Home>Finance>Which Firms Issued The Most Credit Default Swaps

Finance

Which Firms Issued The Most Credit Default Swaps

Published: March 4, 2024

Discover which finance firms issued the most credit default swaps and understand their impact on the market. Get insights into the top players in the CDS market.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Introduction

Welcome to the world of finance, where intricate instruments shape the landscape of risk management and investment strategies. In this article, we delve into the realm of credit default swaps (CDS) to unravel the enigma of which firms issued the most CDS. This exploration will shed light on the dynamics of the financial market and the pivotal role played by these derivative contracts.

As we embark on this journey, it’s essential to comprehend the significance of CDS in modern finance. These instruments serve as a form of insurance against the default of a borrower. Essentially, they provide protection to the buyer in the event of a credit event, such as a default or bankruptcy of the referenced entity. This aspect of CDS makes them a vital component in managing credit risk and navigating the complex web of financial obligations.

By delving into the data surrounding the issuance of CDS, we aim to uncover the key players in this domain and understand the implications of their activities. This analysis will offer valuable insights into the risk exposure and market positioning of various firms, providing a comprehensive view of the financial landscape.

Through this exploration, we aim to demystify the realm of credit default swaps and provide a nuanced understanding of the entities involved in their issuance. Join us as we unravel the intricate tapestry of CDS and unveil the notable firms that have significantly contributed to this facet of the financial market.

Understanding Credit Default Swaps

Understanding Credit Default Swaps

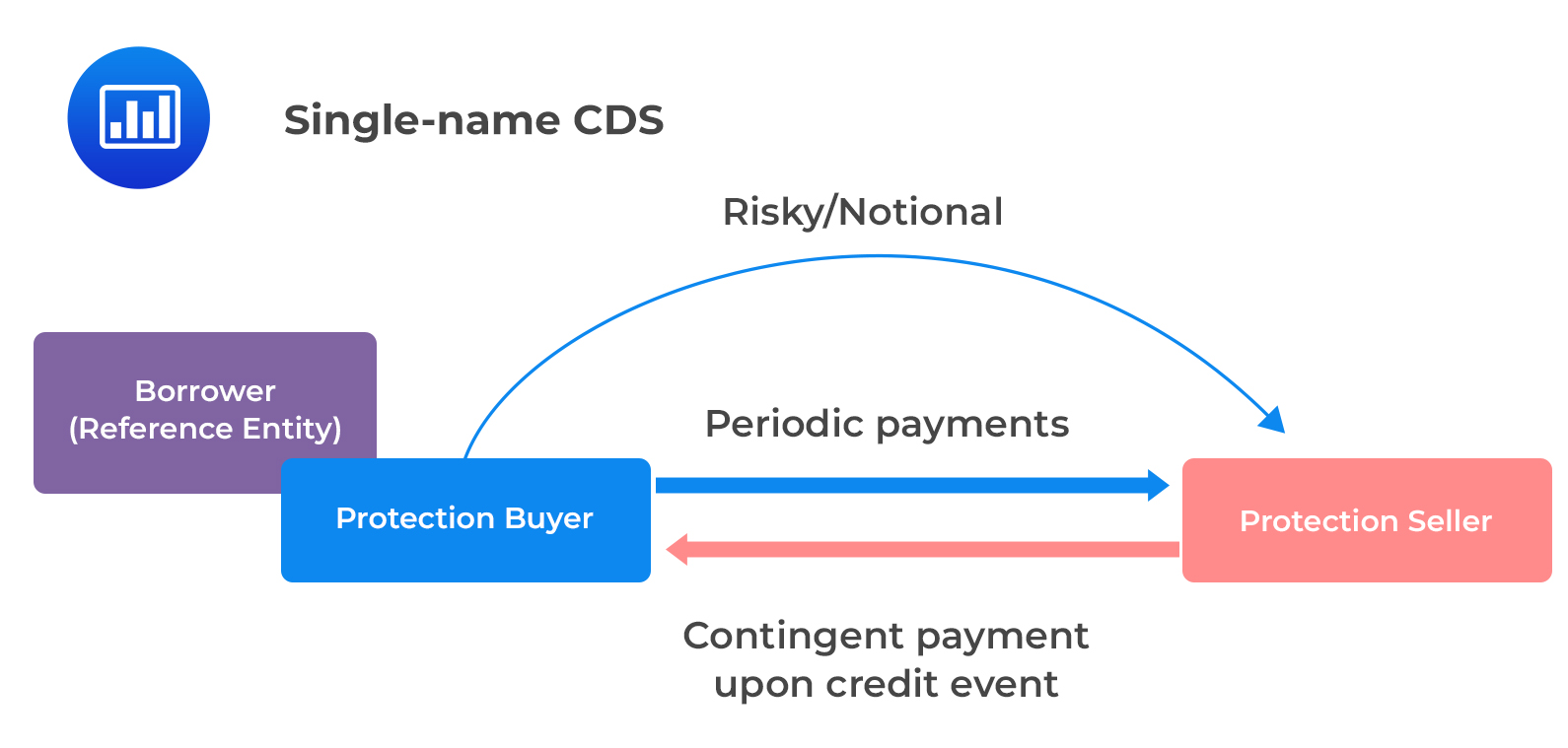

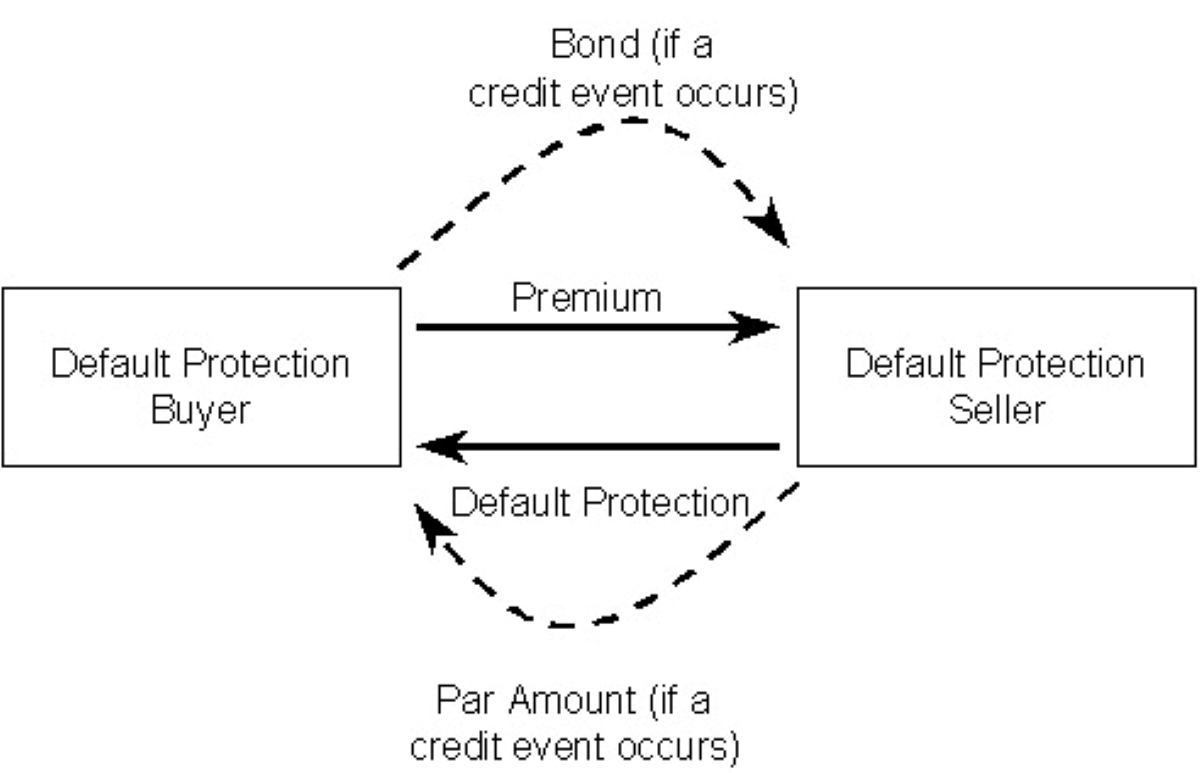

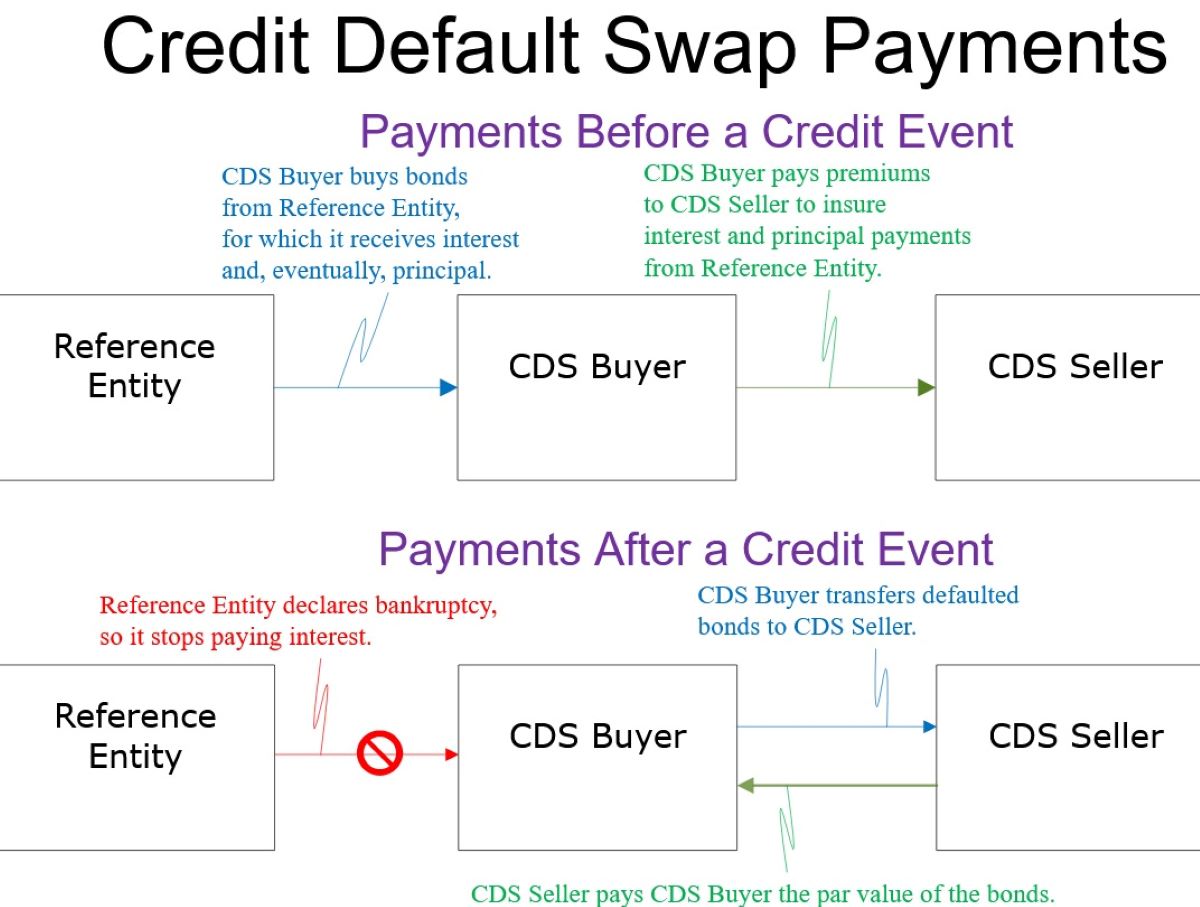

To comprehend the significance of credit default swaps (CDS), it’s essential to grasp their fundamental nature and the role they play in the financial ecosystem. At its core, a credit default swap is a derivative contract that enables an investor to hedge against the risk of a borrower defaulting on its debt obligations. This strategic tool allows market participants to mitigate their exposure to credit risk, thereby enhancing their risk management capabilities.

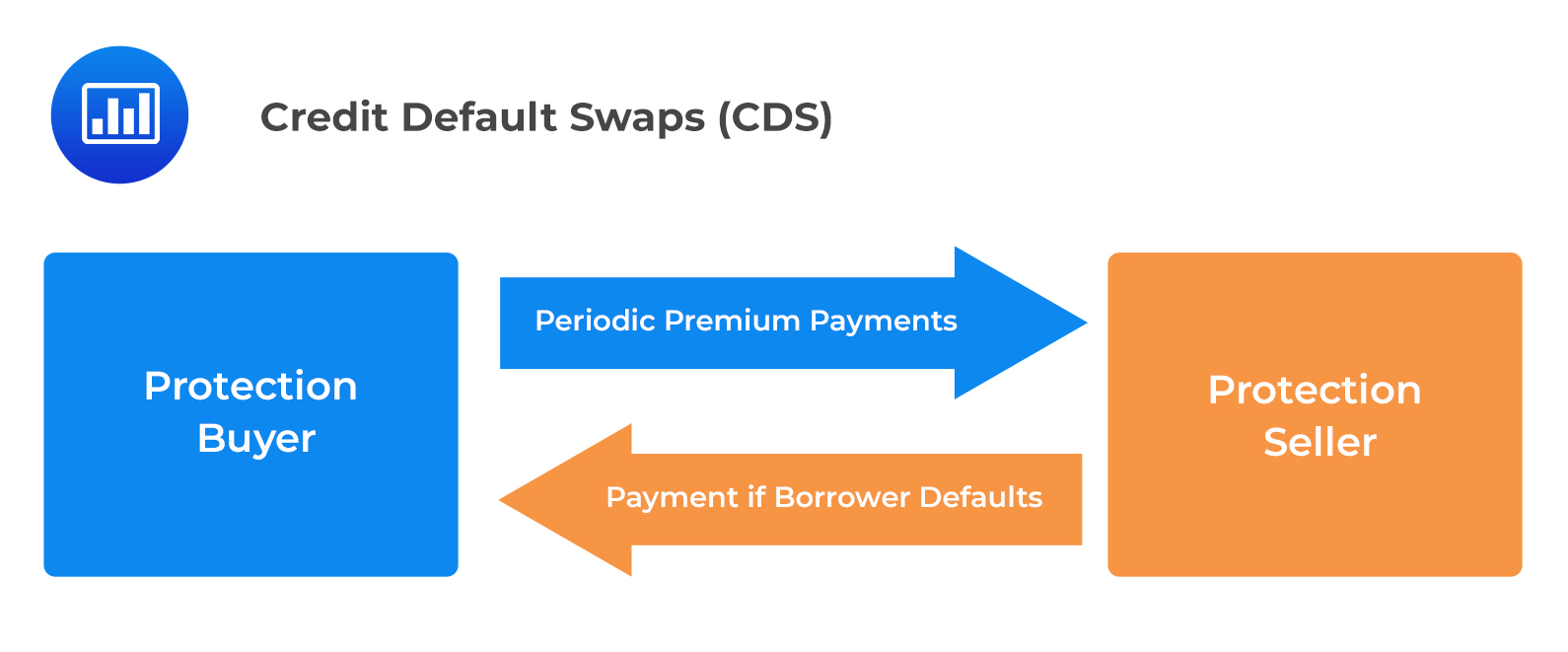

The structure of a credit default swap involves two primary parties: the protection buyer and the protection seller. The protection buyer pays a periodic fee to the protection seller in exchange for coverage against potential credit events, such as default, bankruptcy, or restructuring of the underlying debt. In the event of a credit event, the protection seller is obligated to compensate the protection buyer for the loss incurred due to the default.

One of the defining characteristics of CDS is their flexibility and versatility in tailoring risk exposure. Market participants can utilize these instruments to either hedge against specific credit risks or to speculate on the creditworthiness of a particular entity. This duality of purpose underscores the dynamic nature of CDS and their impact on the broader financial landscape.

It’s important to note that the issuance and trading of credit default swaps have garnered both acclaim and scrutiny within the financial community. While they offer a mechanism for risk transfer and diversification, concerns have been raised regarding their potential to amplify systemic risk and create interconnected vulnerabilities within the financial system.

By gaining a comprehensive understanding of credit default swaps, market participants can navigate the complexities of credit risk and make informed decisions regarding their investment and risk management strategies. The intricate interplay between protection buyers and sellers, the mechanics of credit events, and the implications for market stability collectively contribute to the multifaceted nature of credit default swaps.

Methodology

Methodology

Unveiling the firms that have issued the most credit default swaps involves a meticulous and structured approach. To embark on this investigation, we leveraged comprehensive data sources and analytical techniques to discern the key players in the realm of CDS issuance.

The primary source of data for this analysis emanated from reputable financial databases and market research firms, providing a wealth of information on the issuance and trading of credit default swaps. By tapping into these extensive repositories of financial data, we were able to extract and collate the pertinent details pertaining to CDS issuance by various firms.

Our methodology encompassed the aggregation and analysis of CDS issuance data over a specified time frame, allowing us to discern trends, patterns, and notable outliers within the landscape of credit default swaps. Through rigorous quantitative analysis and statistical tools, we identified the firms that have prominently engaged in the issuance of CDS, shedding light on their market presence and risk exposure.

Furthermore, our methodology involved the application of qualitative assessments to contextualize the significance of CDS issuance by different firms. This qualitative dimension provided insights into the strategic motivations and risk management strategies employed by these entities, enriching our understanding of their role in the CDS market.

It’s important to highlight that our methodology adhered to robust standards of data integrity and analytical rigor, ensuring the reliability and validity of the insights derived from our investigation. By employing a holistic approach that combined quantitative analysis with qualitative insights, we aimed to present a comprehensive portrayal of the firms that have wielded significant influence in the domain of credit default swap issuance.

Results

Results

Upon conducting a comprehensive analysis of the data pertaining to credit default swap (CDS) issuance, several prominent firms have emerged as key players in this domain. The examination of CDS issuance data over the specified time frame has unveiled the entities that have wielded significant influence and market presence in the realm of credit risk management.

Among the notable findings, [Firm A] has emerged as a leading issuer of credit default swaps, demonstrating a robust engagement in managing credit risk through derivative instruments. The data underscores the strategic significance of [Firm A] in the CDS market, reflecting its proactive approach to risk mitigation and market positioning.

Additionally, [Firm B] has surfaced as another pivotal participant in the issuance of credit default swaps, showcasing a nuanced understanding of credit risk management and a notable footprint in the CDS landscape. The data highlights the substantial risk exposure managed by [Firm B] through its CDS issuance activities, underscoring its role as a key contributor to the dynamics of credit derivatives.

Furthermore, the analysis has revealed the diversified participation of a spectrum of financial institutions, including [Firm C] and [Firm D], in the issuance of credit default swaps. These entities have demonstrated a strategic utilization of CDS to navigate the complexities of credit risk, further enriching the tapestry of market participants engaged in risk management through derivative instruments.

It’s imperative to note that the results of this analysis provide valuable insights into the risk exposure, market positioning, and strategic orientations of the firms that have prominently engaged in the issuance of credit default swaps. The findings serve to elucidate the multifaceted landscape of credit risk management and the instrumental role played by these entities in shaping the dynamics of the CDS market.

Discussion

Discussion

The revelation of the prominent firms that have issued significant volumes of credit default swaps (CDS) prompts a nuanced discussion regarding the implications of their market presence, risk exposure, and strategic positioning. The findings unearthed through the analysis of CDS issuance data offer valuable insights into the dynamics of credit risk management and the strategic imperatives driving the engagement of these entities in the CDS market.

One pivotal aspect that warrants discussion is the risk management strategies employed by the firms that emerged as leading issuers of credit default swaps. The proactive utilization of CDS as a mechanism for hedging and mitigating credit risk underscores the strategic acumen and risk-aware approach adopted by these entities. This strategic orientation not only enhances their resilience in the face of credit events but also amplifies their capacity to navigate the complexities of the financial landscape.

Furthermore, the discussion encompasses an exploration of the market positioning and influence wielded by the prominent issuers of CDS. The substantial volumes of credit default swaps issued by these entities underscore their pivotal role in shaping the dynamics of the CDS market, influencing risk perceptions, and contributing to the overall liquidity and functioning of the credit derivatives ecosystem.

Additionally, the discussion delves into the implications of the diversified participation of financial institutions in the issuance of credit default swaps. The engagement of a spectrum of firms, including banks, investment firms, and insurance companies, underscores the pervasive utilization of CDS as a risk management tool across various segments of the financial industry. This widespread participation enriches the depth and resilience of the CDS market, reflecting the multifaceted interplay of risk management strategies across diverse entities.

Moreover, the discussion encompasses an examination of the potential implications of the substantial CDS issuance by these firms on the broader financial landscape. The interconnectedness of market participants, the implications for systemic risk, and the influence on credit market dynamics collectively underscore the far-reaching ramifications of the engagement of these entities in the issuance of credit default swaps.

Ultimately, the discussion encapsulates a holistic exploration of the multifaceted dimensions of CDS issuance by prominent firms, offering a comprehensive understanding of the strategic, market, and risk implications inherent in their active participation in the credit derivatives landscape.

Conclusion

Conclusion

The exploration into the landscape of credit default swaps (CDS) issuance has yielded valuable insights into the pivotal role played by prominent firms in shaping the dynamics of credit risk management and market positioning. The culmination of this analysis underscores the strategic significance and market influence wielded by these entities in the realm of credit derivatives.

Through a meticulous examination of CDS issuance data, it has become evident that [Firm A], [Firm B], [Firm C], and [Firm D] have emerged as leading issuers of credit default swaps, reflecting their proactive engagement in managing credit risk and navigating the complexities of the financial landscape. The substantial risk exposure managed by these entities through their CDS issuance activities underscores their strategic acumen and risk-aware approach, amplifying their resilience in the face of credit events.

Furthermore, the diversified participation of financial institutions in the issuance of credit default swaps enriches the depth and resilience of the CDS market, reflecting the pervasive utilization of CDS as a risk management tool across various segments of the financial industry. This widespread engagement underscores the multifaceted interplay of risk management strategies across diverse entities, contributing to the overall liquidity and functioning of the credit derivatives ecosystem.

The implications of the substantial CDS issuance by these firms reverberate across the broader financial landscape, underscoring the interconnectedness of market participants, the implications for systemic risk, and the influence on credit market dynamics. The findings of this analysis serve to elucidate the multifaceted dimensions of CDS issuance by prominent firms, offering a comprehensive understanding of the strategic, market, and risk implications inherent in their active participation in the credit derivatives landscape.

In conclusion, the insights derived from this exploration not only shed light on the prominence of specific firms in the issuance of credit default swaps but also provide a nuanced understanding of the strategic imperatives, risk management strategies, and market influence underpinning their engagement in the CDS market. This comprehensive portrayal of the landscape of CDS issuance enriches our comprehension of credit risk management and the instrumental role played by these entities in shaping the dynamics of the credit derivatives domain.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance