Home>Finance>What Is Meant By “Basis Risk” When Futures Contracts Are Used For Hedging?

Finance

What Is Meant By “Basis Risk” When Futures Contracts Are Used For Hedging?

Modified: February 21, 2024

Learn about basis risk in finance and its connection to hedging with futures contracts. Understand the implications and importance in managing financial risk.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the world of finance, risk management is a crucial aspect of mitigating losses and protecting investments. One commonly used strategy for risk management is hedging, which involves utilizing futures contracts to offset potential fluctuations in the price of an underlying asset. While futures contracts can be an effective tool for hedging, they are not without their own set of risks. One such risk is known as basis risk.

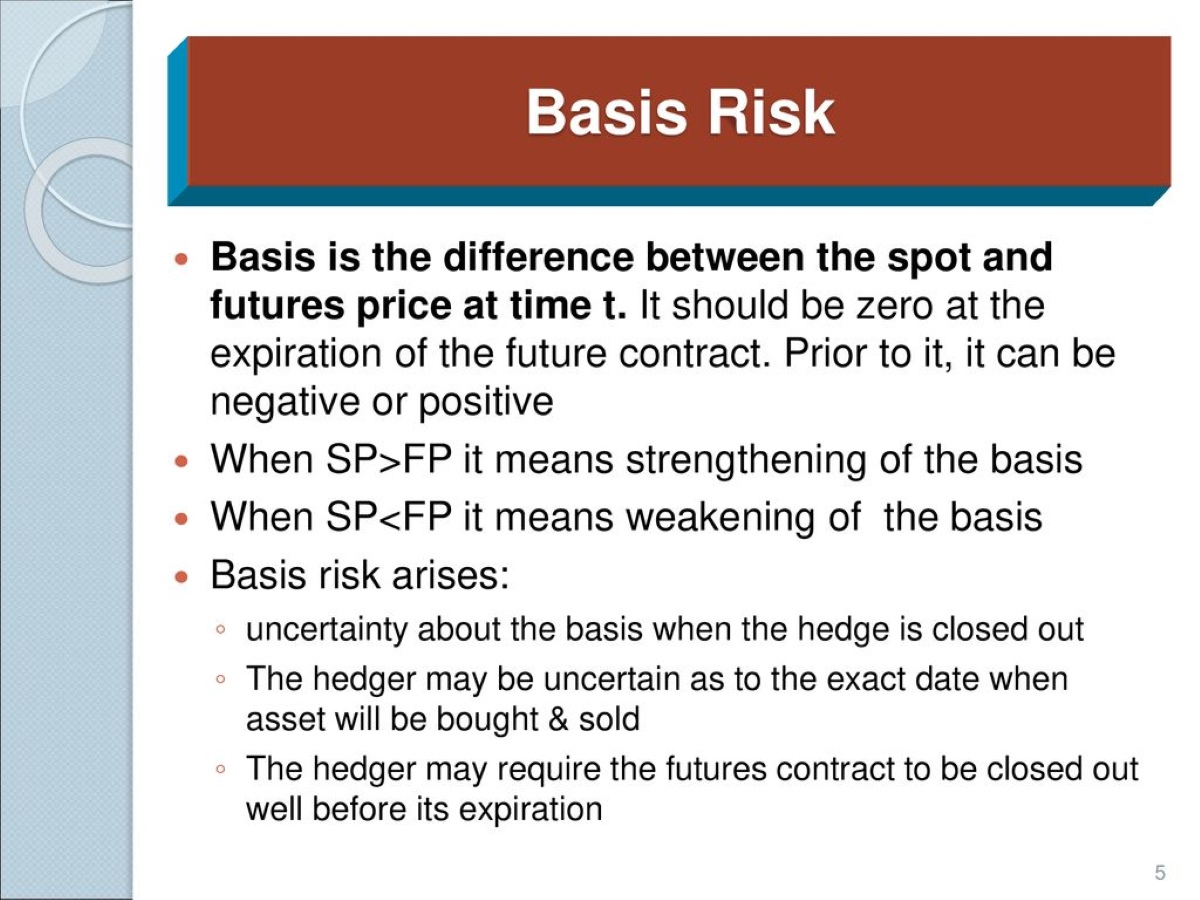

Basis risk is the uncertainty that arises from the imperfect correlation between the price movements of the hedged asset and the futures contract being used for hedging. In other words, it is the risk that the difference between the spot price of the underlying asset and the price of the futures contract widens or narrows over time.

This article aims to provide a comprehensive understanding of basis risk and its implications in the context of using futures contracts for hedging. By delving into the factors contributing to basis risk and exploring real-life examples, we will uncover the challenges that investors and financial institutions face and how they can effectively manage basis risk.

Definition of futures contracts and hedging

To fully comprehend basis risk, it is essential to first establish a clear understanding of futures contracts and hedging.

A futures contract is a standardized agreement between two parties to buy or sell an asset at a predetermined price and date in the future. The underlying asset can be commodities, currencies, stocks, or even interest rates. Futures contracts are traded on organized exchanges, such as the Chicago Mercantile Exchange (CME) or the New York Mercantile Exchange (NYMEX).

Hedging, on the other hand, is a risk management strategy used to protect against potential losses resulting from adverse price movements in the financial markets. It involves taking an offsetting position in a related asset or derivative to mitigate the impact of price fluctuations. The purpose of hedging is to minimize risk rather than seek profits.

By using futures contracts for hedging, investors can lock in a specific price for the underlying asset, thus protecting themselves from future price fluctuations. This is particularly valuable for businesses involved in the production, purchase, or sale of commodities, as it provides them with price certainty and helps stabilize their operations.

Now that we have a fundamental understanding of futures contracts and hedging, let’s explore the concept of basis risk and its implications in hedging strategies.

Understanding basis risk

Basis risk is the potential for a discrepancy between the price of the underlying asset and the price of the futures contract being used for hedging. It arises due to factors such as differences in market conditions, liquidity, and delivery terms between the spot market and the futures market.

It is important to note that while futures contracts are designed to mimic the price movements of the underlying asset, they are not an exact replica. This results in a basis, which represents the difference between the spot price and the futures price at any given point in time.

Basis risk can have both positive and negative impacts on the effectiveness of a hedging strategy. If the basis narrows or converges, meaning the futures price moves closer to the spot price, the hedging position will become more effective in mitigating losses. Conversely, if the basis widens or diverges, the effectiveness of the hedge is reduced, and potential losses may occur.

There are several factors that contribute to basis risk. One of the main factors is the difference in the delivery dates between the futures contract and the underlying asset. For example, if a commodity futures contract expires before the actual delivery date of the commodity, there may be a mismatch in prices and market conditions, leading to basis risk.

Another factor influencing basis risk is the quality or grade of the underlying asset. For commodities such as oil or grains, different grades may have varying supply and demand dynamics, resulting in differences in spot and futures prices. This discrepancy introduces basis risk into the hedging strategy.

Market liquidity is also a key factor in basis risk. If the futures market is illiquid, meaning there is low trading volume and limited buyer or seller participation, it can lead to wider bid-ask spreads and less accurate pricing. This can result in a larger basis and increased basis risk.

Overall, understanding basis risk is crucial for investors and financial institutions engaged in hedging strategies. By recognizing the factors that contribute to basis risk, they can better assess the effectiveness of their hedging positions and make informed decisions to mitigate potential losses.

Factors contributing to basis risk

Basis risk, as mentioned earlier, is the result of various factors that contribute to the discrepancy between the spot price of the underlying asset and the price of the futures contract. Understanding these factors is key to effectively managing basis risk in hedging strategies.

One significant factor contributing to basis risk is timing. The delivery date of the futures contract may not align perfectly with the time when the underlying asset needs to be hedged. This mismatch in timing can lead to differences in market conditions, resulting in a wider basis. For example, if a company hedges its commodity purchases for the next quarter using futures contracts with earlier expiration dates, there may be a disparity in price between the futures contract and the spot market at the time of hedging.

Another factor is the location of the underlying asset. Different geographical locations may have variations in supply and demand dynamics, transportation costs, and storage availability, which can lead to differences in spot and futures prices. This geographic basis risk is particularly relevant for commodities like oil, natural gas, or agricultural products, where regional factors can influence pricing.

Quality or grade differences of the underlying asset can also contribute to basis risk. For commodities with different grades or specifications, such as metals, grains, or oil, the spot price of each grade may not align perfectly with the futures contract, leading to basis risk. This is because market participants may have varying preferences or requirements for specific grades, resulting in price differentials.

Market liquidity is an additional factor influencing basis risk. If the futures market for a particular asset is illiquid, it can lead to wider bid-ask spreads and less accurate pricing. This lack of liquidity introduces uncertainty into the hedging strategy and increases the potential for basis risk.

Finally, external events and market uncertainties can significantly impact basis risk. Factors such as geopolitical tensions, economic crises, or changes in government policies can create volatility in the spot market, causing basis risk to widen. Additionally, unexpected supply or demand shocks can also disrupt the correlation between the spot market and the futures contract, further exacerbating basis risk.

By recognizing and understanding these contributing factors, market participants can take proactive measures to manage basis risk effectively. This may include diversifying hedging strategies, choosing contracts with delivery dates more aligned with the underlying asset’s timeframe, and closely monitoring the market conditions and quality differentials that can impact basis risk.

Examples of basis risk in hedging

Understanding basis risk is essential for investors and financial institutions involved in hedging strategies. Let’s explore a few examples that demonstrate how basis risk can impact the effectiveness of hedging.

Example 1: Agricultural Commodities

Consider a corn farmer who wants to hedge against potential price fluctuations by using corn futures contracts. The farmer enters into a futures contract with a delivery date that aligns with the expected harvest time. However, if weather conditions impact the crop yield, causing a delay in the harvest, there could be a mismatch between the futures contract expiration and the actual delivery of the corn. This timing discrepancy results in basis risk, as the spot price of corn at the time of delivery may differ from the futures price, potentially offsetting the intended hedging benefits.

Example 2: Oil Producers

Oil producers often use futures contracts to hedge against fluctuations in oil prices. However, basis risk can occur due to variations in regional oil prices. For instance, an oil producer in North America may hedge using WTI (West Texas Intermediate) futures contracts. If geopolitical events or infrastructure constraints cause local oil prices to deviate from WTI prices, the basis will widen, increasing the risk of loss in the hedging position.

Example 3: Interest Rate Swaps

Financial institutions frequently use interest rate swaps to manage their exposure to interest rate changes. However, basis risk can arise if there is a mismatch between the reference rate used in the swap contract and the actual borrowing or lending rate of the institution. This discrepancy can lead to basis risk, as the difference between the rates can result in unexpected cash flows, impacting the effectiveness of the hedging strategy.

These examples demonstrate how basis risk can arise in various hedging scenarios. The key takeaway is that market conditions, timing, quality differentials, and regional variations can all contribute to basis risk. It is crucial for market participants to carefully evaluate the potential basis risk before implementing their hedging strategies.

Managing basis risk

While basis risk is inherent in hedging strategies, there are several approaches that market participants can take to effectively manage and mitigate its impact. Here are some common methods:

1. Diversification: By diversifying their hedging strategies, market participants can reduce their exposure to basis risk. This can involve using a combination of futures contracts with different expiration dates or utilizing various derivatives instruments that correlate with the underlying asset in different ways. Diversification can help offset the risk of a widening basis in a single contract or market.

2. Regular monitoring and adjustment: It is important to continuously monitor the basis and its impact on the hedging position. If the basis starts to deviate significantly, adjustments can be made to the hedging strategy. This might involve closing out or rolling over existing futures contracts or implementing additional hedges to better align with current market conditions.

3. Averaging and layering: Rather than entering into a single hedge at a specific point in time, market participants can employ averaging and layering techniques. This involves entering into multiple hedge positions over a period of time or at different price levels. By spreading out the hedging activity, the impact of temporary basis fluctuations can be mitigated.

4. Analyzing historical data: Examining historical basis patterns for the specific underlying asset can provide valuable insights into potential basis risk. Analyzing historical data can help identify seasonal trends, price differentials, and other factors that may influence basis risk. This information can then be used to inform hedging decisions and adjust the hedging strategy accordingly.

5. Hedging using options: Options contracts can offer more flexibility in managing basis risk compared to traditional futures contracts. By utilizing options, market participants can limit downside risk while still providing upside potential in the underlying asset. Options can be combined with futures contracts to create more tailored hedging strategies that account for basis risk.

6. Collaboration and communication: Effective communication and collaboration between different parties involved in the hedging process, such as producers, consumers, and financial institutions, can help manage basis risk. Sharing information, market insights, and coordinating hedging activities can contribute to a more comprehensive and efficient risk management approach.

It is important to note that managing basis risk does not eliminate it entirely. Basis risk is an inherent part of hedging strategies, and complete elimination is not feasible. However, by implementing these strategies, market participants can minimize the impact of basis risk on their hedging positions and improve their overall risk management capabilities.

Conclusion

Basis risk is an essential concept to understand when utilizing futures contracts for hedging in the world of finance. It refers to the potential discrepancy between the spot price of the underlying asset and the price of the futures contract. While basis risk cannot be entirely eliminated, understanding its factors and implications is crucial for effective risk management.

In this article, we explored the definition of futures contracts and hedging as a risk management strategy. We learned that hedging involves using futures contracts to offset potential fluctuations in the price of an underlying asset. However, basis risk arises due to imperfect correlation between the spot price and the futures price.

We discussed the factors that contribute to basis risk, such as timing differences, geographic variations, quality differentials, and market liquidity. These factors can impact the effectiveness of hedging strategies, and market participants must evaluate them to minimize potential losses.

Furthermore, we explored real-life examples illustrating how basis risk can manifest in different hedging scenarios, including agricultural commodities, oil producers, and interest rate swaps. These examples demonstrated the importance of understanding basis risk and its potential impact on hedging outcomes.

To effectively manage basis risk, market participants can employ various strategies, including diversification, regular monitoring and adjustment, averaging and layering, analyzing historical data, hedging using options, and promoting collaboration and communication among stakeholders.

In conclusion, basis risk is an inherent part of using futures contracts for hedging. By recognizing the factors contributing to basis risk and implementing appropriate risk management strategies, market participants can minimize the impact of basis risk on their hedging positions. This allows them to protect their investments, mitigate losses, and navigate the ever-changing financial markets with more confidence.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: Sunny • Finance

By: • Finance