Finance

What Is A Credit Card Balance

Modified: March 3, 2024

Learn about credit card balances and how they impact your personal finances. Find out how to manage your credit card balance effectively to avoid debt and financial stress.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Credit cards have become an integral part of our modern financial landscape. They offer convenience, flexibility, and the ability to make purchases or access funds without carrying cash. However, it is essential to understand how credit card balances work to avoid falling into debt and managing your finances responsibly.

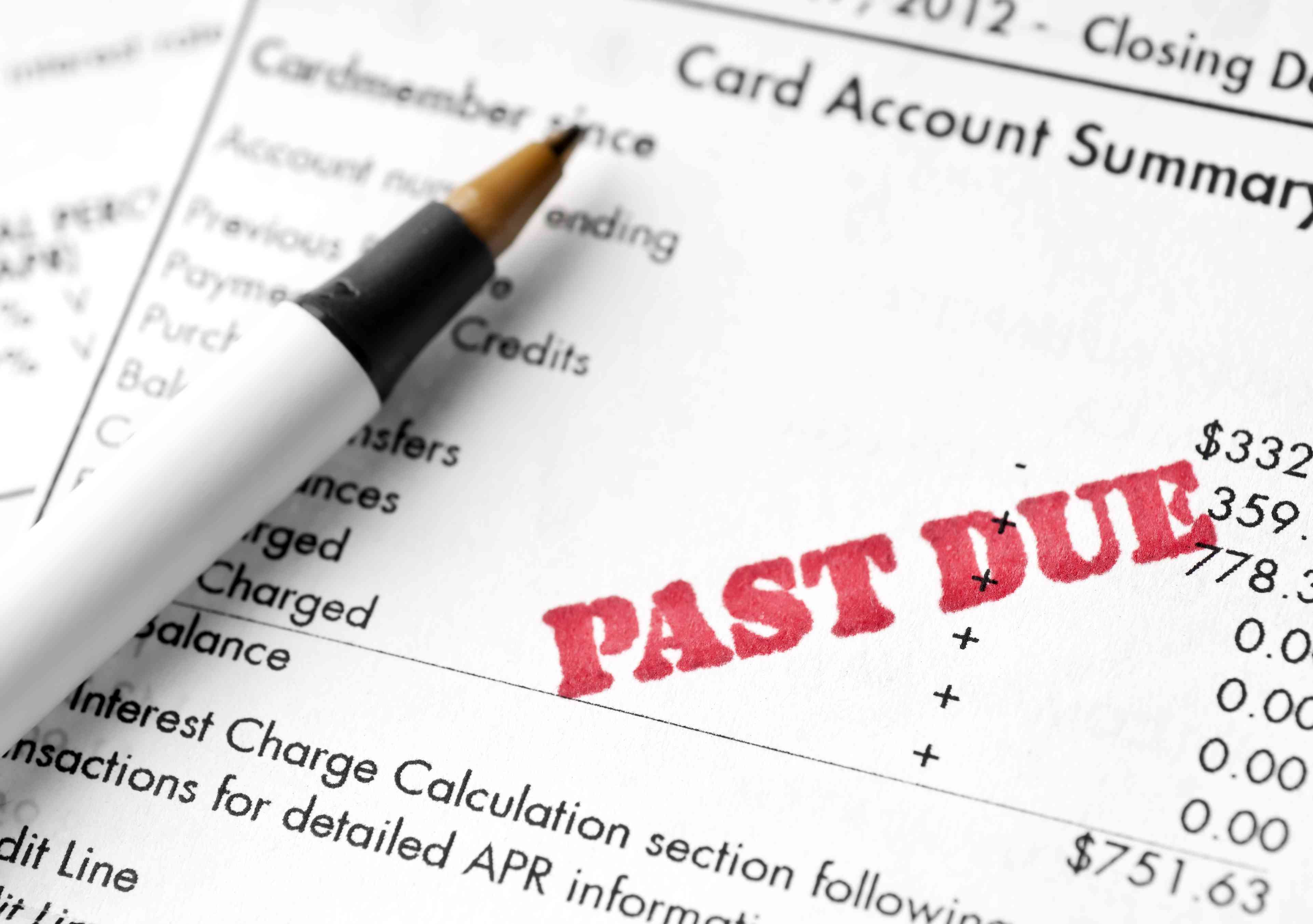

A credit card balance refers to the amount of money owed to the credit card company for purchases, cash advances, or balance transfers that have not been paid off. It is essentially the accumulated debt on your credit card account. Understanding how credit card balances are calculated and the implications of carrying a high balance is vital for maintaining good financial health.

In this article, we will explore the definition of a credit card balance, how balances are calculated, and the factors that influence them. We will also provide tips for managing and paying off credit card balances effectively.

Whether you are new to credit cards or seeking to improve your financial habits, this article will provide insights and strategies to help you make informed decisions regarding your credit card balances.

Definition of Credit Card Balance

A credit card balance refers to the outstanding amount of money that you owe to the credit card issuer. It represents the total unpaid charges on your credit card account, including purchases, cash advances, balance transfers, and any associated fees or interest charges.

When you make a purchase using your credit card, the amount is added to your balance. This balance accumulates as you continue to make purchases and incur charges. If you pay off your entire balance by the due date, you will not be charged interest. However, if you carry a balance from one month to the next, you will be charged interest on the remaining amount, which increases your debt.

Your credit card statement provides a snapshot of your current balance, as well as details of your transactions, payments, and any applicable fees or interest charges. The statement also outlines the minimum payment required and the due date for that payment. It is crucial to review your statement regularly to stay informed about your credit card balance and to avoid any surprises.

How Credit Card Balances are Calculated

Credit card balances are calculated based on several factors, including purchases, cash advances, balance transfers, fees, and interest charges. Understanding how these elements contribute to your balance can help you make informed decisions and manage your credit card debt effectively.

Purchases: When you use your credit card to make purchases, the amount of the purchase is added to your balance. For example, if you buy groceries for $100 using your credit card, your balance will increase by $100.

Cash Advances: Cash advances allow you to withdraw cash from your credit card. However, they often come with high-interest rates and fees. When you take a cash advance, the amount you withdraw is added to your balance. Keep in mind that cash advances typically have higher interest rates than regular purchases.

Balance Transfers: Balance transfers involve moving your existing credit card debt from one card to another, usually at a lower interest rate. When you make a balance transfer, the transferred amount is added to your new credit card’s balance.

Fees: Credit card companies may charge various fees, such as annual fees, late payment fees, or foreign transaction fees. These fees are added to your balance and increase the amount you owe.

Interest Charges: If you carry a balance from one month to the next, you will accrue interest charges on the remaining amount. The interest rate, also known as the Annual Percentage Rate (APR), varies depending on your credit card terms and the type of transaction. The longer you carry a balance, the more interest you will accumulate, increasing your overall debt.

It’s important to note that some credit cards offer an interest-free grace period for new purchases. If you pay your balance in full by the due date, you won’t incur any interest on those purchases. However, cash advances and balance transfers generally don’t have a grace period and begin accruing interest immediately.

To calculate your credit card balance accurately, you need to consider all these factors and ensure that you stay on top of your payments, fees, and interest charges. It’s advisable to review your monthly statement and keep track of your expenses to have a clear understanding of your current balance and potential debt.

Understanding the Minimum Payment

When you receive your credit card statement, you’ll notice a “minimum payment” amount. This is the minimum amount you are required to pay to keep your account in good standing. While it may be tempting to only pay the minimum, it’s important to understand the implications of doing so.

The minimum payment is typically a small percentage of your total balance. It is designed to ensure that you at least cover the interest charges and fees on your account. However, paying only the minimum amount can prolong the time it takes to pay off your balance and result in substantial interest charges.

Here’s how the minimum payment works:

- The minimum payment is usually around 2-3% of your total balance, but can vary depending on the credit card issuer.

- Paying the minimum amount by the due date helps you avoid late payment fees and keeps your account in good standing.

- If you only pay the minimum, the remaining balance will continue to accrue interest, increasing your overall debt.

- While making the minimum payment is better than missing a payment entirely, it’s not a long-term solution for managing your credit card balance.

To illustrate the potential consequences of paying only the minimum, let’s say you have a credit card balance of $5,000 with an annual interest rate of 18%. If your minimum payment is 3% of your balance (which would be $150 in this case), it would take approximately 10 years to pay off the entire debt, and you would end up paying over $5,000 in interest alone!

By paying more than the minimum and tackling your balance aggressively, you can save significantly on interest charges and reduce the time it takes to become debt-free.

It’s important to carefully evaluate your budget and financial situation to determine how much more than the minimum payment you can afford. Allocating additional funds towards your credit card payments can help you pay off your balance faster and save money in the long run.

Remember, the minimum payment is just a starting point. Aim to pay off your credit card balance in full each month if possible, or, at the very least, pay as much as you can comfortably afford to reduce your debt more quickly.

Factors Affecting Credit Card Balances

Several factors can influence your credit card balance, and understanding them can help you better manage and control your debt. By being aware of these factors, you can make informed decisions when using your credit card and keep your balances at a manageable level.

1. Credit Card Usage: The more you use your credit card for purchases, cash advances, or balance transfers, the higher your balance will be. It’s important to be mindful of your spending habits and use your credit card responsibly to avoid accumulating unnecessary debt.

2. Interest Rates: The interest rate on your credit card plays a significant role in determining how quickly your balance grows. Higher interest rates result in higher interest charges, making it more challenging to pay off your balance. To minimize interest expenses, consider choosing a credit card with a lower interest rate or explore options for transferring your balance to a card with a more favorable rate.

3. Payment Habits: How you manage your credit card payments affects your balance. Paying your balance in full and on time each month helps avoid interest charges and keeps your balance low. On the other hand, making only the minimum payment or missing payments can lead to increased balances due to interest charges and late fees.

4. Fees and Charges: Credit card fees, such as annual fees, late payment fees, and foreign transaction fees, can add to your balance. It’s crucial to review the terms and conditions of your credit card to understand the potential fees associated with it. Being aware of these fees and avoiding unnecessary charges can help keep your balance in check.

5. Promotional Offers: Some credit cards offer promotional interest rates, rewards, or cashback for specific periods or transactions. While these offers can be beneficial, it’s important to be cautious and understand the terms and conditions. For example, a credit card that offers a 0% APR for balance transfers may have a higher regular interest rate once the promotional period ends.

6. Credit Limit: Your credit limit is the maximum amount you can charge to your credit card. It’s important to manage your usage in relation to your credit limit to maintain a healthy credit utilization ratio. Utilizing a high percentage of your available credit can negatively impact your credit score and may make it more challenging to manage your credit card balance.

7. Changes in Interest Rates: Some credit cards may have variable interest rates that can change over time. Fluctuations in interest rates can affect the amount of interest you pay on your credit card balance. Staying informed about any changes in your credit card’s interest rate can help you adjust your repayment strategy accordingly.

By considering these factors and being proactive in managing your credit card balance, you can maintain control over your debt and work towards achieving financial stability.

Tips for Managing and Paying off Credit Card Balances

Managing and paying off credit card balances is crucial for maintaining good financial health and avoiding unnecessary debt. Here are some effective strategies to help you stay on top of your credit card balances:

- Create a Budget: Start by assessing your income and expenses to create a realistic budget. Identify areas where you can cut back on spending and allocate a portion of your income towards paying off your credit card balances.

- Pay More Than the Minimum: Whenever possible, pay more than the minimum payment required. By paying more, you’ll reduce the amount of interest charged and accelerate the process of paying off your balances.

- Consolidate Your Debt: If you have multiple credit cards with balances, consider consolidating your debt into one credit card or a personal loan with a lower interest rate. This can simplify your payments and potentially save you money on interest.

- Avoid Unnecessary Charges: Be mindful of your spending habits and try to avoid unnecessary purchases. Consider whether you really need an item before charging it to your credit card. By curbing impulsive spending, you can prevent your balances from growing excessively.

- Track Your Expenses: Keep a record of your purchases and review your monthly statements to identify any areas where you may be overspending. This can help you make necessary adjustments to your budget and identify areas where you can cut back.

- Negotiate Lower Interest Rates: Contact your credit card issuer to inquire about lowering your interest rate. If you have a good payment history and credit score, they may be willing to reduce your rate, allowing you to save on interest charges.

- Consider Balance Transfers: Explore balance transfer options if you have high-interest credit card debt. Look for credit cards that offer low or 0% introductory APRs on balance transfers. This can provide temporary relief from interest charges, allowing you to focus on paying off your balances more quickly.

- Seek Professional Help if Needed: If you’re struggling to manage your credit card balances and find yourself falling deeper into debt, consider seeking assistance from a credit counseling agency or a financial advisor. They can provide guidance and help you develop a realistic plan to regain control of your finances.

Remember, managing your credit card balances requires discipline and a proactive approach. By implementing these tips and strategies, you can make significant progress in paying off your debt and achieving financial freedom.

The Implications of Carrying a High Credit Card Balance

Carrying a high credit card balance can have significant implications on your financial well-being and overall creditworthiness. Here are some of the potential consequences of carrying a high credit card balance:

- Increased Interest Charges: One of the most immediate effects of carrying a high balance is the accumulation of interest charges. Credit cards typically have high interest rates, which can result in substantial interest expenses if you don’t pay off your balances in full each month. As your balances grow, so do the interest charges, making it harder to pay off your debt and potentially leading to a cycle of revolving credit.

- Financial Stress: High credit card balances can cause significant financial stress. The burden of carrying debt and the pressure to make monthly payments can lead to anxiety and sleepless nights. It can also impact your overall well-being and strain relationships.

- Negative Impact on Credit Score: Your credit card utilization, which is the ratio of your credit card balance to your credit limit, is a crucial factor in determining your credit score. Carrying a high credit card balance increases your credit utilization ratio, which can negatively impact your credit score. A lower credit score can make it harder to obtain loans, secure favorable interest rates, or even get approved for rental applications.

- Reduced Available Credit: Carrying high balances on your credit cards reduces the amount of available credit you have left. This means you’ll have limited funds available for emergencies or other essential purchases. It can also affect your credit score as it indicates a higher level of risk to lenders.

- Impacts Future Financial Goals: Carrying a high credit card balance can hinder your ability to achieve future financial goals. It can make it more challenging to save for a down payment on a house, invest in your retirement, or pursue other important milestones. The longer you carry a high balance, the longer it may take to break free from debt and focus on your financial aspirations.

- Difficulty in Obtaining New Credit: When you have a high credit card balance, it may be more challenging to obtain new credit, such as loans or credit cards. Lenders may view you as a higher risk borrower and be hesitant to extend you credit. This can limit your options and opportunities in accessing additional credit for important purchases or emergencies.

It’s crucial to recognize the implications of carrying a high credit card balance and take steps to address the situation. Implementing a sound strategy to pay down your debt, managing your spending habits, and seeking professional guidance if necessary can help you regain control of your finances and improve your overall financial well-being.

Conclusion

Managing and understanding credit card balances is essential for maintaining good financial health. It’s important to be aware of the factors that contribute to your credit card balance, such as purchases, cash advances, fees, and interest charges. By staying informed and implementing effective strategies, you can avoid unnecessary debt and make progress towards paying off your balances.

Remember to pay more than the minimum payment whenever possible and avoid unnecessary charges. Creating a budget, tracking your expenses, and negotiating lower interest rates can also help you manage your credit card balances effectively. If you find yourself overwhelmed with debt, don’t hesitate to seek professional guidance to develop a customized plan to regain control of your finances.

Carrying a high credit card balance can have far-reaching implications, including increased interest charges, financial stress, negative impacts on your credit score, reduced available credit, and difficulties in obtaining future credit. By taking proactive steps to reduce your balances and pay off your debt, you can work towards a healthier financial future.

Remember that responsible credit card usage involves using your credit card wisely, paying off your balances in full whenever possible, and keeping track of your spending. By practicing smart financial habits and staying informed, you can avoid the pitfalls of high credit card balances and enjoy a more secure financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance