Finance

FICO Definition

Published: November 23, 2023

Discover the meaning of FICO in finance and how it impacts your credit score. Gain insight into the importance of FICO in managing your financial health.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Welcome to the Finance Category: Unraveling the FICO Definition

Welcome to the Finance category on our blog, where we explore various aspects of money, credit, and everything in between! Today, we are diving deep into the world of FICO and its definition. If you’ve ever wondered what FICO stands for and what it means for your financial well-being, then you’ve come to the right place. Let’s unravel the FICO definition and discover why it is crucial for your financial success.

Key Takeaways:

- FICO stands for Fair Isaac Corporation and is a standardized credit scoring system used by lenders to assess an individual’s creditworthiness.

- Your FICO score is calculated based on various factors, including payment history, credit utilization, length of credit history, credit mix, and recent credit inquiries.

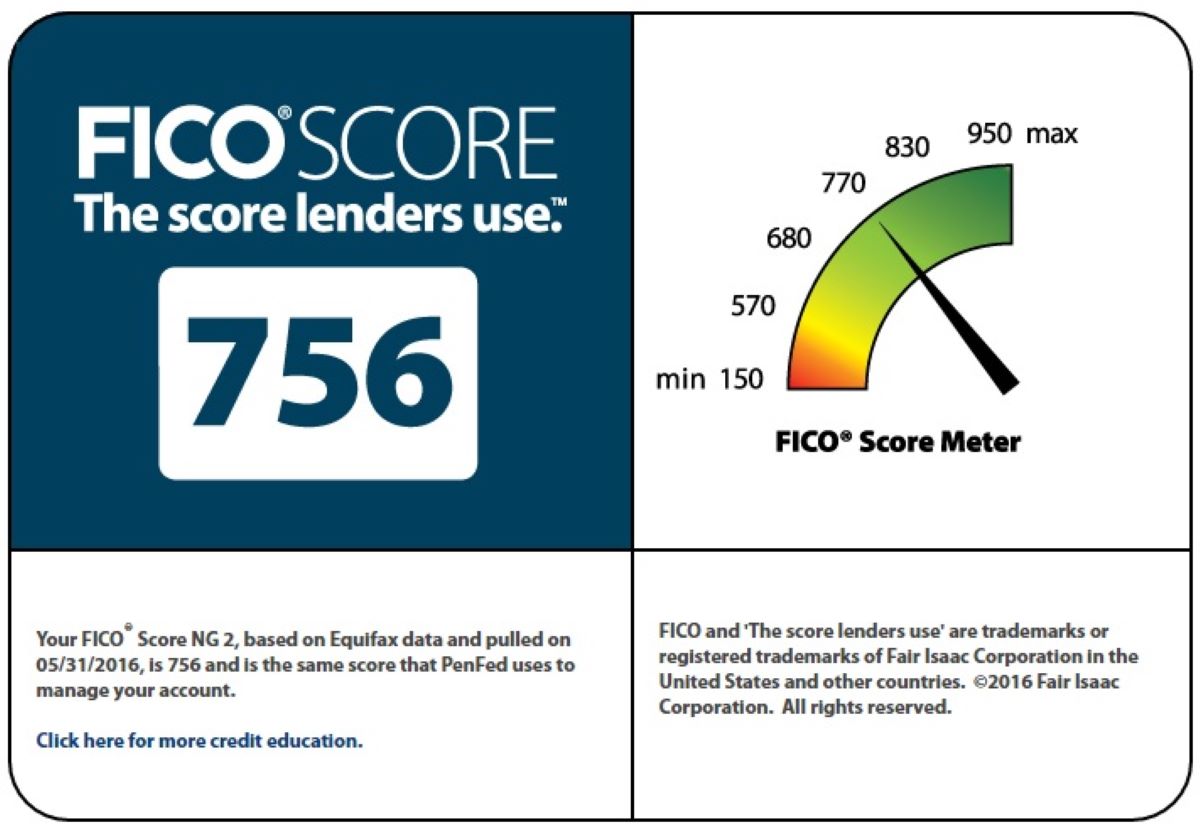

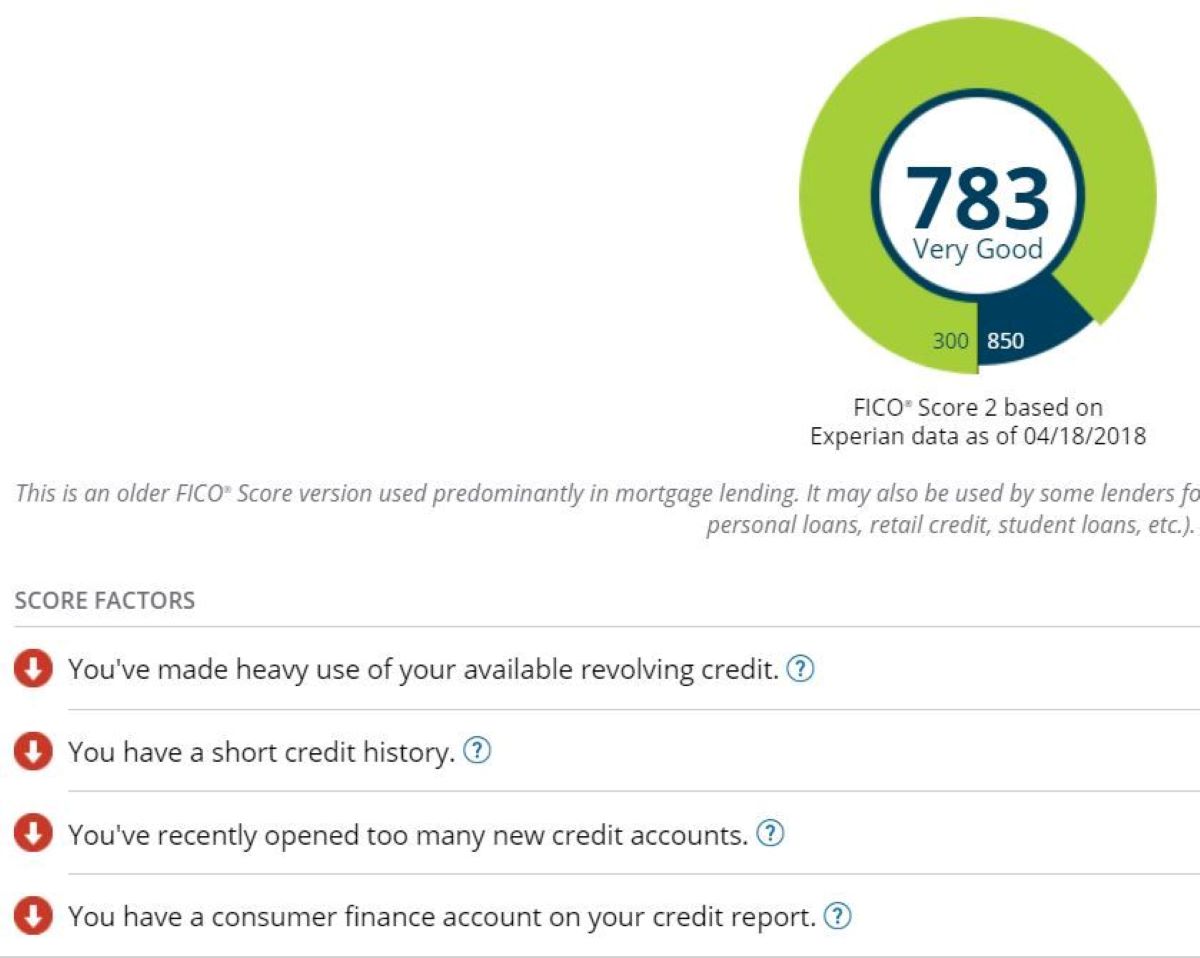

First things first, what does FICO actually stand for? FICO is an acronym for Fair Isaac Corporation, the company that developed the FICO scoring model. This scoring model is widely used by lenders to evaluate an applicant’s creditworthiness or their ability to repay a loan. Think of it as a snapshot of your financial health that lenders take into consideration before approving credit applications.

Now, you may be wondering how your FICO score is determined. Well, it takes into account several key components:

- Payment History: This is the most significant factor in determining your FICO score. It tracks whether you have paid your bills on time and if you have any negative records such as late payments or collections.

- Credit Utilization: This factor considers how much of your available credit you are using. If you consistently use a high percentage of your credit limit, it may negatively impact your score.

- Length of Credit History: The longer your credit history is, the better it reflects your financial behavior. Lenders want to see a track record of responsible credit management.

- Credit Mix: Having a diverse mix of credit accounts, such as credit cards, loans, and mortgages, can positively impact your score. It shows that you can handle different types of credit responsibly.

- Recent Credit Inquiries: When you apply for new credit, it triggers a credit inquiry. Multiple inquiries within a short period may suggest financial instability and can slightly lower your score.

So, why does your FICO score matter? Your FICO score is essential because it can significantly influence your financial life. Here are two key takeaways:

- Access to Credit: Lenders often refer to your FICO score to determine your creditworthiness. A high FICO score can make it easier for you to obtain loans, credit cards with favorable interest rates, and other forms of credit.

- Cost of Credit: Your FICO score can impact the interest rates you are offered. A lower score may result in higher interest rates, which can cost you more over time.

To summarize, understanding the FICO definition and how your score is calculated is crucial for your financial well-being. In future blog posts, we will explore strategies to improve your FICO score and maintain good credit health. Stay tuned and remember, awareness is the first step towards financial success!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance