity and potential impact on the financial system.

While credit default swaps offer a mechanism for transferring and managing credit risk, they also introduce a layer of complexity and interconnectedness into the financial markets. The intricate nature of these derivatives has been a subject of scrutiny, particularly in the aftermath of the 2008 financial crisis, where the excessive use of CDS contributed to systemic risk and amplified the impact of credit market disruptions.

Understanding the mechanics and implications of credit default swaps is essential for investors and market participants to navigate the complexities of modern finance effectively. By comprehending the role of CDS in the broader financial ecosystem, individuals can make informed decisions regarding their use and assess the associated risks more prudently.

The Risks of Holding Credit Default Swaps

While credit default swaps offer a means of managing credit risk, they also entail inherent risks that warrant careful consideration. One of the primary risks associated with holding credit default swaps is counterparty risk. Since CDS contracts are bilateral agreements between the buyer and the seller, the creditworthiness of the seller becomes a critical factor. In the event of a credit event triggering the CDS, the buyer relies on the seller to fulfill the contractual obligations. If the seller is unable to meet its obligations, the buyer faces the risk of not receiving the protection they paid for, thereby exposing themselves to significant losses.

Another notable risk is the potential for market illiquidity. Credit default swaps are traded over-the-counter (OTC), which means that they are not as standardized or easily tradable as exchange-traded instruments. In times of market stress or heightened uncertainty, liquidity in the CDS market can diminish, making it challenging for investors to unwind their positions or execute new trades. This illiquidity can exacerbate the impact of adverse credit events and hinder investors from effectively managing their exposure to credit risk.

Furthermore, the leverage inherent in credit default swaps can magnify both potential gains and losses. The upfront payment required to initiate a CDS position is substantially lower than the face value of the underlying debt, allowing investors to gain significant exposure with a relatively small capital outlay. While this leverage can amplify profits if the credit risk materializes as anticipated, it also heightens the downside risk if the market moves unfavorably.

Additionally, the interconnectedness of credit default swaps with other financial instruments and institutions can contribute to systemic risk. The widespread use of CDS in the financial system means that adverse developments in the CDS market can reverberate across various sectors, potentially amplifying the impact of credit events and creating contagion effects.

Understanding and effectively managing these risks is imperative for investors who hold or are considering entering into credit default swap positions. By acknowledging the inherent complexities and vulnerabilities associated with CDS, market participants can adopt more robust risk management strategies and make well-informed decisions regarding their credit risk exposure.

The Cost of Holding Credit Default Swaps

While credit default swaps offer a mechanism for managing credit risk, they come with associated costs that can impact investors’ overall portfolio performance. One of the primary costs of holding credit default swaps is the ongoing payment, known as the premium, made by the buyer to the seller. This premium compensates the seller for assuming the risk of default and providing protection to the buyer. The cost of the premium is influenced by various factors, including the creditworthiness of the reference entity, prevailing market conditions, and the duration of the CDS contract.

Furthermore, the premium payments for credit default swaps are recurring expenses that can erode the potential gains from the investment. For investors holding CDS positions over an extended period, the cumulative premium payments can diminish the overall profitability of the investment, particularly if the anticipated credit events do not materialize, leading to a loss on the premium outlay.

Another cost consideration is the impact of margin requirements. In some cases, holding credit default swaps may necessitate the posting of collateral or margin to mitigate the risk of default by the buyer or seller. This requirement ties up additional capital, potentially limiting the investor’s capacity to deploy funds in other investment opportunities or increasing the overall funding costs of maintaining the CDS positions.

Moreover, the potential for basis risk introduces another dimension of cost associated with credit default swaps. Basis risk arises when the hedging provided by the CDS does not perfectly align with the underlying credit exposure, leading to potential inefficiencies and suboptimal risk management. Addressing basis risk may require additional hedging strategies or adjustments, incurring further costs for the investor.

It is essential for investors to carefully assess the total cost of holding credit default swaps and evaluate whether the benefits of credit risk mitigation outweigh the associated expenses. By conducting a comprehensive cost-benefit analysis, investors can make informed decisions regarding the use of credit default swaps in their investment and risk management strategies, ensuring that the overall impact on their portfolio aligns with their financial objectives.

Alternatives to Holding Credit Default Swaps

While credit default swaps offer a means of managing credit risk, investors have alternative strategies at their disposal to achieve similar objectives without the complexities and risks associated with holding CDS positions. One alternative approach is to utilize traditional risk management tools, such as diversification and asset allocation, to mitigate credit risk within an investment portfolio. By spreading investments across different asset classes, industries, and geographic regions, investors can reduce their exposure to individual credit events and enhance the overall resilience of their portfolios.

Another alternative is the use of credit derivatives, such as credit spread options or total return swaps, to hedge against credit risk. These instruments provide flexibility in tailoring risk management strategies to specific credit exposures while potentially offering more transparent and standardized terms compared to credit default swaps. By exploring a diverse range of credit derivatives, investors can identify instruments that align more closely with their risk preferences and investment objectives.

Furthermore, engaging in fundamental credit analysis and due diligence can serve as a proactive alternative to relying solely on credit default swaps for managing credit risk. By thoroughly assessing the creditworthiness of bond issuers and counterparties, investors can make informed decisions regarding their credit exposures, potentially reducing the reliance on derivative instruments for risk mitigation.

Employing dynamic risk management strategies, such as active monitoring and adjustment of credit exposures based on evolving market conditions, can also serve as an alternative to static credit default swap positions. By maintaining agility in responding to changing credit dynamics, investors can adapt their risk management approaches in a more nimble and responsive manner, potentially mitigating the need for prolonged CDS holdings.

Exploring these alternatives empowers investors to diversify their risk management toolkit, potentially reducing their dependency on credit default swaps while achieving effective credit risk mitigation. By incorporating a combination of traditional risk management practices, alternative derivatives, rigorous credit analysis, and dynamic risk management techniques, investors can tailor their approach to credit risk in a manner that aligns with their risk tolerance and investment objectives.

Conclusion

Credit default swaps, while offering a mechanism for managing credit risk, present investors with a complex array of risks and costs that necessitate careful consideration. The inherent risks of holding credit default swaps, including counterparty risk, market illiquidity, leverage, and interconnectedness, underscore the importance of a thorough understanding of these derivatives and their potential impact on investment portfolios.

Furthermore, the costs associated with holding credit default swaps, such as premium payments, margin requirements, and basis risk, contribute to the overall expense and complexity of maintaining CDS positions. Investors must weigh these costs against the benefits of credit risk mitigation to determine the suitability of credit default swaps within their investment strategies.

Exploring alternative approaches to managing credit risk, including traditional risk management tools, credit derivatives, fundamental credit analysis, and dynamic risk management strategies, provides investors with a diverse toolkit for achieving effective risk mitigation without solely relying on credit default swaps.

By comprehensively evaluating the risks, costs, and alternatives associated with credit default swaps, investors can make informed decisions that align with their risk tolerance and investment objectives. Whether through diversification, alternative derivatives, rigorous credit analysis, or dynamic risk management, the ability to tailor risk management strategies to specific credit exposures empowers investors to navigate the complexities of credit risk in a manner that suits their individual preferences.

In conclusion, while credit default swaps remain a viable tool for managing credit risk, investors must approach their usage judiciously, considering the full spectrum of risks, costs, and available alternatives. By integrating a diverse range of risk management techniques and maintaining a nuanced understanding of the dynamics of credit markets, investors can optimize their approach to credit risk management and enhance the resilience of their investment portfolios.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance